Alibaba Group Holding Limited (NYSE: BABA) is scheduled to report its results for the first quarter of Fiscal 2023 on August 4, before the market opens. As of now, there are fears that China’s tech crackdown initiatives and zero-COVID policy, which is leading to regional lockdowns, can hurt the company’s earnings results.

Shanghai, China’s major financial hub, was under strict lockdown for two months during the to-be-reported quarter. This would have adversely impacted Alibaba’s financials. Citing similar reasons, the company didn’t provide any financial guidance for Fiscal 2023.

However, the performance of the company’s Cloud segment has remained solid. Alibaba has developed more diversified sources like rising revenue contribution from non-Internet industries within the Cloud business, which should boost its results.

With some support from China commerce, local consumer services, and Digital media and entertainment segments, Alibaba is expected to see strength in the International commerce retail business, which largely includes Lazada, AliExpress, Trendyol, and Daraz, in the to-be-reported quarterly results.

Consensus Estimates for Q1 Are Mixed

For the first quarter of Fiscal 2023, the consensus estimate for Alibaba’s earnings is pegged at $1.60 per share. The company had posted earnings of $2.57 per share in the year-ago period.

Meanwhile, analysts expect the company to post revenues of $30.16 billion in the first quarter, lower than the previous year’s tally of $32.37 billion.

Regulatory Hurdles Haunt BABA Stock

BABA and nearly 270 Chinese companies listed in the United States are facing the risk of getting delisted under the Holding Foreign Companies Accountable Act. These Chinese companies are required to comply with U.S. auditing requirements until early 2024 to avoid delisting.

In this regard, a Financial Times report recently highlighted that Chinese securities regulators are considering a three-tier data strategy that will aid Chinese firms to come into compliance with U.S. rules. However, the China Securities Regulatory Commission (CSRC) has denied contemplating any such move, as per a Reuters article.

Further, the stock declined around 8% on July 11 after the Chinese government imposed a fine of about $372,000 on BABA for failing to comply with certain anti-monopoly rules, according to a Motley Fool article.

Website Traffic Trends Reflect a Weak Q1

According to TipRanks’ Website Traffic Tool, Alibaba’s websites — aliexpress.com, alibaba.com, and taobao.com — recorded a 22.7% decline in global visits in June, compared to the same period last year. Further, quarter-to-date (April-June), the company’s website traffic declined 26.9%, compared to the previous year.

The COVID-19 lockdown in China during the larger part of the first quarter (April to June) can explain the muted website traffic growth, which also could have hurt the company’s top line. Learn how Website Traffic can help you research your favorite stocks.

Street Is Still Optimistic for BABA Stock

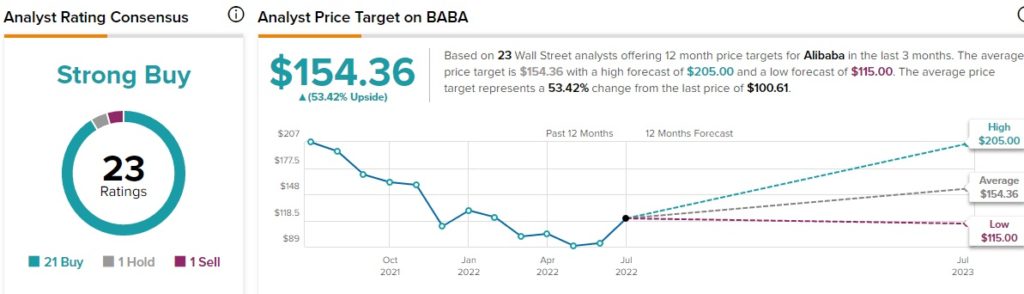

Overall, the Street is optimistic about the stock and has a Strong Buy consensus rating based on 21 Buys, one Hold, and one Sell. Alibaba’s average price target of $154.36 signals that the stock may surge nearly 53.4% from current levels. Shares of BABA have declined 16.4% so far this year.

BABA scores a 9 out of 10 on TipRanks’ Smart Score rating system, indicating that the stock has strong potential to outperform market expectations.

TipRanks data shows that financial bloggers are 79% Bullish on Alibaba, compared to the sector average of 63%. The news sentiment is also Positive for the stock.

Troubled Times Ahead for BABA?

Alibaba remains exposed to macroeconomic challenges. Also, COVID-19 lockdowns in China are expected to put the company’s financials under pressure. However, continued strength in the company’s global consumer-facing businesses makes BABA a hot stock for long-term investors.

Read full Disclosure