Airbnb (ABNB) is the largest online booking agency/network for temporary accommodations, and also offers booking services for boutique hotels and experiences.

The company boasts a network of over 4 million hosts across 220 countries and over 100,000 cities. It generates just over half of its revenues in North America, another 30% in EMEA, and the rest in Asia-Pacific and Latin America. (See Airbnb stock analysis on TipRanks)

The main value for ABNB comes from online transaction fees for bookings on its website, which are generated through its massive host network. Its competitive advantage stems from its wide array of attractive and reasonably priced accommodation offerings that make it the booking agency of choice for travelers. As more people use it to book accommodations, Airbnb’s moat is further widened.

Pluses and Minuses

The company is expected to continue generating strong growth on the back of the re-opening of the global economy from the COVID-19 outbreak. It should also perform well in its markets outside of North America. In those areas, Airbnb controls much less market share, but it still has a significant presence and strong brand recognition.

That being said, the company also has numerous challenges to contend with.

First and foremost, it already faces significant competition from the well-entrenched hotel industry and other competing sites like VRBO. Additionally, sites like TripAdvisor (TRIP), the large online travel agencies, and even some of the tech mega caps like Facebook (FB), Amazon (AMZN), and Google (GOOG) may decide to leverage their large troves of consumer data and existing customer networks within their own ecosystems to edge into Airbnb’s market.

Any or all of these potential competitors mounting a major push into the space would compress margins significantly and put a major dent in ABNB’s growth and earnings potential.

Valuation Metrics

Despite these headwinds, ABNB still possesses a significant head start in the segment, giving it a significant edge to leverage in terms of industry-specific consumer data and network.

However, its valuation remains elevated. The forward EV/EBITDA is quite high at 109x and the company remains unprofitable on a net income basis. Analysts expect the company to generate $0.07 earnings-per-share in 2022, which would put the current share price at nearly 2,000 times 2022 earnings.

Wall Street’s Take

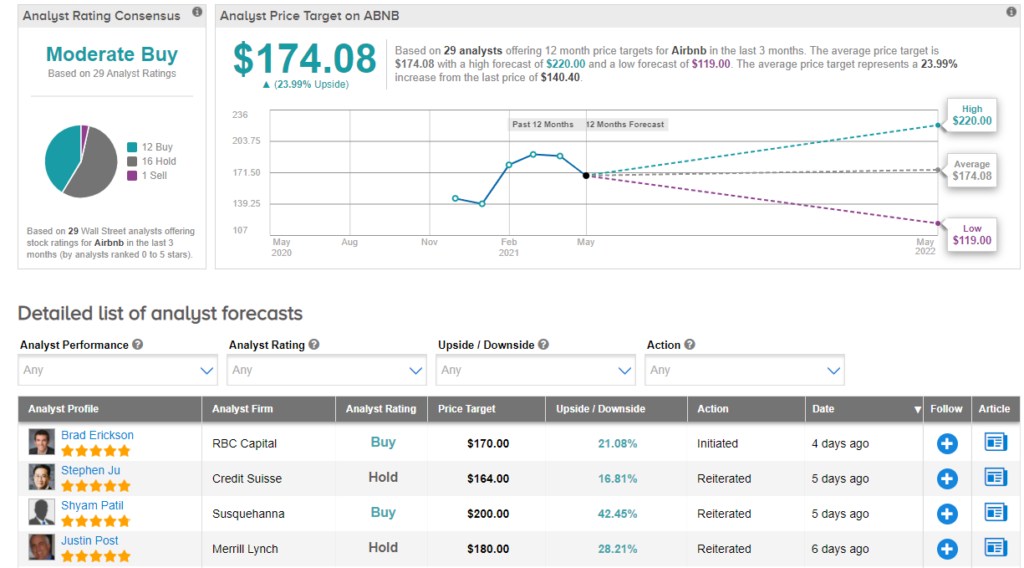

From Wall Street analysts, ABNB earns a Moderate Buy analyst consensus based on 12 Buy ratings, 16 Hold ratings, and 1 Sell rating in the past 3 months. Its average analyst price target of $174.08 puts the upside potential at 24%.

Summary and Conclusions

ABNB is facing significant headwinds right now, as it struggles to emerge from the COVID-19 pandemic while also facing potential competition from several deep-pocketed heavyweight companies. As a result, the company’s growth could take a hit in the near future and underperform expectations.

Nonetheless, it still has a lot going for it with a significant head start in industry-specific consumer data collection and network effect. Furthermore, it already has a foothold in countries across the globe and millions of loyal customers and hosts. Those users are already familiar with and loyal to Airbnb’s platform and style, making them less likely to switch to a competitor.

Overall, the business is likely to continue growing and analysts remain bullish on the shares here.

At the same time, given the potential for reduced profit margins due to growing competition and the elevated valuation multiples at current prices, the stock could face significant downside if it fails to live up to lofty growth expectations.

Disclosure: On the date of publication, Samuel Smith had no position in any of the companies discussed in this article.

Disclaimer: The information contained herein is for informational purposes only. Nothing in this article should be taken as a solicitation to purchase or sell securities.