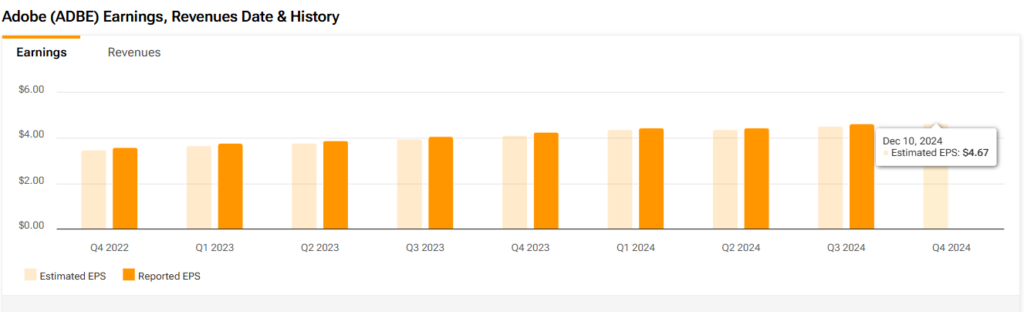

Adobe’s (ADBE) fiscal Q4 earnings are set to be released on December 11th, after the market close. I remain bullish on Adobe stock heading into earnings, especially after the stock’s “de-risking” from the bearish reaction to the August quarter. While Q4 guidance was softer, indicating slower top-line growth, moderate expectations, and an attractive valuation suggest a stable quarter ahead. Over the past seven quarters, Adobe has consistently surpassed EPS expectations while delivering revenue growth of at least 9%, even in mixed economic environments.

Confident Investing Starts Here:

- Easily unpack a company's performance with TipRanks' new KPI Data for smart investment decisions

- Receive undervalued, market resilient stocks right to your inbox with TipRanks' Smart Value Newsletter

In this article, I’ll recap Adobe’s recent results, explain the reasons behind the bearish momentum, outline what investors can expect from Fiscal Q4, and discuss why I see Adobe as an attractive buying opportunity as earnings day approaches.

Recapping Adobe’s Q3

Contributing to my bullish outlook on Adobe, the company’s fiscal third-quarter results, released in September, were quite solid. Adobe exceeded both revenue and non-GAAP earnings expectations, beating the top line by $40 million and non-GAAP EPS by 11 cents. The company reported $5.41 billion in revenue and EPS of $4.65, reflecting nearly 11% growth compared to the same period last year.

Looking at Adobe’s income statement, an interesting point is that its cost of revenue actually decreased by around $26 million compared to the previous year. This suggests that Adobe has become more efficient in generating revenue, as it costs the company less to produce this revenue. As a result, its gross profit increased by approximately $544 million, reaching a total of $4.85 billion for the quarter.

On the expense side, Adobe’s operating expenses grew by about 10% year-over-year, rising to $2.86 billion, compared to $2.61 billion in the same quarter last year. However, despite the increase in operating expenses, the company still managed to grow its operating income by around $300 million, bringing it to $1.99 billion. This demonstrates that Adobe was able to effectively manage costs while still achieving strong profitability.

Why Was the Post-Q3 Reaction So Bearish?

Despite Adobe’s solid reported results, which, in theory, should have reinforced the bullish sentiment around ADBE stock, the market’s reaction was quite the opposite. Shares plummeted by double digits, falling as much as 18% from September 12 to the end of October.

The main issue stemmed from the outlook provided for the fourth quarter. According to the company, it expects revenue to fall between $5.5 billion and $5.55 billion, translating to a 9% year-over-year growth for Q4. This suggests that Adobe anticipates its revenue growth will continue to decelerate into the fourth quarter. The slowdown in growth was a major concern raised by analysts during the conference call, as it indicates a broader slowdown in the company’s business.

To make matters worse, Adobe is also projecting approximately $550 million in net new annual recurring revenue (ARR) for Q4, representing a 3% year-over-year decline compared to the ARR growth seen in Q4 2023. This decline in net new ARR, coupled with decelerating revenue growth, raised further alarms. Both slowing revenue growth and ARR growth are concerning, especially when combined. In fact, a 9% year-over-year revenue growth for Q4 would mark Adobe’s lowest revenue growth rate in the past five years. The previous low was 9.2% in Fiscal Q1 2022.

What Else to Expect from Fiscal Q4?

Despite the soft guidance, which has dragged the stock down, I remain optimistic about Adobe’s upcoming earnings, believing that buying on the weakness presents a good opportunity. First, I think the bar has been lowered for Adobe, given that the negative surprise from the slowdown in top-line growth for Q4 seems to have already been priced in. This reduces the risk of even greater disappointments.

While 26 out of 27 analysts have revised downwards their revenue growth forecasts, the outlook for earnings is more favorable. In fact, 16 out of 25 analysts have revised their EPS estimates upward heading into Fiscal Q4. Adobe’s guidance for non-GAAP EPS is between $4.63 and $4.68, implying a 9.6% growth at the higher end of the range.

Additionally, it will be interesting to see progress on Adobe’s generative AI platform, Firefly, which made significant strides in Q3 through integration into core applications like Photoshop and Lightroom. This integration could lead to improved margins in the coming quarters, especially considering that operating margins are currently at an impressive ~36%.

The company has also made it clear that it has no plans to provide guidance for Fiscal 2025, which could ultimately be a positive move to avoid unnecessary disappointments (or not), as was the case in the previous quarter.

Making the Case for Valuations on ADBE

Finally, I believe Adobe stock, down around 10% over the last twelve months and underperforming the S&P 500 (SPY), now presents a decent “buy the dip” opportunity. With the stock trading at a P/E ratio of 30x—more than 20% below its five-year average—it looks attractive at this valuation.

While bears argue that Adobe is lagging behind other tech giants in the midst of the AI boom, with revenue growth slowing, its business model remains steady and predictable, coupled with world-class margins. This consistency arguably warrants a premium compared to the broader industry.

On the other hand, despite the deceleration in top-line growth, the bottom line remains strong. Adobe’s net income has grown at a compound annual growth rate (CAGR) of 14% over the past five years, and EPS growth is expected to rise by 17.6% over the next three to five years. With a forward P/E multiple of 29x, Adobe trades at a PEG ratio of 1.67. While not a bargain, this is still well below the average of other software companies, which trade at around 2x.

Is ADBE A Good Buy, According to Wall Street Analysts?

At TipRanks, the Wall Street consensus on ADBE is a Moderate Buy rating. Of the 30 analysts covering the stock, 23 have a Buy recommendation, five have a Hold rating, and only two have a Sell recommendation. The average ADBE stock price target is $621.81, suggesting an upside potential of 15.9% from the current share price.

Conclusion

I hold a Buy stance on Adobe heading into its earnings. The reality check in Fiscal Q3 for Adobe, marked by conservative guidance for Fiscal Q4, in my view, has effectively de-risked the stock, making it an appealing opportunity for long-term investors.

Adobe’s robust business model, characterized by recurring revenues, best-in-class margins, and solid cash flows undeniably positions it as a company deserving of a premium valuation. With expectations for Fiscal Q4 now set relatively low, particularly on the top line, this could present an attractive buy opportunity to capitalize on weakness, given that the stock is currently trading at valuation multiples well below historical averages.

Looking for a trading platform? Check out TipRanks' Best Online Brokers , and find the ideal broker for your trades.

Report an Issue