Apple (AAPL) is one of the most well-regarded stocks among tech sector stars. AAPL stock was soaring early in the year, but since has dipped amidst broader market fears. The macro-economic situation has created uncertainty, but it might be a good time for savvy investors to pick it up while it trades at multi-year lows. Not to forget, Apple’s self-sustaining ecosystem and rock-solid cash balance indicate that it can weather the current economic storm, and offer massive gains down the line. Hence, I am bullish on AAPL stock

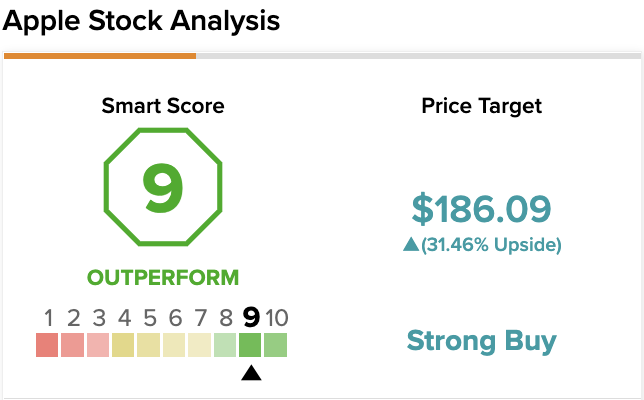

On TipRanks, AAPL scores a 9 out of 10 on the Smart Score spectrum. This indicates a high potential for the stock to outperform the broader market.

Apple Works Better than a Magnet at Attracting Customers

Apple always succeeds at keeping people coming back to its incredibly popular product base. This quality has helped the company earn billions before and continues to provide it with a competitive advantage. Apple, in its second quarter of 2022, generated more than $97 billion in revenue.

The iPhone, which is considered Apple’s bread and butter, contributed more than $50 billion to overall sales. Undoubtedly, Apple’s products, especially the iPhone, have what it takes to sustain this level of growth. Hence, the iPhone has it all covered.

Apple has had a knack for grabbing opportunities. The company recognized the 5G opportunity and has pounced on it. Apple released 5G-compatible phones in late 2020 to which has led to a double-digit surge in revenues since its release.

Despite the high revenue growth, it might be ignorant to assume that Apple won’t be hurt by inflation. The increase in prices might put consumers off from buying Apple’s devices. But the good part is that Apple isn’t just a hardware company. The firm’s diversification towards software-as-a-service (SaaS) has aided Apple in generating recurring revenue through subscriptions.

The company’s service segment, which comprises of digital payments, AppleCare, cloud storage, and advertising products, saw a revenue hike from $46.3 billion in 2019 to more than $68 billion last year.

Incredibly Sticky Ecosystem

Apple’s self-sustaining ecosystem must be one of the reasons to invest in the company’s stock. In addition, the interplay between Apple’s products and services ensures that consumers rely on both, which means Apple’s revenue will bolster as more people continue to subscribe between product purchases.

The amazing part is that Apple is consistently putting efforts into expanding this ecosystem. The company has acquired more than 100 companies in the last few years, and it spends millions in research and development just to enhance the ecosystem it has built over the years.

The company’s research and development budget has soared from $0.78 billion in 2007 to a whopping $21.91 billion. The considerable research and development cost represents half of the company’s operating expenses. This means that Apple’s expenses today will turn into profits in the long run.

A Cash Flow Generating Machine

Cash hoarding is one of Apple’s powerful assets. The company wrapped up its second quarter with more than $193 billion in cash and cash equivalents. So, while looking at Apple’s cash flow, one can say that Apple has a lot of capital to put into work.

The powerful cash position has not only helped Apple invest in research and development, but rewarded shareholders. For instance, Apple spent a massive $85.5 billion in share repurchases and $14.5 billion on dividends last year. Hence, it reaffirms its commitment to reward its shareholders.

Wall Street’s Take

Turning to Wall Street, AAPL stock maintains a Strong Buy consensus rating. Out of 28 total analyst ratings, 22 Buys and six Holds were assigned over the past three months.

The average AAPL price target is $186.09, implying 31.46% upside potential. Analyst price targets range from a low of $157 per share to a high of $210 per share.

Final Word on AAPL Stock

Apple’s strong cash flows and liquidity are reason enough to invest in the tech giant. Its timeless products continue to impress and leave an indelible mark on its burgeoning customer base. Moreover, the company’s thriving service segment continues to grow at double-digit rates, entailing that revenue will keep growing in the future. Yes, Apple isn’t unsusceptible to macroeconomic challenges, so the stock may experience pain in the short run.

However, it doesn’t take away from its incredible long-term case which continues to get stronger over time. Hence, it’s plausible to expect another bumpy year, despite the headwinds.

So while macroeconomic factors such as inflation and recession fears may paint a sordid picture, investors holding AAPL stock will be glad they picked up the right company for the long haul.

Read full Disclosure

Questions or Comments about the article? Write to editor@tipranks.com