If the last few months have proven anything, it’s that even a long-term bull run is still open to volatile market forces. The S&P 500 has been flirting with correction territory amid concerns over President Donald Trump’s aggressive tariff policies and escalating trade wars with key partners like Canada, Mexico, and China. These protectionist measures have led to increased market volatility, disrupted global supply chains, and heightened fears of an economic slowdown.

Investors are left navigating an environment where defensive plays become increasingly attractive, and sectors with strong long-term tailwinds stand out.

One such sector is cybersecurity. In a world where digital threats are only becoming more sophisticated, cybersecurity companies provide essential services that remain in demand regardless of market conditions. Unlike cyclical industries that ebb and flow with economic shifts, the need for data protection, network security, and compliance solutions is non-negotiable. Businesses, governments, and individuals are continually increasing their cybersecurity spending, creating a resilient revenue stream for industry leaders.

Summing up the situation in a recent note, Morgan Stanley’s Keith Weiss, an analyst ranked in the top 2% of Wall Street stock experts, explained: “Growing attack surface area matched with a rising threat environment should sustain cyber demand. At the same time, we see promising product cycles across Machine Identity, Security Analytics and SASE. Against a volatile market backdrop, Security looks poised to regain its safe haven status.”

Backed by this thesis, Weiss has spotlighted several top cybersecurity stocks. Using the TipRanks platform, we’ve dug into three of his picks – each with Buy ratings and double-digit upside potential. Let’s take a closer look.

Palo Alto Networks (PANW)

First on our list is a Silicon Valley company, Palo Alto Networks. This firm is a giant in the cybersecurity industry, founded in 2005 and today boasting a market cap of $121 billion. The company offers its subscribers and users a full line of comprehensive solutions and firewalls designed to meet the various threats of modern cyberattacks and permit a safe and secure online work environment for cloud, network, and endpoint services. Palo Alto is a leader in the global cybersec field and prides itself on keeping up with the constantly accelerating pace of change in the digital world.

At the forefront of Palo Alto’s current approach is Precision AI, the company’s AI platform built and trained based on the rich security dataset that Palo Alto has built up over the past two decades. The company’s basic premise is simple: the advent of AI, especially generative AI, has given cyber attackers a tremendous boost in speed – and defenses will need to fight that fire with fire. Palo Alto has embedded Precision AI across its product portfolio and even uses it to provide for more secure system access. The result is a simpler but much smarter security environment that makes use of intuitive AI-powered platforms to outsmart potential attackers.

Users like Palo Alto’s security features because they have proven successful. The company can protect any cloud-based network, a vital asset these days, and automation has always been a key feature – even before Palo Alto introduced its AI-powered products. The company claims that it can meet and defeat any cybersecurity challenge, no matter how advanced, and its use of AI and machine learning tech has become a key feature in that claim.

Last month, Palo Alto released its results for fiscal 2Q25, the period ending on January 31 of this calendar year. For that period, Palo Alto reported total revenue of $2.26 billion, up 14% year-over-year and beating the estimates by $20 million. At the bottom line, the company realized non-GAAP earnings of 81 cents per share, or 3 cents per share better than the forecasts. In two metrics that bode well going forward, the company reported that its next-generation security ARR (annual recurring revenue) had grown 37% year-over-year to reach $4.8 billion and that it had a remaining performance obligation, or work backlog, that hit $13 billion, up 21% year-over-year.

This stock is covered by Keith Weiss, and the 5-star analyst is upbeat on the prospects for AI tech to drive continued gains. He writes of PANW, “While still early days and likely a net tailwind across our security coverage, we think the most immediate beneficiaries from GenAI are those with large, unique data sets across multiple threat vectors. In our view, Palo Alto Networks will likely be one of the top security beneficiaries from GenAI proliferation longer term, largely driven by AI-enabled efficiencies, ramping product cycles (Cortex XSIAM, AI security) and larger platform deals… From a product perspective, the company remains well-positioned to sustain strong growth in the SecOps automation opportunity through Cortex XSIAM, which continues to see strong momentum and reached >$1B in cumulative bookings during the latest quarter.”

At the bottom line, Weiss notes several points that should continue to support this stock, saying, “Overall, we remain positive on Palo Alto Networks’ opportunity to sustain durable long-term growth, with AI likely a fundamental driver given the need for 1) securing employee access to AI, 2) securing AI workloads in the Cloud, and 3) securing AI-related network traffic.”

Quantifying his stance on PANW, Weiss rates the stock as Overweight (i.e., Buy) with a $230 price target that points toward a 12-month gain of 22.5% for the shares. (To watch Weiss’s track record, click here)

This stock gets a bullish outlook from the Street, with a Strong Buy consensus rating based on 32 recent reviews that break down to 25 Buys, 6 Holds, and 1 Sell. The shares are currently priced at $187.54, and their average price target of $218.90 implies an upside potential for the coming year of 17%. (See PANW stock forecast)

CrowdStrike Holdings (CRWD)

The next stock we’ll look at is another large-cap name in the cybersecurity world, CrowdStrike. This company specializes in endpoint security, identity threat detection, and ransomware protection. In the 14 years since its founding, CrowdStrike has become one of the industry’s go-to names, and with its $90 billion market cap, it is another industry giant.

CrowdStrike’s flagship Falcon platform is designed for a proactive approach to security, actively detecting threats and stopping breaches. The platform is billed as cloud-native, providing multi-tenant intelligent security solutions that protect networked workspaces, whether on-premises, in the cloud, or virtualized – and across all endpoints, from desktops and laptops to servers, virtual machines, and IoT devices. CrowdStrike offers 29 cloud modules on its Falcon platform, through the popular software-as-a-service model.

CrowdStrike backs up its security platform with a full range of services. These include the mundane – a variety of option packages and pricing plans for the security platform – and the technical – such as AI integration for ‘red team’ penetration testing of application security. The company uses AI to improve its security stance, as the expanding adoption of the technology is causing a surge in cybersecurity risks. According to CrowdStrike, while a majority of companies regularly use generative AI technology, only 38% are actively addressing the increased security risks associated with it. CrowdStrike aims to bring AI to the security realm, to maximize efficiency while not sacrificing security. The company’s AI capabilities include maintaining system integrity, preventing harmful activity, and guarding sensitive data.

The key to all of this is giving customers both what they want and what they need. CrowdStrike accomplishes this with a modular approach to its flagship platform, allowing subscribers to pick and choose packages or features, find the right pricing plan, and even customize a security installation.

CrowdStrike completed its fiscal year 2025 this past January 31, and in the fiscal 4Q25 report, the company showed revenue of $1.06 billion, up 25% year-over-year and $20 million better than had been anticipated. The company’s bottom line, reported as a non-GAAP EPS of $1.03, was up 8 cents per share from the previous year period and was 17 cents per share over the forecasts.

Looking ahead, CrowdStrike has a solid foundation to continue its record of strong performance. ARR was up year-over-year by 23%, to $4.24 billion, and of that total, $224 million was added during fiscal 4Q25.

Looking at this cybersecurity stalwart’s prospects, Weiss sees it as a solid choice in the space. Outlining CrowdStrike’s advantages, he writes, “CrowdStrike remains a leading platform consolidator within security and continues to gain share across core endpoint security, cloud security, identity protection and next-gen SIEM. CrowdStrike already has 32% of customers adopting 7+ modules across its platform, and has seven separate modules each contributing >$300M in total ARR. The company continues to win across the security stack, with ARR from Cloud security, identity security and LogScale Next-Gen SIEM growing ~50% YoY to >$1.3B in the latest quarter. We see a long runway for CrowdStrike to continue benefitting from platform consolidation, especially as benefits from prior customer commitment packages (CCP) roll off the model over the next few quarters and allow the company to drive larger TCV deals with longer duration.”

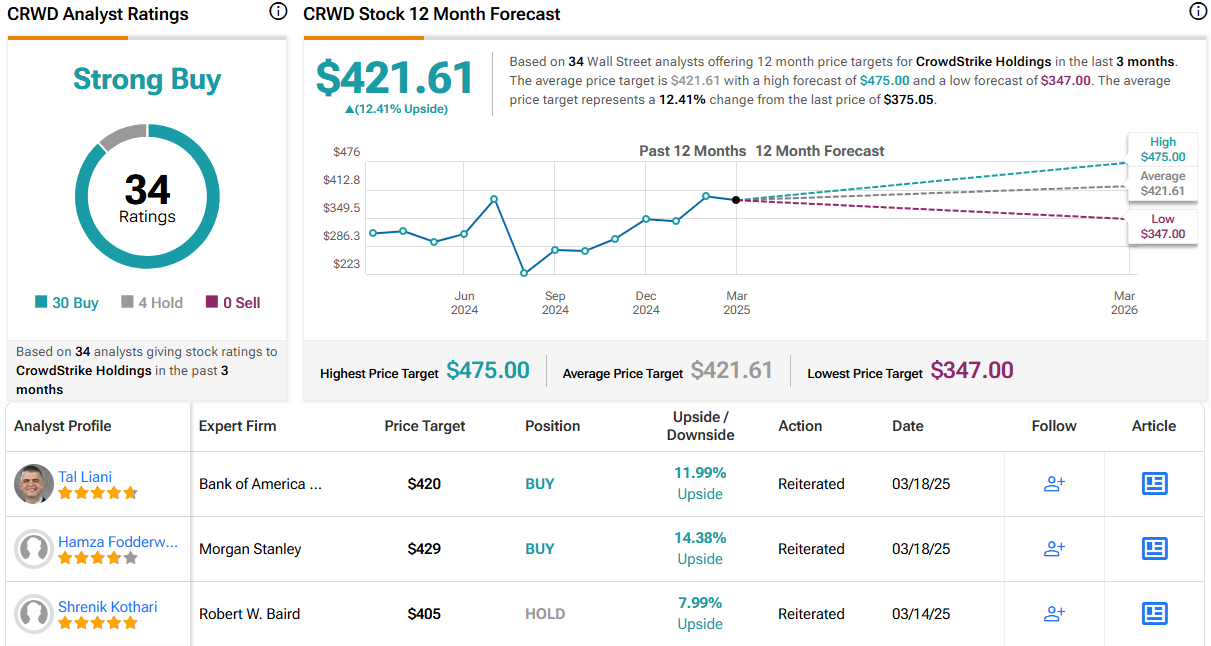

The analyst goes on to put an Overweight (i.e., Buy) rating on these shares, along with a $429 price target that indicates an 14% gain lying in wait for the year ahead.

Tech stocks typically get a lot of attention from Wall Street, and CrowdStrike is no exception. The 34 recent reviews on record for the stock include 30 to Buy and 4 to Hold, for a Strong Buy consensus rating. The average price target here is $421.61, implying a 12.5% upside potential from the current share price of $375.05. (See CRWD stock forecast)

Varonis Systems (VRNS)

For the last stock on our list, we’ll take a step down in size and look at Varonis Systems. This $4.7 billion company is an expert in automated data protection, taking the view that data is the basic commodity of the digital world and must be protected ‘first, not last.’

To achieve this, Varonis gives its customers a cloud-native data security platform, purpose-built to bring AI-powered automation capabilities to bear on the discovery and classification of critical data, the removal of security exposures, and the detection of advanced cybersecurity threats. Varonis’ customers make use of the system and its AI technology to automate security outcomes across a wide range of online environments, including SaaS, IaaS, and hybrid clouds. These automated outcomes can include data security posture management, data classification, data access governance, data detection and response, and data loss prevention. The company’s system can even provide insider risk management.

For Varonis, all of this is based on the recognition that valuable data is vulnerable data, and that cybersecurity must start where the threat is highest. The company has taken this outlook from its Miami headquarters to the global scene, with 14 offices around the world and more than 2,400 people engaged in cybersecurity work. The company generated $551 million in total revenue in 2024, for a 10% gain over 2023.

In its last reported quarter, 4Q24, Varonis reported a top line of $158.5 million, up 3% year-over-year – although we should note that the quarterly revenue missed expectations by $7.4 million. At the same time, Varonis had earnings of 18 cents per share by non-GAAP measures, a figure that was 4 cents per share better than expected. The company’s SaaS revenue grew significantly year-over-year, from $23 million in 4Q23 to $72.2 million in 4Q24.

We’ll check in again with analyst Keith Weiss, who lays out the Morgan Stanley view here, noting that Varonis presents investors with a chance to buy a quality stock at a relatively discounted price. He says of the company, “Varonis offers a unique platform to manage, secure, and optimize human generated data, well positioned to address data protection compliance requirements in a number of industries and regions. With VRNS shares trading at a discount to its Security & SMID Software peer set, we see an increasingly attractive risk-reward profile, as a confluence of trends including signs of stabilizing demand, faster than anticipated traction with the Varonis SaaS platform, and secular tailwinds benefiting data security & governance (i.e. robust data growth, generative AI use cases, regulatory and data compliance standards), come together to drive an idiosyncratic inflection in business fundamentals.”

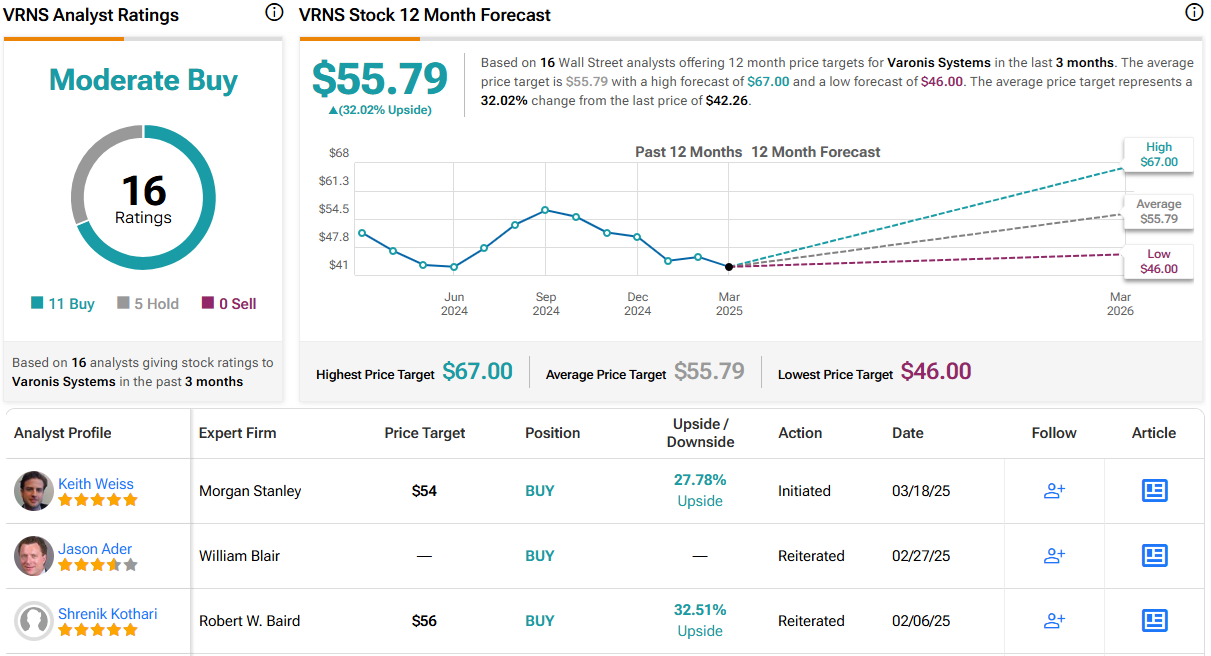

For Weiss, this adds up to an Overweight (i.e. Buy) rating, and his $54 price target suggests a 28% upside potential for the shares by this time next year.

There are 16 recent reviews on file for VRNS, with an 11 to 5 split, favoring Buy over Hold, giving the stock a Moderate Buy consensus rating. The stock is currently trading for $42.26, and its $55.79 average target price implies that it will gain 32% in the next 12 months. (See VRNS stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.