Mall-facing retailers like Nordstrom (JWN) have been on the ropes for years now. Facing a declining business thanks to online retailers and discount brick-and-mortar operations, the mall just hasn’t been all that attractive a destination. Yet, the latest word for Nordstrom has it not only coming back – but coming back strongly.

Nordstrom added 5.3% in premarket trading on Wednesday, and those gains continued into the trading session. The stock is currently up over 10%. I’m bearish on Nordstrom, however, as I am on most mall-facing retailers. While it’s managed to fend off one problem, it’s got several others waiting to pick up where that one left off.

The last 12 months for Nordstrom stock have not fared well. Plunges have been often followed by recoveries, but the recoveries seldom prove sustainable. The company is down significantly from where it was this time last year, dropping from just over $34 per share to just under $23 per share.

The latest news, meanwhile, offers at least some hope. Nordstrom’s earnings report featured a loss that was a little ahead of expectations—the company lost $0.06 per share against projections of $0.05 from Refinitiv—but revenue turned in a beat.

The company brought in $3.57 billion against projections calling for $3.28 billion. This actually brings Nordstrom back up to pre-pandemic levels of revenue.

Wall Street’s Take

Turning to Wall Street, Nordstrom has a Hold consensus rating. That’s based on nine Holds and two Sells assigned in the past three months. The average Nordstrom price target of $25.40 implies 10.6% upside potential.

Analyst price targets range from a low of $22 per share to a high of $32 per share.

Investor Sentiment is in Open Revolt

Nordstrom is not doing well in terms of investor sentiment. However, everything taken together suggests that, perhaps, investor sentiment is overblown on this one. Nordstrom currently has a Smart Score of 7 out of 10 on TipRanks. That puts it at the highest level of “neutral,” one step below “outperform.”

Investor sentiment seems to believe the exact opposite.

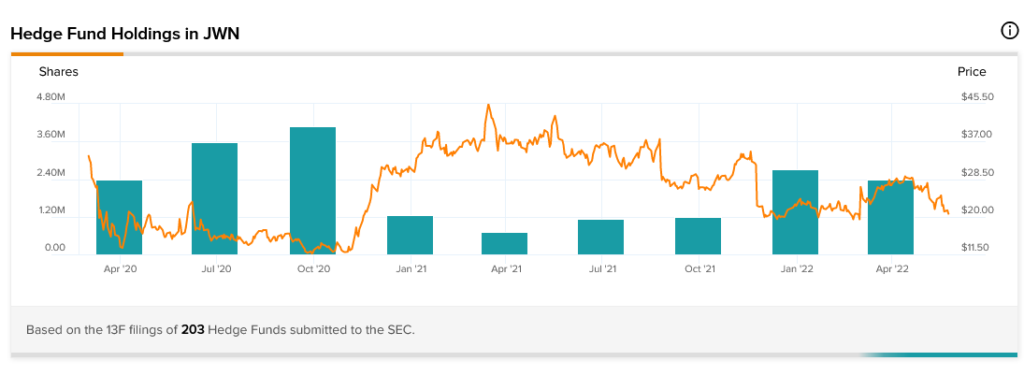

Hedge fund involvement, for example—as based on the TipRanks 13-F Tracker—is down for the first time in about a year. Hedge funds were adding to their positions in Nordstrom since March 2021 and were doing so at a steady clip.

The latest figures show a drop from just over 2.711 million shares to just over 2.386 million shares. Both of these are a long way up from this time last year, though, when hedge funds owned just over 704,000 shares.

Meanwhile, insider trading seems heavily sell-weighted, particularly in the most recent figures. While no transactions were recorded in either direction for April, the last three months show a rush to the exits. Sell transactions led buy transactions by 15 to seven.

Meanwhile, for the full year, the ratio was nearly perfectly balanced, as sell transactions led buy transactions – 26 to 24. Thus, until February 2022, buyers were actually leading sellers.

As for retail investors who hold portfolios on TipRanks, they too have been fleeing. In the last seven days, TipRanks portfolios holding Nordstrom shares dropped 0.5%. In the last 30 days, that’s down 2.8%.

Finally, there’s the matter of Nordstrom’s dividend history. After sitting out the pandemic, Nordstrom recently restarted its dividend. Granted, it’s only about half of what it was in March 2020, but it’s there.

One Bright Spot amid Disaster

Things don’t look good for Nordstrom overall, but it has one critical advantage: its primary market base.

Nordstrom targets the higher-income consumer, and we’ve seen that higher-income shoppers are commonly more willing to shop than their lower-income counterparts, especially in bad times. This makes sense; those who bring in quite a bit of money, to begin with, have more disposable income in general than those who don’t.

While even higher-income consumers are subject to the ebb and flow of recessionary times, they have further to fall. They can fall at the same rate as lower-income consumers but objectively have about the same amount of disposable income that those lower-income consumers had in good times.

Thus, Nordstrom is working to exploit its advantage. The company recently set up a deal with Allbirds (BIRD) to bring its shoe line to 14 Nordstrom locations. This way, Allbirds gets access to Nordstrom’s customer base. Further, Nordstrom gets a reputation for taking on newer companies as well.

The value of novelty is hard to underestimate, especially for upscale shoppers who would likely love a shot of something new and different.

Further, Nordstrom is cutting off ties with Trunk Club in favor of more in-store advice, as well as some online operations as well. Meanwhile, the Nordstrom Half-Yearly Sale is drawing plenty of attention and is giving the company a head start on the latest quarter’s figures.

There are significant problems for Nordstrom, however. While it’s got the high-dollar consumer in place, it may not have them for long. Recessions hit everybody. While the higher-income consumer may have farther to fall, they may fall indeed, and that’s going to hit Nordstrom. There are, after all, fewer higher-income shoppers than there are lower-income.

Moreover, the mall business may be recovering from the pandemic, but it’s still well down, thanks to the growing numbers of competitors in the field. With inflation still on the rise, there’s also more incentive to scale down shopping from upscale locations.

Concluding Views

While certainly, Nordstrom has a solid friend in the upscale shopper, it’s unclear how long that friendship will hold in the face of rising inflation and worsening macroeconomics. With Nordstrom trading close to its lowest price target, however, some may be tempted to call this a good buy-in point and invest.

I’m bearish on Nordstrom because of two key factors. One, the best-case scenario isn’t that bright. The company continues appealing to the big spender. However, there are so few of them that it can only go so far.

Two, the worst-case scenario is a disaster. If those high-income shoppers go away, Nordstrom will lose its primary market base.

The outcome for Nordstrom is similar to a “Dilbert” strip. Dilbert remarks to the Pointy-Haired Boss that a certain project has a 70% chance of “minor success” and a 30% chance of “corporate ruination.” The Pointy-Haired Boss, meanwhile, enthusiastically signs off on the project, wishing he had “ten more like this one.”

No outcome looks that great for Nordstrom, and that prompts my bearishness.

Read full Disclosure