In a financial environment riddled with unprecedented levels of uncertainty, investors are at wits’ end. When it comes to finding an investment strategy that will yield returns, traditional methods might not be as dependable. So, how should investors get out of the rut?

In times like these, a more comprehensive stock analysis can steer investors in the direction of returns. Rather than looking solely at more conventional factors like fundamental or technical analyses, other metrics can play a key role in determining whether or not a particular stock is on a clear path forward.

TipRanks offers a tool that does exactly that. Its Smart Score measures eight key metrics including fundamentals and technicals while also taking into account analyst, blogger and news sentiment as well as hedge fund and corporate insider activity. After analyzing each metric, a single numerical score is generated, with 10 being the best possible result.

Using the Best Stocks to Buy tool, we were able to pour through TipRanks’ database, filtering the results to show only the names that have earned a “Perfect 10” Smart Score. We found seven that managed to tick all of the boxes. Let’s jump right in.

Limelight Networks, Inc. (LLNW)

Limelight Networks is best known for being a content delivery network (CDN) service provider, with its solutions enabling organizations to deliver digital assets that are fast, reliable and secure. With the growth story set to get even better, it’s no wonder LLNW has scored fans out on the Street.

Among the bulls is Northland Capital analyst Michael Latimore. After hosting a call with the company’s management team, he told clients that he walked away even more positive on the stock. “LLNW is a company with improving growth rates, expanding margins, and top tier customers; and getting a little help via work-from-home. We believe management remains confident in growth patterns, especially given new customers coming on board, and a healthy additional tailwind via work-from-home,” the analyst commented.

To support his bullish thesis, Latimore highlights the fact that going forward into Q2 and Q3, new customer launches should drive significant sequential growth, more so in full year 2021 than full year 2020. Online gaming updates as well as new sports content could also help propel the stock forward.

Latimore added, “Traffic related to work-from-home peaked at the end of March, but LLNW is managing more traffic than ever on a daily basis… LLNW has perfected its platform for OTT video and is in every conversation among new meaningful OTT video and live event providers.”

As its top 20 customers, which account for 77% of revenue, are financially sound, the deal is sealed for Latimore. To this end, the five-star analyst left an Outperform rating and $8 price target on LLNW, implying 51% upside potential. (To watch Latimore’s track record, click here)

Do other analysts agree with Latimore? As it turns out, they do. With 100% Street support, or 4 Buy ratings to be exact, the message is clear: LLNW is a Strong Buy. At $7.50, the average price target is less aggressive than Latimore’s, but still suggests 41% upside potential. See the LLNW stock analysis.

Krystal Biotech, Inc. (KRYS)

Using its STAR-D platform, Krystal Biotech develops and commercializes innovative therapies that target various dermatologic conditions. On the heels of its recent data release, some Wall Street pros believe that now is the time to snap up shares.

During the American Society of Gene & Cell Therapy (ASGCT) virtual meeting, the company presented positive in vitro preclinical data for replication-defective HSV-1-based gene therapy (GT), KB407, in cystic fibrosis (CF), the most common inherited genetic disorder in the U.S. Based on the update, the asset was able to infect small airway epithelial cells (SAECs) and generate a robust expression of functional, full-length human CFTR protein that properly traffics to the cell membrane.

Commenting on this result for Chardon Capital, five-star analyst Gbola Amusa stated, “This result suggests KB407 has overcome the issues of limited-capacity GT vectors not infecting the appropriate cells of the lungs.” He also pointed out that KB407 went head-to-head with Orkambi (G418) in relevant mutations, but also worked broadly on functional correction of the cystic phenotype of organoids.

Amusa added, “We thus see the KB407 in vitro data as a good start en route to Krystal testing KB407 for other issues that have held back GTs for CF, namely: (1) redosing (B-VEC data suggest Krystal’s vectors can be re-dosed), and (2) delivery (upcoming mouse nebulizer data will shed light).”

It should be noted that Vertex Pharmaceuticals is already well positioned within the space, but Amusa argues that a therapy for the 10% of CF patients with class I mutations, which cause the most severe phenotypes, still isn’t available, leaving the door wide open for KRYS.

Based on all of the above, Amusa calls the stock a Top Pick for 2020. Along with a Buy rating, the $100 price target remains unchanged. This target puts the upside potential at 89%. (To watch Amusa’s track record, click here)

What does the rest of the Street think about Krystal Biotech’s long-term growth prospects? It turns out that other analysts also have high hopes. Only Buy ratings, 6, in fact, have been received in the last three months, so the consensus rating is a Strong Buy. In addition, the $81 average price target indicates 53% upside potential. See the KRYS stock analysis.

Celsius Holdings, Inc. (CELH)

Celsius Holdings offers a portfolio of fitness drinks under the flagship CELSIUS brand that provide healthy energy while accelerating the metabolism and burning body fat. Following its Q1 2020 earnings release, the analyst community is singing its praises.

On May 12, CELH reported revenue of $28.2 million, which flew past the Street’s $13.4 million call and reflected a whopping 94.6% year-over-year gain. Up 660 basis points year-over-year, gross margin also surpassed the consensus estimate.

The driver of this impressive quarterly performance? Maxim Group’s Anthony Vendetti believes it was “the continued momentum and traction CELH is gaining as its products expand both nationally and abroad.” Even though he acknowledges that consumer purchasing behaviors have changed, the analyst highlights the fact that functional beverage demand is holding up strong.

In addition, COVID-19 played a role during the first quarter. “CELH has seen a surge in grocery deliveries and online orders and, in response, has stockpiled inventory and secured additional distribution and co-packer agreements. Additionally, the company has pivoted its marketing resources to digital programs, better reflecting the current macro environment. Although we believe that CELH has received a short-term sales bump from COVID-19, we remain positive in the long-term as the company continues to expand its distribution network and highlight itself as a ‘lifestyle brand,’ where active, routine customers continue to drive growth,” Vendetti explained.

All of the above combined with a compelling valuation prompted Vendetti to maintain a Buy recommendation. On top of this, the four-star analyst bumped up the price target from $8 to $12, bringing the upside potential to 33%. (To watch Vendetti’s track record, click here)

Looking at the consensus breakdown, 4 Buys and no Holds or Sells give CELH a unanimous Strong Buy analyst consensus. Not to mention the $11.31 average price target suggests 26% upside potential. See the CELH stock analysis.

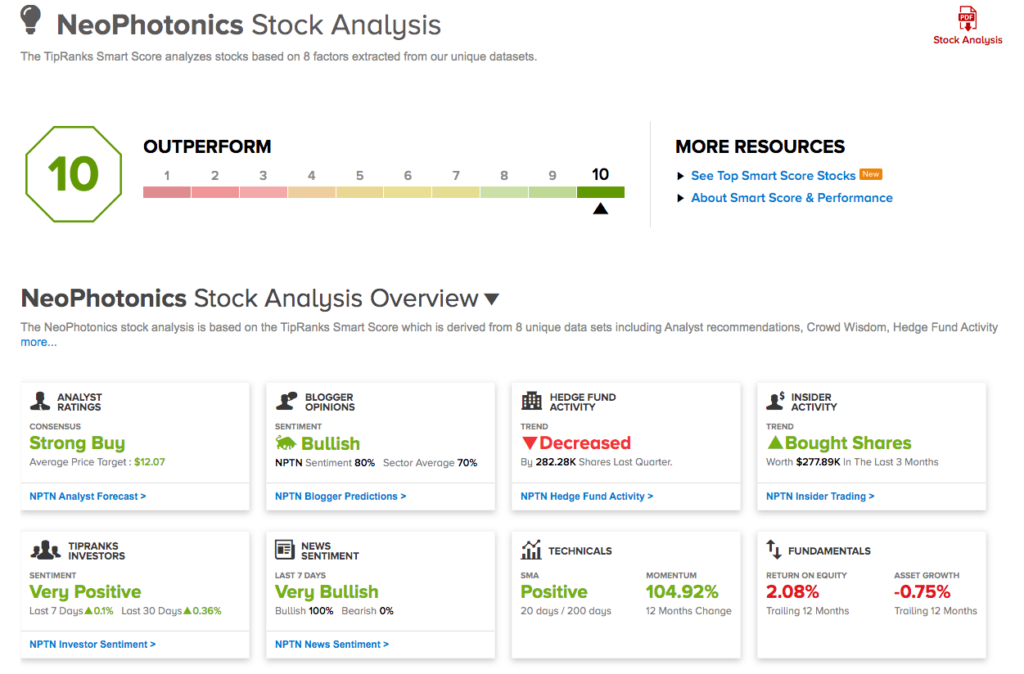

NeoPhotonics Corporation (NPTN)

NeoPhotonics is one of the top manufacturers of ultra-pure light lasers and optoelectronic products that transmit, receive and switch the highest speed over distance digital optical signals for cloud and hyper-scale data center internet content provider and telecom networks. After tuning in to the company’s recent webinar, one analyst thinks its future is bright.

Needham’s Alex Henderson cites a few key takeaways from the webinar discussing “Optical Technology Trends and Capacity in IP over DWDM”. “The primary points of the presentation is the shift to higher speeds and the emergence of standardization enabling Pluggables strengthens Neo’s competitive position should drive increased market share and improve margins,” he commented.

Part of what makes NPTN a stand-out, in Henderson’s opinion, is that it has a diverse product lineup that’s ready to accelerate in new arenas. It has also already been seeing traction with its more advanced capabilities. This translates to a significant competitive advantage for NPTN. Additionally, the company believes that its speeds will reach 400G and above, which will give it the chance to capture even more market share.

On top of this, the expansion into the C++ extended spectrum bands is producing design wins. Henderson explained, “Neo’s ability to use the same components and to take advantages of the ultra-clean signal enables Neo to offer as much as a 50% increase in spectral capacity using C++. This is an important advantage. Neo is already seeing considerable traction particularly in China for this technology.”

Taking all of this into consideration, Henderson stayed with the bulls. Along with a Buy rating, he reiterated a $12 price target. This target conveys the five-star analyst’s confidence in NPTN’s ability to surge 45% in the next twelve months. (To watch Henderson’s track record, click here)

In general, other analysts echo Hendersons’s sentiment. 7 Buys and 1 Hold add up to a Strong Buy consensus rating. A twelve-month rise of 45% could be in store if the $12.07 average price target is met. See the NPTN stock analysis.

Bunge Limited (BG)

Counting itself as the world’s largest soybean processor, Bunge Limited operates as an agribusiness and food company. Connecting farmers and consumers, the company is also involved in food processing, grain trading and fertilizer. Sure, 2020 has not been kind to this stock, with shares down 38% year-to-date, but several analysts see a turnaround on the horizon.

The recent negative sentiment surrounding BG can be attributed to its most recent quarterly performance. Looking at revenue, the figure came in at $9.2 billion, missing the consensus estimate by 8.6%. It also didn’t help that a loss of $1.46 per share was reported.

That being said, Baird analyst Ben Kallo is looking at the glass half full. Speaking to its recent portfolio optimization, the five-star analyst believes the company has “unlocked substantial value.” Additionally, the stock is trading at levels that are less than book value. As a result, he argues that now is the time for investors to “get more constructive on the longer-term earnings power story, enabled by BG’s leading (and underappreciated) asset footprint.”

It should also be noted that last week, BG declared a regular quarterly cash dividend of $0.50 per common share as well as a $1.22 per share quarterly dividend on its 4.9% cumulative convertible perpetual preference shares.

With everything that Bunge has going for it, it’s clear why Kallo is optimistic. Giving the stock a thumbs up, the analyst upgraded his rating from Neutral to Outperform. At $46, his price target suggests shares could climb 30% higher in the twelve months ahead. (To watch Kallo’s track record, click here)

Turning now to the rest of the Street, most other analysts are on the same page. Out of 4 analysts that have thrown an opinion into the mix, 3 were bullish, making the consensus rating a Strong Buy. To top it all off, the $57.50 average price target speeds past Kallo’s and brings the upside potential to 63%. See the BG stock analysis.

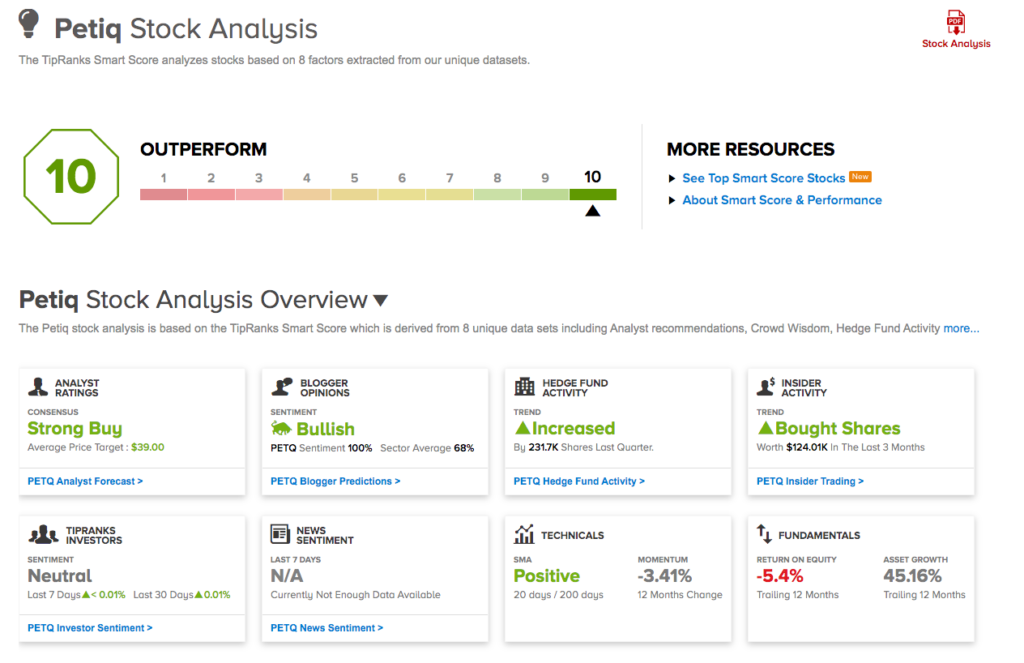

PetIQ, Inc. (PETQ)

Through retail channels across the U.S., PetIQ offers affordable pet health and wellness products as well as veterinary services. While the company, like the broader market, has been impacted by the COVID-19 pandemic, some analysts believe gains are in store post-virus.

Writing for Oppenheimer, five-star analyst Brian Nagel tells clients that PETQ is well-positioned to stage a post-COVID-19 rebound. “We are increasingly optimistic that the products and services businesses of PETQ should prove situated well to capitalize upon improved underlying consumer demand, given a recent surge in pet adoptions and rescues amid broad-based shelter in place orders across the U.S.,” he said.

Adding to the good news, PETQ just unveiled its telehealth platform. As part of the collaboration with whiskerDocs, prior PetIQ service customers will have access to various telehealth services, with a more comprehensive digital experience for new and existing customers coming later down the road.

To conclude, Nagel opined, “In our view, PETQ represents one of the most compelling, early stage small-cap growth stories to emerge in the consumer sector in a long while. A few key factors underpin our initial positive stance on the shares: 1) Potential for sustained, outsized topline expansion, owing to a still small market share, a unique consumer proposition, and favorable industry dynamics; 2) Already compelling free cash flow generation and the opportunity for rapidly expanding sales to leverage largely fixed operating expenses; and 3) An attractive valuation.”

It should come as no surprise, then, that Nagel kept an Outperform call and $50 price target on the stock. Given this target, shares could jump 73% in the next year. (To watch Nagel’s track record, click here)

Like Nagel, other analysts also like what they’re seeing. With 3 Buys and no Holds or Sells, the word on the Street is that the stock is a Strong Buy. In addition, the $39 average price target implies 35% upside potential. See the PETQ stock analysis.

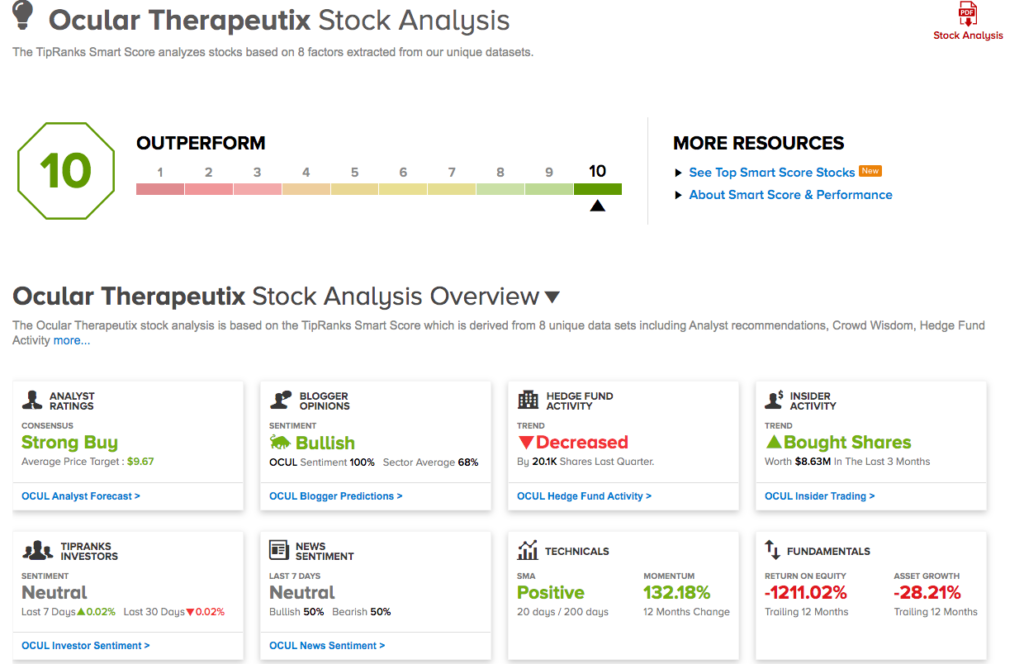

Ocular Therapeutix, Inc. (OCUL)

Last but not least on our list of Perfect 10s we have Ocular Therapeutix, which leverages its formulation expertise to develop cutting-edge treatments. With the company dosing the first patient in the Phase 1 open-label trial of OTX-CSI, its bioresorbable insert designed to release drug to the ocular surface for up to three months as a treatment of dry eye disease (DED), it’s clear why Wall Street focus has locked in on this healthcare name.

Looking more closely at the trial, it’s being conducted in a single center in the U.S., with it slated to enroll five patients and follow them for four months. As for why OCUL is garnering so much attention, it comes down to the design of the therapy.

OTX-CSI enables preservative-free delivery of a constant dose of cyclosporine, which could be less irritating than eye drop formulations. In addition, blocking the punctum may provide immediate relief for dry eye symptoms.

H.C. Wainwright analyst Yi Chen acknowledges that there’s already a treatment available for DED called RESTASIS, which generated sales of $1.1 billion in 2019. However, the analyst points out that the irritating side effects and slow onset of efficacy have led to high patient dropout rates.

Expounding on this, Chen stated, “In our view, an intracanalicular insert approach could be a better route of administration for chronic DED treatment; OTX-CSI could be less irritating and faster-acting compared to RESTASIS, in addition to eliminating the burden of twice-daily eye drop instillation required for RESTASIS.”

It should be noted that OCUL also faces competition from Oyester Point Pharma and its OC-01 candidate, but its recent data readout revealed lackluster levels of efficacy. “OC-01’s efficacy on DED symptom is a mixed bag at best, in our view, and neither dose met the symptom endpoint twice in the two studies. In addition, neither dose met the secondary symptom endpoint,” Chen mentioned.

All in all, Chen believes OCUL’s long-term growth prospects are strong. As a result, the five-star analyst reiterated a Buy rating and $10 price target, suggesting 39% upside potential. (To watch Chen’s track record, click here)

When it comes to other analysts, they take a similar approach. Two other analysts have published a review in the last three months, and both rated the stock a Buy, so the consensus rating is a Strong Buy. Based on the $9.67 average price target, the upside potential lands at 34%. See the OCUL stock analysis.

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.