The cannabis sector generally took a step back after Canopy Growth (CGC) reported a disastrous quarter last week. The Canadian cannabis giant set the sector back after cannabis was generally seen in a positive light coming out of the economic shutdown due to the coronavirus.

Invest with Confidence:

- Follow TipRanks' Top Wall Street Analysts to uncover their success rate and average return.

- Join thousands of data-driven investors – Build your Smart Portfolio for personalized insights.

While the U.S. cannabis space is poised for a strong 2H of the year, the sector wasn’t completely unscathed during the coronavirus shutdown. A few states such as Massachusetts and Nevada closed stores during the virus outbreak hitting revenues hard in those states.

While some of the large multi-state operators (MSOs) have rallied near pre-virus highs, the smaller MSOs are just now starting to rally. These stocks all trade with market values far below $1 billion and could eventually become acquisition targets from Canadian operators or new entrants into the space.

The ultimate gift for shareholders could exist from the Safe Banking Act getting approved via current legislature in the House as part of another round of stimulus. Over 34 state Attorney Generals approved the passage of the bill to eliminate the handling of cash, amongst other reasons. Access to capital will help these secondary MSOs to a greater extent than the larger ones.

With this in mind, we’ve delved into three under-the-radar MSO stocks to consider as the U.S. cannabis space is set to thrive during the economic reopening. Using TipRanks’ Stock Comparison tool, we were able to read the fine print on what 2020 has in store for the three MSO players.

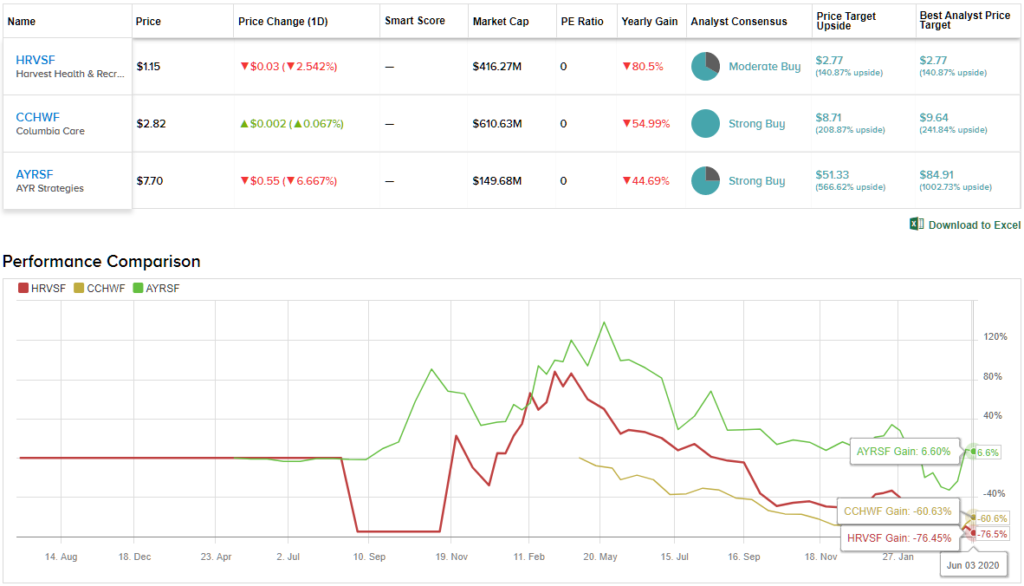

Harvest Health & Recreation (HRVSF)

Harvest Health & Recreation has been one of the most disappointing MSOs due to a couple of failed large-scale deals. The company has had to retreat from deals that would’ve placed Harvest Health into a leading MSO position, but the company is now focused on growing markets with recreational optionality in the future.

The company now has core operations in Arizona, Florida, Maryland and Pennsylvania. The Arizona operation has 14 open dispensaries with a good shot for the state approving recreational cannabis by the end of 2020.

For Q1, Harvest Health had $45.0 million in quarterly revenues with a 19% increase from the prior quarter. The cannabis MSO reported a small quarterly EBITDA loss of $3.9 million and expects to reach EBITDA positive in the 2H. Harvest Health needs to boost margins presently at 42%, but the company expects revenue growth and $6 million in quarterly expense cuts to drive the bottom line improvement.

The company targets over $200 million in 2020 revenues with the optionality of recreational cannabis in Arizona alone adding a boost of $50 million to the revenue base for 2021. The stock has a market cap of $405 million which could be very appealing in a scenario where any of their core states add recreational cannabis.

Harvest Health still trades near the lows of 2020 and far off the 2019 highs. The stock could easily trade below 2x actual 2021 sales assuming Arizona approves recreational sales in the November ballot.

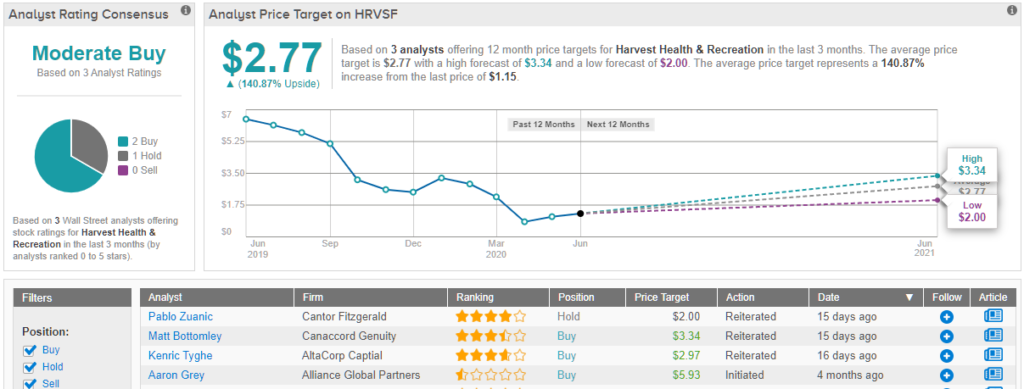

All in all, Wall Street is not convinced just yet on this MSO player, but optimism is circling, as TipRanks analytics demonstrate Harvest Health as a Buy. Based on 3 analysts polled in the last 3 months, 2 rate the stock a Buy, while 1 remains sidelined. The 12-month average price target stands at $2.77, marking a 141% upside from where the stock is currently trading. (See Harvest Health stock analysis on TipRanks)

Columbia Care (CCHWF)

Columbia Care remains one of the few MSOs not well known by the market. The company just reported Q1 results $28.9 million, up $4.4 million from the December quarter.

The MSO has strong operations in Florida, Illinois, Massachusetts and Ohio, amongst other states. In total, Columbia Care has licenses in 18 U.S. jurisdictions plus the E.U.

Between the Illinois store having business disruption recently due to COVID and Massachusetts shutting down recreational cannabis sales until last week, Columbia Care expects disrupted Q2 sales for areas just ramping up. As with Harvest Health, the MSO is positioned for the optionality of recreational approval in other states while having a relatively small revenue base.

For 2020, Columbia Care is forecasted to generate revenues of $210 million with a market cap of $620 million. More importantly, the MSO is expected to double revenues in 2021 to over $400 million before even seeing upside from a Florida approval of recreational cannabis in a few years.

The small MSO has $45 million in liquidity and $27 million in cash with the expectation for additional transactions later this year. Columbia Care is still generating large EBITDA losses as the company still launches operations in states such as New Jersey and Virginia.

Although the stock has only a few analysts currently throwing the hat in the ring, all are bullish on the stock. Columbia Care’s analyst consensus rating is a Strong Buy, with all 3 analysts giving it the thumbs up. The 12-month average price target stands at $8.71, which implies over 200% upside from current levels. (See Columbia Care stock analysis on TipRanks)

AYR Strategies (AYRSF)

One MSO actually hit by the coronavirus crisis was AYR Strategies. The company operates in both Massachusetts and Nevada where the states chose to close dispensaries or recreational sales.

For the March quarter, AYR Strategies reported revenues rose 4% to $33.6 million. The company was highly profitable heading into the mid-March COVID related closures in both Nevada and Massachusetts reduced sales towards the end of March. The company predicted sales would’ve risen by 16% sequentially in the quarter without the store closures.

The Q1 numbers weren’t hit hard with adjusted EBITDA still coming up at $8.4 million and cash flow of operations hitting $7.4 million. With Massachusetts blocking recreational cannabis until May 25, AYR Strategies forecasts June returning to the Q1 EBITDA levels with margins approaching 25%.

Analysts have AYR Strategies reaching $230 million in sales for 2021 while the stock valuation is only $152 million now. The stock trades at ~1x forward sales estimates while the industry as a whole trade closer to 3x forward sales.

The company only has $9.9 million in cash which could hold back investors, but the solid adjusted EBITDA position of the company should allow for AYR Strategies to easily raise cash in the future. Any approval of U.S. cannabis regulations would help this small MSO either raise cash or attract a suitor at premium prices.

All in all, AYR Strategies maintains a Strong Buy from the analyst consensus, based on 4 recent ratings. These include 3 Buys and 1 Hold, giving a 3 to 1 advantage to the bulls. Share are trading at $7.70, so the $51.33 average price target suggests room for whooping 567% upside. (See AYR Strategies stock analysis on TipRanks)

To find good ideas for cannabis stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclosure: No position.