Let’s talk portfolio defense. After last week’s social flash mob market manipulation, that’s a topic that should not be ignored.

Now, this is not to say that the markets are collapsing. After 2% losses to close out last week’s Friday session, this week’s trading kicked off with a positive tone, as the S&P 500 rose 1.5% and the Nasdaq climbed 2.5%. The underlying bullish factors – a more stable political scene, steadily progressing COVID vaccination programs – are still in play, even if they are not quite as strong as investors had hoped.

While increased volatility could stay with us for a while, it’s time to consider defensive stocks. And that will bring us to dividends. By providing a steady income stream, no matter what the market conditions, a reliable dividend stock provides a pad for your investment portfolio when the share stop appreciating.

With this in mind, we’ve used the TipRanks database to pull up three dividend stocks yielding 8%. That’s not all they offer, however. Each of these stocks has scored enough praise from the Street to earn a “Strong Buy” consensus rating.

New Residential Investment (NRZ)

We’ll start by looking into the REIT sector, real estate investment trusts. These companies have long been known for dividends that are both high-yield and reliable – as a result of company compliance with tax rules, that require REITs to return a certain percentage of profits directly to shareholders. NRZ, a mid-size company with a market cap of $3.9 billion, holds a diverse portfolio of residential mortgages, original loans, and mortgage loan servicing rights. The company is based in New York City.

NRZ holds a $20 billion investment portfolio, which has yielded $3.4 billion in dividends since the company’s inception. The portfolio has proven resilient in the face of the corona crisis, and after a difficult first quarter last year, NRZ saw rising gains in Q2 and Q3. The third quarter, the last reported, showed GAAP income of $77 million, or 19 cents per share. While down year-over-year, this EPS was a strong turnaround from the 21-cent loss reported in the prior quarter.

The rising income has put NRZ in a position to increase the dividend. The Q3 payment was 15 cents per common share; the Q4 dividend was bumped up to 20 cents per common share. At this rate, the dividend annualizes to 80 cents and yields an impressive 8.5%. In another move to return profits to investors, the company announced in November that it had approved $100 million in stock repurchases.

BTIG analyst Eric Hagen is impressed with New Residential – especially by the company’s sound balance sheet and liquidity.

“[We] like the opportunity to potentially build some capital through retained earnings while maintaining a competitive payout. We think the dividend increase highlights the strengthening liquidity position the company sees itself having right now… we expect NRZ has been able to release capital as it’s sourced roughly $1 billion of securitized debt for its MSR portfolio through two separate deals since September,” Hagen opined.

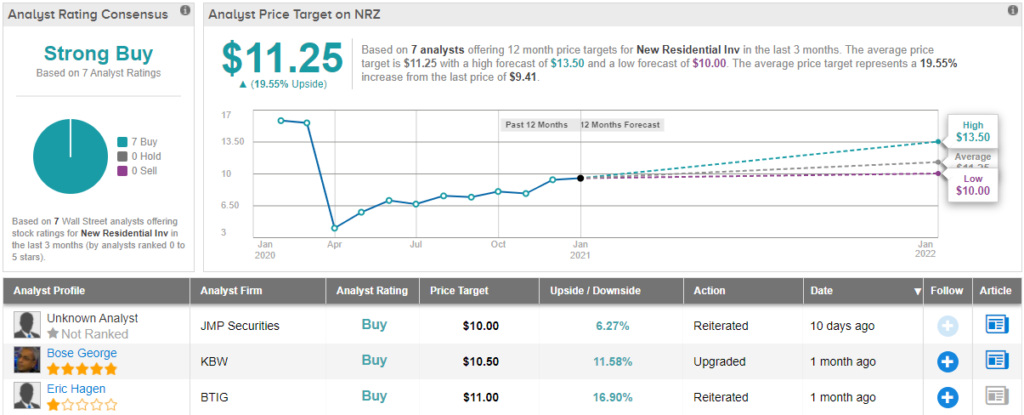

In line with his comments, Hagen rates NRZ a Buy, and his $11 price target implies an upside of 17% for the year ahead.

It’s not often that the analysts all agree on a stock, so when it does happen, take note. NRZ’s Strong Buy consensus rating is based on a unanimous 7 Buys. The stock’s $11.25 average price target suggests ~20% upside from the current share price of $9.44. (See NRZ stock analysis)

Saratoga Investment Corporation (SAR)

With the next stock, we move to the investment management sector. Saratoga specializes in mid-market debt, appreciation, and equity investments, and holds over $546 million in assets under management. Saratoga’s portfolio is wide ranging, and includes industrials, software, waste disposal, and home security, among others.

Saratoga saw a slow – but steady – rebound from the corona crisis. The company’s revenues fell in 1Q20, and have been slowly increasing since. The fiscal Q3 report, released early in January, showed $14.3 million at the top line. In pre-tax adjusted terms, Saratoga’s net investment income of 50 cents per share beat the 47-cent forecast by 6%.

They say that slow and steady wins the race, and Saratoga has shown investors a generally steady hand over the past year. The stock has rebounded 163% from its post-corona crash low last March. And the dividend, which the company cut back in CYQ2, has been raised twice since then.

The current dividend, at 42 cents per common share, was declared last month for payment on February 10. The annualized payment of $1.68 gives a yield of 8.1%.

Analyst Mickey Schleien, of Ladenburg Thalmann, takes a bullish view of Saratoga, writing, “We believe SAR’s portfolio is relatively defensive with a focus on software, IT services, education services, and the CLO… SAR’s CLO continues to be current and performing, and the company is seeking to refinance/upsize it which we believe could provide upside to our forecast.”

The analyst continued, “Our model anticipates SAR employing cash and SBA debentures to fund net portfolio growth. We believe the Board will continue to increase the dividend considering the portfolio’s performance, the existence of undistributed taxable income, and the economic benefit of the Covid-19 vaccination program.”

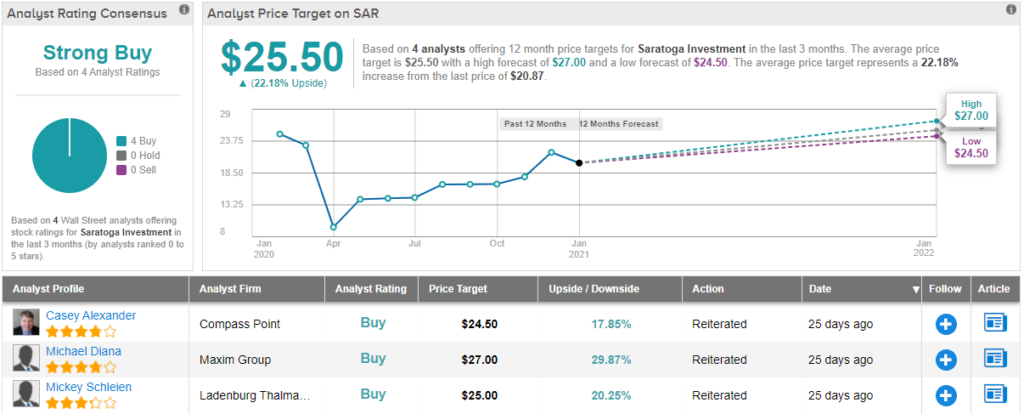

To this end, Schleien rates SAR a Buy along with a $25 price target. This figure implies a 20% upside from current levels. (To watch Schleien’s track record, click here)

Wall Street’s analysts agree with Schleien on this stock – the 3 other reviews on record are Buys, and the analyst consensus rating is a Strong Buy. Saratoga’s shares are trading for $20.87, and carry an average price target of $25.50, suggesting an upside of 22% for the next 12 months. (See SAR stock analysis on TipRanks)

Hercules Capital (HTGC)

Last but not least is Hercules Capital, a venture capital company. Hercules offers financing support to small, early-stage client companies with scientific bent; Hercules’ clients are in life sciences, technology, and financial SaaS. Since getting started in 2003, Hercules has invested over $11 billion in more than 500 companies.

The quality of Hercules’ portfolio is clear from the company’s recent performance. The stock has bounced back fully from the corona crisis of last winter, rebounding 140% from its low point reached last April. Earnings have also recovered; for the first nine months of 2020, HTGC posted net investment income of $115 million, or 11% higher than the same period of 2019.

For dividend investors, the key point here is that the net investment income covered the distribution – in fact, it totaled 106% of the base distribution payout. The company was confident enough to boost the distribution with a 2-cent supplemental payment. The combined payout gives a $1.28 annualized payment per common share, and a yield of 8.7%.

In another sign of confidence, Hercules completed a $100 million investment grade bond offering in November, raising capital for debt pay-downs, new investments, and corporate purposes. The bonds were offered in two tranches, each of $50 million, and the notes are due in March of 2026.

Covering the stock for Piper Sandler, analyst Crispin Love sees plenty to love in HTGC.

“We continue to believe that HTGC’s focus on fast growing technology and life sciences companies sets the company up well in the current environment. In addition, Hercules is not dependent on a COVID recovery as it does not have investments in “at-risk” sectors. Hercules also has a strong liquidity position, which should allow the company to act quickly when it finds attractive investment opportunities,” Love commented.

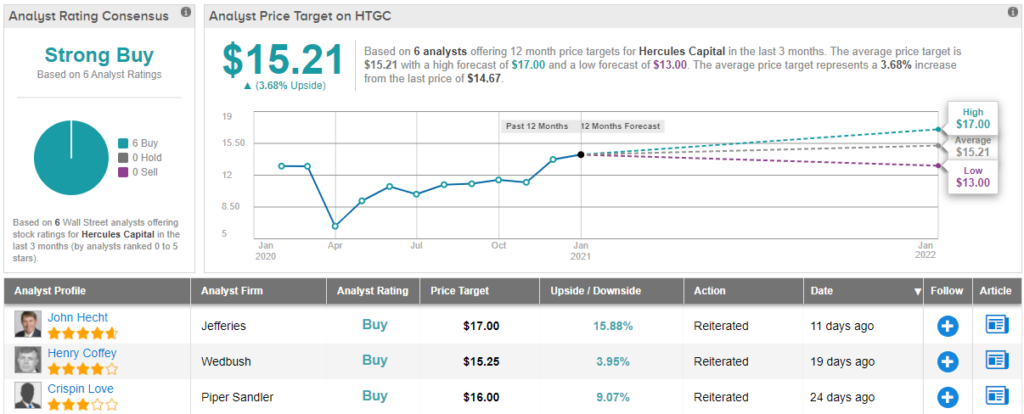

All of the above convinced Love to rate HTGC an Outperform (i.e. Buy). In addition to the call, he set a $16 price target, suggesting 9% upside potential. (To watch Love’s track record, click here)

Recent share appreciation has pushed Hercules’ stock right up to the average price target of $15.21, leaving just ~4% upside from the trading price of $14.67. Wall Street doesn’t seem to mind, however, as the analyst consensus rating is a unanimous Strong Buy, based on 6 recent Buy-side reviews. (See HTGC stock analysis on TipRanks)

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.