The markets have been on a tear of late despite the headwinds presented by the novel coronavirus pandemic. The question is how long this will last?

Writing from Goldman Sachs, the firm’s chief US equity strategist David Kostin says that the markets will outperform both other investments and analyst expectations over the next two years. He sees the S&P 500 hitting 4,600 by the end of 2022, which would represent a 25% gain.

Backing his stance, Kostin gives four reasons for his bullishness. The first three reasons are the obvious ones: the economy is improving, earnings are rising, and interest rates are low – these all draw investors into stocks. But under them all is ‘Tina’ (there is no alternative).

The stock market is the only place right now where investors can find big returns and, according to Kostin, “equities become the default opportunity.”

With investors moving into stocks, they’re going to look for data to back their choices. After all, even without an alternative, investors want to find the right moves.

With this in mind, we used TipRanks database to pinpoint three stocks with a Strong Buy consensus rating, and a Perfect 10 Smart Score.

The Smart Score is a data analysis tool, which uses the real-time information collected in the database. The stock data is collated according to 8 separate factors, each of which is known to predict growth and share appreciation. The factors are averaged together, and given as a single-digit score, on a scale from 1 to 10, letting investors know at a glance the likely way forward for a stock.

The Strong Buy rating and the Perfect 10 don’t have to go together, but it’s a strong positive sign for investors when they do. Let’s take a closer look.

Turning Point Brands (TPB)

Turning Point may not be a household name – but there’s a good chance that you’ve heard of some of its brands. The company owns both Zig Zag, the well-known maker of rolling papers and branded gear, and Stoker’s chewing tobacco. Turning Point has a range of ‘consumer products with active ingredients,’ including chewing tobacco, as well as snuff and vapes.

The company registered an earnings increase from 4Q19 to 1Q20, bucking the corona trend, and has seen quarterly revenues level out at $104 million in Q3, up 15% from the first quarter. Earnings have been rising consistently for the past three quarters, with Q3 EPS at 75 cents.

The company’s stock has been rising, too. Shares in TPB are up an impressive 50% year-to-date, wiping out all losses sustained during the shutdown policies last winter.

Covering this stock for Craig-Hallum is 5-star analyst Eric Des Lauriers. He rates TPB shares a Buy, and his $60 price target suggests room for 41% growth in the coming year. (To watch Des Lauriers’ track record, click here)

Backing his bullish stance, the analyst writes, “Turning Point Brands (TPB) delivered another strong beat and raise quarter, beating all analyst estimates as the two base businesses benefitted from long term secular trends and growth initiatives… [We] expect the strong trends in the base businesses to continue through 2021 and expect significantly increased profitability in NewGen as competitors exit the market. With strategic investments and M&A picking up, we are increasingly bullish on TPB’s long-term outlook…”

Overall, the Strong Buy consensus rating on Turning Points Brands is unanimous, standing on 5 Buy-side reviews. The stock is selling for $42.60, and its $46.46 average price target implies ~9% upside from current levels. (See TPB stock analysis on TipRanks)

Gladstone Lands (LAND)

Next up is a unique REIT, real estate investment trust. Gladstone owns and manages farmland, acquiring high-quality farms and related properties which it then leases to independent farmers or to farming corporations. The company’s properties are actively involved in the production of a wide range of crops, including strawberries, raspberries, blueberries, cabbage and watermelons. Gladstone boasts 100% occupancy of its properties, an enviable position for any REIT.

During the first quarter, when most companies felt the pain of the lockdown policies, Gladstone posted its strongest earnings and revenues of 2020. The most recent results, for Q3, showed revenue of $13.99 million, up 10% sequentially. Since the third quarter, Gladstone has acquired four new farms, totaling nearly 1,400 acres, and collected 99% of rents due in October. Even better, for shareholders, to company’s portfolio has exceeded $1 billion in total value.

Like most REITs, Gladstone pays out a regular dividend. The payment, of 4.4 cents per regular share, is paid out monthly. At an annualized rate of nearly 53 cents per share, it gives a yield of 3.6%.

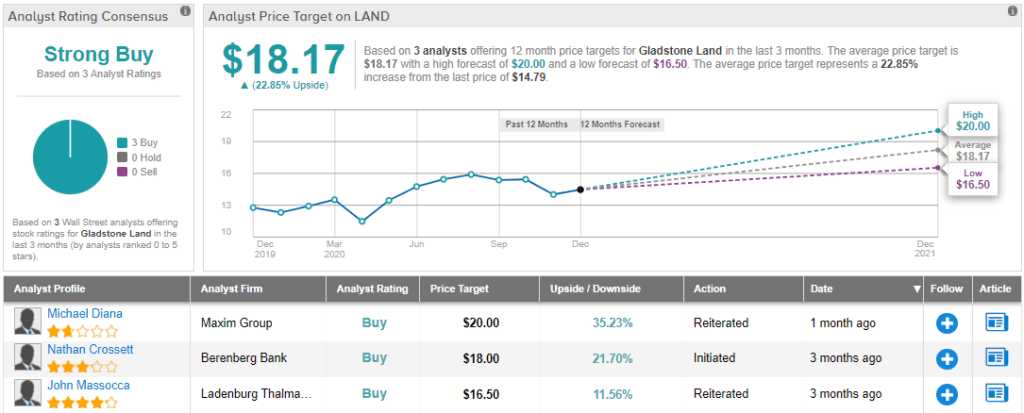

Among the bulls is Maxim analyst Michael Diana who wrote, “We have covered LAND since it went public in January 2013, and have consistently regarded its investment thesis (appreciation in the value of farmland) as sound, its strategy (focused mainly on non-commodity crops such as fruits and vegetables) as superior, and its execution (buying high quality farms at reasonable cap rates) as strong.”

To this end, Diana gives LAND a Buy rating and a $20 one-year price target, which indicates room for 35% growth. (To watch Diana’s track record, click here.)

Overall, along with its Strong Buy consensus rating, LAND shares have a 12-month average price target of $18.17. This suggests an upside potential of ~23% in the year ahead. (See LAND stock analysis at TipRanks)

MarineMax (HZO)

The last stock on our list is a retailer, in the water-leisure niche. MarineMax sells boats, yachts, and support services such as winterization, new and used, across the spectrum of price points. The company advertises itself as recreational retailer focused on premium brands.

HZO has seen strong appreciation in 2020, bucking the coronavirus. The shares are up 89% year-to-date, far outpacing the NASDAQ and S&P 500.

The share growth has been based on powerful results for the company’s fiscal year, which ended on September 30. In the fiscal Q4, just reported, EPS was down sequentially, but beat the forecast by a wide margin. Quarterly revenue came in at $398 million. Fiscal 2020 full-year revenue was $1.5 billion, and reflected 25% same-store sales growth during the year. EPS for fiscal 2020 was $3.37, more than double the previous year’s figure.

When a company reports results like that, it’s no surprise to see it has a Perfect 10 from the Smart Score.

B. Riley analyst Eric Wold is impressed by MarineMax’s same-store sales and its overall position in its retail niche. He writes, “HZO reported impressive 4Q20 SSS growth of +33%, which was up against a two-year comp stack of +13%, and compared to our +25% estimate and the consensus estimate of +14%. We believe the company’s broad network of retail locations, strong manufacturer relationships and investments into a digital/virtual platform can help the company take meaningful share—and even in situations where most are shutdown during a pandemic.”

In line with his comments, Wold gives the stock a Buy rating. His $40 price target implies an upside of ~27% over the next year. (To watch Wold’s track record, click here)

All in all, MarineMax’s Strong Buy consensus rating is based on 6 reviews, breaking down to 5 Buys and 1 Hold. The stock is selling for $31.53, and its $35.80 average price target suggests it has room to grow 13.5% from that level. (See HZO stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.