There are plenty of fundamentally sound, low cost stocks out there for retail investors to consider. The key to success is to find stocks that are at or near the bottom of their cycle.

Don't Miss Our Christmas Offers:

- Discover the latest stocks recommended by top Wall Street analysts, all in one place with Analyst Top Stocks

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

Equity investment advisors will always tell you that ‘timing the market’ is impossible, and they’re right – but timing is still important for success. Investors need to buy into low prices, and to do that, they need to know when prices are low. This doesn’t necessarily mean low in absolute dollar terms, but low relative to a stock’s recent past performance.

In recognizing that lower price range, investors can turn to Wall Street’s pros for help. The analysts have been busy lately, picking out stocks that are in their lower price range, and are flirting with the bottom.

We’ve used the TipRanks database to look up three such stocks, Strong Buys with strong upside potential for the next few months – and each one is trading at or near its one-year low. Let’s take a closer look.

Oportun Financial Corporation (OPRT)

We’ll start in the financial services sector. Oportun is a digital banking platform that uses AI to back up inclusive, affordable financial services for more than 1.5 million members. The company’s customers can access savings, banking, investing services, including short-term loans and credit. The company offers alternatives to high-risk credit services such as payday and auto-title loans; Oportun’s customers can access personal loans between $300 and $10,000 with repayment terms between 1 and 4 years, and can apply for credit cards with limits between $300 and $1,000. Oportun has been in business since 2009, and in that time provided over $12 billion in affordable credit.

Personal banking and credit services targeted at the lower end of the consumer financial market has become big business, and a look at Oportun’s recent performance bears this out. The company reported $194 million in quarterly revenue for 4Q21, and the quarter’s aggregate loan originations rose 93% to $865 million. For the full year 2021, these numbers reached $627 million and $2.3 billion – both company records. The company reported adjusted earnings of 82 cents per share, up 36% year-over-year, and well above the 72-cent forecast.

Nevertheless, Oportun’s share price has fallen by 46% from the peak it reached in November of last year.

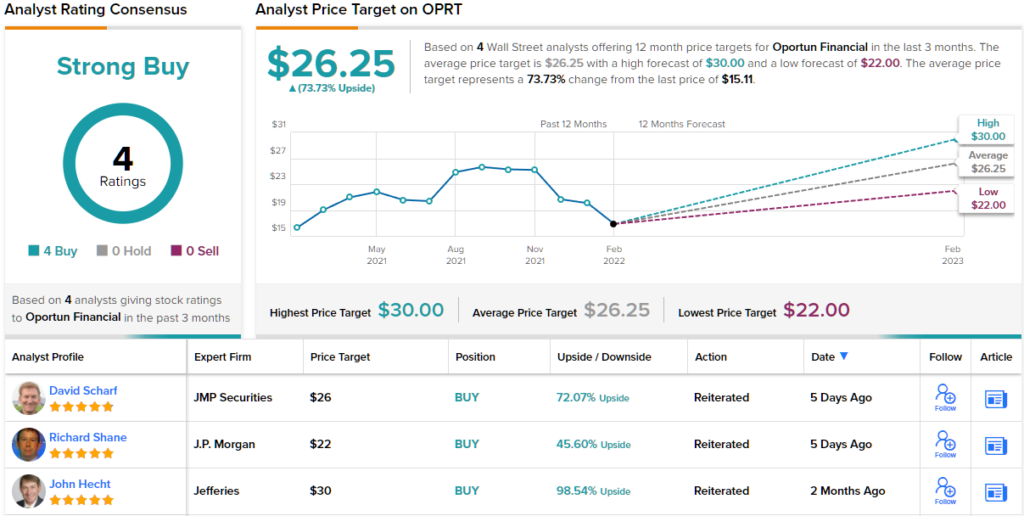

This doesn’t mean that the stock is unsound. 5-star analyst David Scharf, of JMP, takes an upbeat view of Oportun, writing: “Exiting 2021, we believe that Oportun represents one of the best positioned and most compelling growth stories in our Consumer Finance coverage… Our sense is that the company’s significant geographic, product, and channel expansion over the course of the past two years has been lost amid the broader investor focus on the pandemic and the related credit normalization that is underway. Yet OPRT’s management has been quietly and steadily building a diverse and comprehensive subprime platform…”

Backing his optimistic view of the company, Scharf assigns the shares an Outperform (i.e. Buy) rating, and his $26 price target implies a robust upside of ~72% for the coming year. (To watch Scharf’s track record, click here)

Overall, all 4 of the recent analyst reviews on OPRT are positive, making a unanimous Strong Buy consensus rating, and the $26.25 average price target indicates potential for ~74% upside from the trading price of $15.11. (See OPRT stock forecast on TipRanks)

Altra Industrial Motion (AIMC)

We may live under the digital economy, and the financial and cyberspace sectors may drive much of what happens around us, but the physical world makes demands that cannot be avoided – and that is where Altra Industrial Motion comes in. This company manufactures motion control and power transmission products, for a wide range of sectors: cranes and hoists, the oil and gas industry, robotics and factory automation, precision motors, and medical and surgical tools. Altra produces a full range of equipment to control speed, torque, positioning, and braking, at every scale imaginable. The company operates in 17 countries and has over 48 production facilities.

In its most recent quarter, 4Q21, Altra reported $469.8 million at the top line, flat sequentially but up a modest 3.7% year-over-year. While sales were slightly up, EPS was down. The reported non-GAAP earnings, at 67 cents per share, were down almost 12% y/y. On a positive note, the company also reported a record backlog, indicating high potential for future business, and guided toward full-year 2022 revenue in the range of $2.025 billion to $2.065 billion – which would translate to a 7.6% y/y gain at the midpoint.

In a couple of recent organizational moves, Altra has taken action to emphasize its strengths and shed some weaknesses. The company entered an agreement to sell its JVS (Jacobs Vehicle Systems) business to Cummins for $325 million. This sale price was 40% higher than JVS’ share of the 2021 revenues. And, in January, Altra completed its acquisition, for an undisclosed sum, of Nook Industries, a leader in engineered linear motion. Nook showed approximately $42 million in revenue last year.

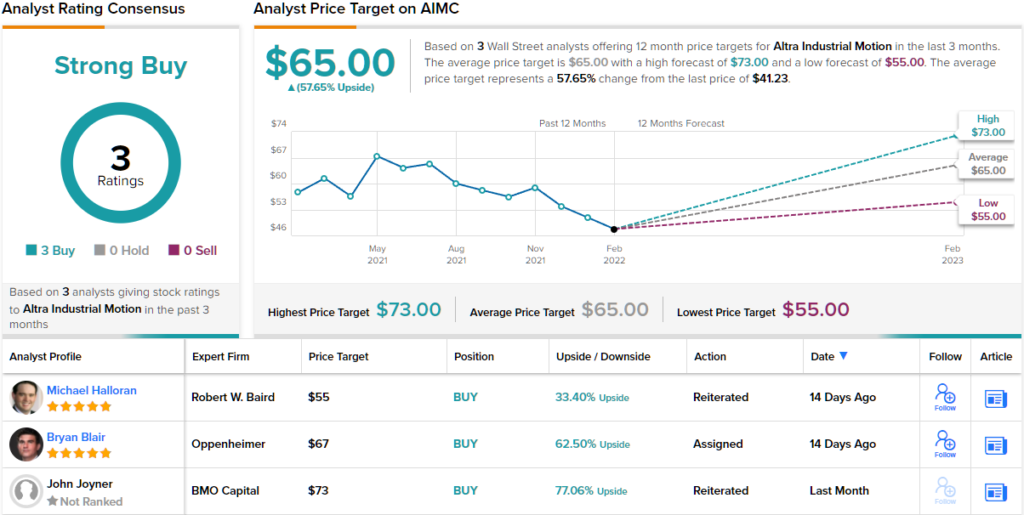

Altra shares have been falling steadily for the past 12 months; the stock is down 32% in that period. However, Oppenheimer’s 5-star analyst Bryan Blair points out the stock’s potential for a rebound, saying: “We believe valuation now excessively discounts Altra’s business quality (including the fourth-highest EBITDA margins across IMFC coverage), the favorable positioning of its overall portfolio (with underappreciated exposure to factory automation, material handling/e-commerce, infrastructure, and medical technologies), and the through-the-cycle earnings power of combined PTT/A&S operations (supporting normalized FCF generation solidly >$250M). We view the stock’s eye-catching valuation discount (notably >10 points on P/E) as disconnected from fundamentals, highlighting AIMC as a compelling value play.”

To this end, Blair gives AIMC an Outperform (i.e. Buy) rating, along with a $67 price target that suggests an upside of 63% over the next 12 months. (To watch Blair’s track record, click here)

While only three analysts have weighed in on Altra, their unanimous agreement gives the stock its Strong Buy consensus rating. The shares are priced at $41.23 and have an average target of $65, for ~58% upside potential in the next 12 months. (See AIMC stock forecast on TipRanks)

Axalta Coating Systems (AXTA)

We’ll wrap up with another industrial stock, this one in something of a ‘leisure/luxury’ niche. Axalta, headquartered in Philadelphia, has produced and marketed a wide range of color and coating solutions for industrial and consumer use for the past 150 years. The company is particularly noted as provider of automotive coatings – paint jobs – but its full product line includes liquid and powder coatings for vehicles in the commercial, industrial, and agricultural sectors as well.

In the past year, Axalta has seen revenues rise while earnings came under pressure. The company’s top line hit $1.14 billion in 4Q21, up 6% year-over-year and the best result in two years. For 2021 as a whole, revenues were reported at $4.42 billion, an 18% gain over the ‘COVID year’ of 2020, and indicative of a solid recovery.

At the same time that revenue numbers are up, earnings have been slipping in recent quarters. Q4’s 30-cent adjusted EPS was down by almost half from the 58-sent EPS reported in the year-ago quarter. As a result, Axalta’s shares are down 20% so far this year.

All may not be gloom for this industrial paint company, however, as BMO analyst John McNulty writes: “Conservative expectations/estimates, pricing accelerating while raw materials level, and continued strength in its end-markets, have AXTA poised to deliver in the near term. With a thin valuation, this execution should yield solid upside in the stock and help AXTA to ‘break out’ of the perpetual upper $20s/low $30s range it has held for the last five years. The risk/reward remains one of the most compelling in the sector…”

Unsurprisingly, McNulty rates AXTA an Outperform (i.e. Buy), and his $40 price target shows the stock’s potential for ~53% upside in the months ahead. (To watch McNulty’s track record, click here)

Axalta is a high-profile company, and has picked up 9 analyst reviews in recent weeks. These break down to 7 Buys and 2 Holds, for a Strong Buy analyst consensus. AXTA shares are selling for $26.13 and have an average price target of $35.56, giving the stock ~36% upside potential. (See AXTA stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.