The professional corps of Wall Street stock analysts is 7,500 strong and growing. Collectively, they present us – every day – with comprehensive reviews on the full list of publicly traded stocks. Their information is invaluable for investors of all stripes – but how to figure out whose advice is worth trusting?

Don't Miss Our Christmas Offers:

- Discover the latest stocks recommended by top Wall Street analysts, all in one place with Analyst Top Stocks

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

The top analysts on Wall Street stand head-and-shoulders above their peers, with more accurate stock ratings and higher returns on the equities they recommend. And for now, Heiko Ihle, of investment firm H.C. Wainwright, holds the number 2 spot out of those 7,500 stock pros.

Ihle is an expert in the Basic Materials sector, an economically vital branch of the markets. Let’s see what he has to say about these three Strong Buy mining stocks.

Largo Resources (LGO)

Rare-earth metals are key ingredients of a host of products in today’s technological world. One of these metals, vanadium, is well-known for both its rarity and its application to a host from products. From high-grade steel to high-yield batteries, vanadium has a place in multiple industries. The metal is expensive, with the European price of vanadium pentoxide flakes (a common industrial form of the metal) running at more than US$8 per pound.

Largo Resources, the first stock we’re looking at, is both a miner and refiner of vanadium. The company has one mine, the Maracas Menchen mine in Brazil, that produces vanadium, with 2021 production projected to be between 12,000 and 12,500 tons. This ore is processed into a variety of products by Largo, including the company’s VPure and VPure+ lines. These include pure metal in flake or powder form, as well as the industrially useful vanadium pentoxide alloy. Largo will begin production of vanadium trioxide, used in steel and titanium alloying, later this year.

Largo’s revenue and income can vary quarter to quarter and year over year, based on market demand and mine production. In 1Q21, the company saw $4.1 million in net income, compared to $4.3 million one year ago. Per share, this came to 7 cents, compared to 8 cents in the year-ago quarter. At the top line, revenue was $39.8 million, down 4% from 1Q20.

Heiko Ihle, in his note on Largo, comes to a bullish conclusion: “Largo continues to sell products with prices based on different V2O5 and ferrovanadium benchmarks, as demand within all of its key markets remained strong during the quarter. In particular, we highlight that the company experienced sales volume improvements from the steel and chemical industries…. We highlight the company’s strategy on developing new markets for its high-purity products, while simultaneously focusing on expanding sales into the growing vanadium redox flow battery (VRFB) market…”

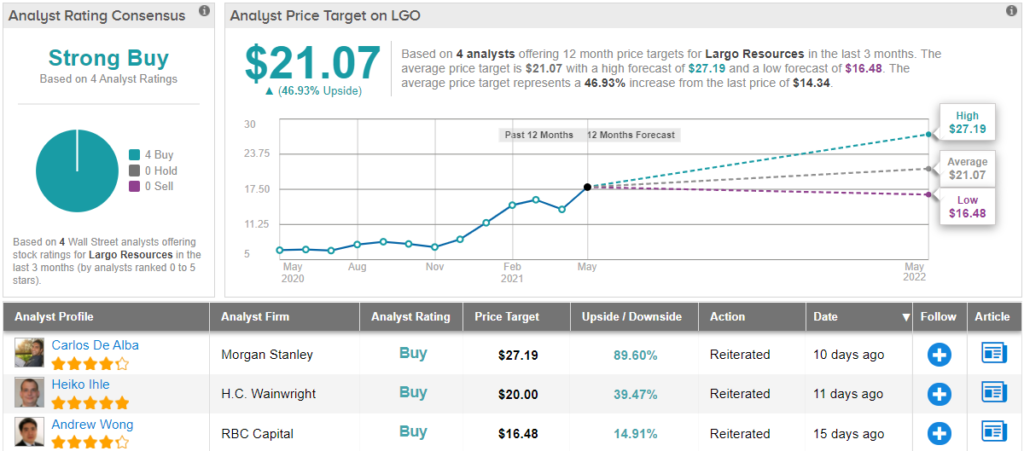

In line with these comments, Ihle rates LGO a Buy along with a $20 price target. Should his thesis play out, a potential upside of ~40% could be in the cards. (To watch Ihle’s track record, click here)

Overall, there are 4 recent reviews on record for LGO and all are Buys – making the analyst consensus rating a unanimous Strong Buy. Shares are priced at $14.34 and the average price target of $21.07 indicates ~47% upside potential from that level. (See LGO stock analysis on TipRanks)

Uranium Energy (UEC)

Next up, Uranium Energy, is a US-based mining and exploration company of – you guessed it! – uranium. This is a pure-play miner, meaning it focuses solely on uranium. The company is working to promote lower-cost and more environmentally-friendly uranium mining, on the ISR, or in-situ recovery, model. UEC has uranium recovery projects in Wyoming, Colorado, Arizona, New Mexico, and south Texas. The company’s top production capacity is over 4 million pounds of uranium oxide per year.

The company has a ‘physical uranium initiative,’ a project to gather and safely warehouse a large store of uranium ore. Currently, the initiative has over 2.1 million pounds warehoused, and is fully funded. The company acquired an additional 200,000 pounds of uranium in May of this year.

Reporting on this stock, Ihle notes that the company has multiple paths for continued profits.

“Going forward, we maintain our longer-term expectation that current global developments throughout the uranium market should drive higher future prices that could eventually support favorable production decisions at one or more of UEC’s properties. Additionally, any market improvements should greatly benefit the company’s liquidity given growth in UEC’s inventory,” Ihle wrote.

The analyst continued, “Looking ahead and towards the company’s development and production potential, we highlight that the Burke Hollow property already holds all four major required permits for uranium extraction. Finally, we expect the physical uranium purchasing initiative to eventually add incremental value through higher future uranium prices…”

Overall, Ihle believes this is a stock worth holding on to. The analyst rates UEC shares a Buy, and his $5 price target suggests a solid upside potential of 52%. (To watch Ihle’s track record, click here)

This small-cap company has attracted 3 recent stock reviews. All are positive, making for unanimous Strong Buy consensus rating. UEC shares have an average price target of $4.08 and a share price of $3.29, giving the stock a 24% one-year upside. (See UEC stock analysis on TipRanks)

Sierra Metals, Inc. (SMTS)

Last on our list of Heiko Ihle picks is Sierra Metals, an Ontario-based small-cap mining company with operations in Mexico and Peru. Sierra focuses its exploration and production on copper, lead, and granodiorite stone, along with small amounts of gold and silver. While only the gold and silver are precious metals, the company’s non-precious metals find a ready market in a variety of industries.

Sierra’s active operations currently include three mines, one in Peru and two in Mexico, along with no fewer than 16 exploration properties. During the first quarter of 2021, the company reported production of 7.9 million pounds of copper, 9 million pounds of lead, and 2,636 ounces of gold. These metals all showed year-over-year decreases in output, which was compensated by increased production of other ores. Metals showing a yoy increase were zinc, to 24.1 million pounds, and silver, to 1 million ounces. The company attributed the lower gold production to a reduction in the mining areas of that metal, so as to focus on higher-purity ores during the labor restriction of the COVID pandemic crisis.

In its Q1 financial report, Sierra reported total revenue of $69.6 million, up 25% year-over-year and demonstrating that the increased production was zinc and silver did make up for lower production in copper, lead, and gold. Net income for the quarter, at $3.1 million or 2 cents per share, was a solid turnaround from the $1.9 million loss recorded in 1Q20.

In his coverage of this stock, Heiko Ihle wrote: “Looking ahead, Sierra continues to place a strong importance on avoiding any mine closures and hitting production targets despite operational difficulties seen in 1Q21 due to COVID-19. In addition, the company intends to continue working on the completion of Preliminary Feasibility Studies for its three mines, thereby building upon the positive Preliminary Economic Studies released in FY20. Finally, we expect management to continue building on its recent brownfield exploration successes, as Sierra simultaneously looks to improve its costs at all three of its mines.”

To this end, Ihle rates the stock a Buy, and his $4.25 price target implies room for 19% growth in the next 12 months.

In general, the rest of the Street is on the same page. 3 Buy ratings in the last three months give SMTS a ‘Strong Buy’ analyst consensus. At the $4.48 average price target, shares could surge ~25% over the next twelve months. (See SMTS stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.