Penny stocks, you either love them or you hate them. One of the obvious draws of these stocks trading for under $5 per share is the ability to get more bang for your buck. And should these bargain priced stocks see their share prices rise by only a small amount, the rewards can be staggering.

Don't Miss our Black Friday Offers:

- Unlock your investing potential with TipRanks Premium - Now At 40% OFF!

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

However, before jumping right into an investment in a penny stock, Wall Street pros advise looking at the bigger picture and considering other factors beyond just the price tag. For some names that fall into this category, you really do get what you pay for, offering little in the way of long-term growth prospects thanks to weak fundamentals, recent headwinds or even large outstanding share counts.

Taking the risk into consideration, we used TipRanks’ database to find compelling penny stocks with bargain price tags. The platform steered us towards three tickers sporting share prices under $5 and “Strong Buy” consensus ratings from the analyst community. Not to mention substantial upside potential is on the table.

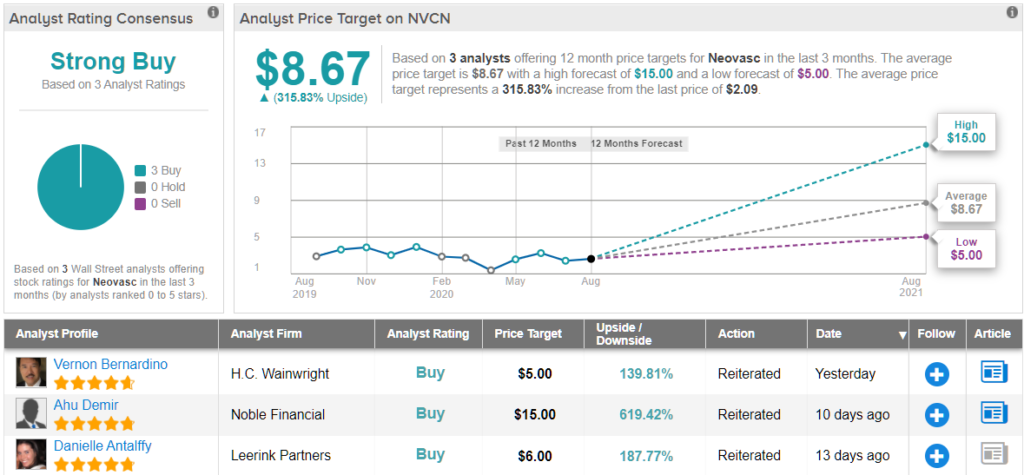

Neovasc Inc. (NVCN)

Operating as a specialty medical device company, Neovasc develops and manufactures cutting-edge products for the cardiovascular space. As it gears up for an FDA panel, several members of the Street are pounding the table on this name, which trades for $2.10 per share.

On October 27, the FDA will hold a circulatory system devices panel meeting to review the premarket approval application for NVCN’s Reducer device, which was submitted in December 2019 for the treatment of patients suffering from refractory angina pectoris who are ineligible for revascularization by coronary artery bypass grafting (CABG) or by percutaneous coronary intervention (PCI).

Writing for Leerink, 5-star analyst Danielle Antalffy likes what she has been seeing. Now that the meeting has been confirmed, Antalffy argues it “essentially implies that FDA views the existing Reducer clinical data as sufficient for approval.” The analyst added, “… we are now increasingly confident that Reducer could secure a U.S. approval in the near-term and launch in early 2021. Given that the NVCN story has been so laser-focused on the Tiara TMVR (Transcatheter Mitral Valve Replacement) device, the Reducer opportunity has been understated and underappreciated by both us and investors, and now this could become a much more meaningful revenue contributor over the medium-term than we are currently thinking.”

Looking more closely at the product, the Reducer is an hourglass-shaped stent-like device that raises blood pressure in the coronary sinus, which increases blood flow to the heart muscle. As for the market opportunity, management estimates that it lands at roughly 250,000 procedures globally, assuming ~25% of the patients underwent PCI (~1 million procedures worldwide per year) for refractory angina, with 50% of the patients in the U.S.

Having said that, it hasn’t been entirely smooth sailing for the company as Reducer sales were negatively impacted by the pandemic. However, Antalffy points out that beginning in June, there has been a “more rapid than anticipated” recovery in Reducer implants. Key regions like Germany, Austria and Switzerland have hit pre-COVID implant and revenue targets. “Management expects the significant backlog of procedures to drive volume growth in 2H20 granted the current COVID situation does not worsen/cause significant impact to elective procedures,” the analyst added.

To this end, the top analyst rates NVCN an Outperform (i.e. Buy) along with a $6 price target. Should her thesis play out, a potential gain of 188% could be in the cards. (To watch Antalffy’s track record, click here)

Are other analysts in agreement? They are. Only Buy ratings, 3, in fact, have been issued in the last three months, so the consensus rating is a Strong Buy. Given the $8.67 average price target, which is more aggressive than Antalffy’s, shares could skyrocket 315% in the next year. (See NVCN stock analysis on TipRanks)

VolitionRx (VNRX)

Using its Nucleosomics technology, VolitionRX offers a range of tests designed to change the way cancer and other conditions are diagnosed. Even though COVID-19 has impacted the company’s development pipeline, multiple analysts believe that at $3.48, its share price presents an opportunity to get in on the action.

Maxim analyst Jason McCarthy notes that like many of its peers, VNRX has been affected by the pandemic. Part of the problem is that its clinical development activities are taking place throughout the world. Therefore, with international travel limited and the global supply chain dispersed, several large-scale “flagship” studies have been delayed along with the initial CE marking for the CRC and lung triage assays.

However, the 5-star analyst applauds VNRX’s response to these headwinds, pointing out that the company has taken advantage of the ATM and conducted a public offering to raise funds. As a result, he estimates that VNRX has about $23-$24 million in cash, which should support its operations into 2H21.

In addition, VNRX has been focusing on the portion of the development pipeline that is in its control. “The Nu.Q vet program remains on track for launch later this year. The company has also continued work on moving assays over to the magnetic bead format, with 13 completed to date (beating the target of 12), out of 20 targeted for YE20. Additionally, Volition is working on a COVID-19 prognostic test, which could make it to market in 2021,” McCarthy noted.

The COVID-19 prognostic test was designed to detect elevated levels of Neutrophil Extracellular Traps (NETs), which are produced by white blood cells and are comprised of chromatin in nucleosome form. These NETs have been found to catch and trap invading viruses. In severe cases of COVID-19, a hyperimmune response is present which causes a large infusion of NETs into the blood that are very damaging to the lungs, resulting in conditions like ARDS, the leading cause of death in COVID patients. “This represents a differentiated approach since there are a number of tests for detecting COVID, but a prognostic test could help better allocate hospital resources and direct treatment,” McCarthy said.

With the company already having demonstrated initial proof-of-concept that nucleosomes are elevated in COVID-19 patients, especially in those requiring mechanical ventilation, McCarthy sees significant potential. “The trial should have the data collected by September 2020, with a release planned for Q4 2020. This could position Volition to have a CE mark by YE20, with a product to launch shortly afterwards. The pathway in the U.S. is expected to take slightly longer, but could potentially receive funding from BARDA, CEPI, or Operation Warp Speed,” he stated.

Based on all of the above, McCarthy rates VNRX a Buy along with an $8 price target. This target puts the upside potential at a whopping 138%. (To watch McCarthy’s track record, click here)

Other analysts don’t beg to differ. 4 Buy ratings and no Holds or Sells have been assigned in the last three months. Therefore, VNRX is a Strong Buy. The $7.25 average price target implies shares could climb 115% higher in the coming year. (See VNRX stock analysis on TipRanks)

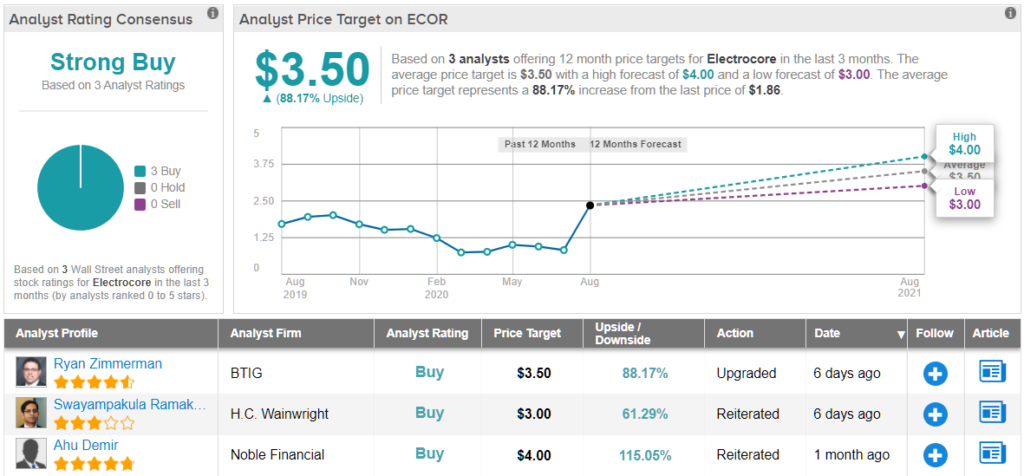

electroCore (ECOR)

Last but not least is electroCore, which uses non-invasive vagus nerve stimulation (nVNS) to develop new treatments for patients suffering from pain and chronic conditions. Currently going for $1.86 apiece, this name could see major gains, according to some analysts.

Representing BTIG, 5-star analyst Ryan Zimmerman tells clients that excitement surrounding ECOR’s COVID application has fueled some major share price appreciation recently. The company has two ongoing investigator-initiated trials, SAVIOR-1 in Spain and SAVIOR-2 in Pittsburgh.

Additionally, ECOR agreed to support a clinical trial with the VA system to treat COVID-19 patients in an outpatient setting (and prior to any hospital submission). This will be organized by the Hampton, Virginia VA Medical Center, with data from this trial as well as SAVIOR-1 and 2 set to come in the next 12 months. Even though this program could be a revenue driver, Zimmerman argues “the real value for longer-term investors lies in a radically improved and refocused organizational structure that has taken a few quarters to emerge.”

Looking at its gammaCore product, it has held up relatively well during the pandemic, with only a minor sequential reduction in paid months of therapy witnessed, given that it can be prescribed easily during a telehealth consult and delivered directly to a patient’s home. On top of this, while pharmacies have been filling between 300-500 paid months of therapy per quarter during the first two quarters of 2020, prescriptions were being delivered from inventory purchased by a distributor in 2019.

“This inventory has now been worked through, and management expects to ship at least 200 paid months of therapy per quarter in Q3 2020 and Q4 2020 (~$80,000 per quarter by our estimate). As we look into Q3, we think the fact that ECOR shipped 435 paid months of therapy in July compared to an average of 329 per month in the Q2 points to a nice sequential increase in revenue,” Zimmerman commented.

Wrapping it all up, Zimmerman stated, “We think shares have the potential to move higher over coming quarters based on these dynamics and the investments ECOR is now able to make to further enhance its commercial opportunities. Looking ahead, we see multiple value-creating events in clinical data readouts and publications, quarter-over-quarter revenue growth in key customer channels, and potential upside from COVID patient adoption.”

In line with his optimistic take, Zimmerman rates ECOR a Buy and set a $3.50 price target, which implies a potential upside of 88%. (To watch Zimmerman’s track record, click here)

Overall, the bulls have it. ECOR’s Strong Buy consensus rating breaks down into 3 Buys and no Holds or Sells. In addition, the $3.50 average price target matches Zimmerman’s. (See electroCore stock analysis on TipRanks)

To find good ideas for penny stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.