Stocks are on the rise, but why? The glum results of earnings season have not caused another panic – rather, investors seem to be taking them in stride as ‘baked in’ to the current financial situation. The indexes are generally holding steady, at resistance levels Wall Street had predicted two weeks ago. And this brings up the questions, How long will this last? and What will happen next?

Weighing in from Morgan Stanley, chief US equity strategist Michael Wilson believes that stocks hit their true bottom on March 23. In his view, the coronavirus and the collapse in oil markets simply marked the end of the last US market expansionary cycle, and that the current rally has potential to develop into a true recovery. The relatively flat trading of the last few weeks is, in Wilson’s opinion, the market’s first break after a “torrid 35% rally from the lows.”

Wilson cites several factors in support of his stance. In particular, he notes that stock markets typically lead an economic recovery by as much as two quarter – and that economists are predicting a general recovery to begin in 2H20. If they are correct, then the March 23 market trough and current rally would fit that pattern. Wilson also points to the enormous support and stimulus being offered by central banks and governments as a move that will benefit the equity markets.

As a first step toward the next bull run, Wilson has advised his clients to buy into small-cap stocks. These companies typically fly under-the-radar, getting less notice from Wall Street – a quirk that sometimes helps them weather storms. We’ve taken Wilson’s advice as part of a profile, and used the TipRanks database to pull up three micro-cap penny stock companies with super-low entry costs (a dollar per share or less) and huge upside potential (greater than 90% in the year to come). Here are the details.

Great Panther Silver (GPL)

The first stock on our list is mining company Great Panther Silver. Most of Great Panther’s operations are located in Mexico, but the company also has an active mine in Brazil and exploration operations in Peru. The company focuses on gold and silver production. Great Panther has been in a time of transition, with a new CEO and top management team.

Overall production has taken a hit from the COVID-19 pandemic. GPL reported that two workers at its Brazilian mine are confirmed to have the disease, and while they are now quarantined, the site’s mining operations remain at full capacity. In Mexico, production was halted through April 30 on orders from the Mexican government, and that order has since been extended to May 30. The Mexican Topia mine, located in a locality that has not experienced any coronavirus cases, may be able to reopen early, on May 18. Great Panther’s Peruvian operation is on hold until July.

Despite the setbacks in production caused by the pandemic, Great Panther reported a 134% year-over-year increase in Q1 gold production, with output reaching 35,000 gold equivalent ounces. Silver production reached 393,000 equivalent ounces, for an 11% year-over-year increase. The high production complements a strong cash position – GPL reported $37 million in cash on hand at the end of 2019. The production numbers and cash position are welcome news, and reflect well on the new management team.

Reviewing this stock for Cantor Fitzgerald, analyst Matthew O’Keefe sees a clear path forward, based on fine exploration opportunities. “We continue to highlight exploration as a key upside for the Company. Exploration expenditures of approximately $7 … are primarily focused on near mine drilling activities intended to replace gold ounces mined in 2020. These activities are ongoing, and we expect that a significant amount of the drilling to be completed by the end of Q3/20. We continue to see excellent potential here,” he commented.

O’Keefe puts a Buy rating on GPL, along with a $1.10 price target that indicates 134% upside potential. (To watch O’Keefe’s track record, click here)

The Wall Street analyst corps clearly agrees with O’Keefe on GPL’s potential. The stock gets a Strong Buy rating from the analyst consensus, and it is unanimous, based on 3 recent Buy reviews. GPL is a penny stock, and sells for only 47 cents per share. The average price target is slightly more bullish than O’Keefe’s, at $1.15 per share, and it suggests an upside potential of 145% for the next 12 months. (See Great Panther Silver price targets and analyst ratings on TipRanks)

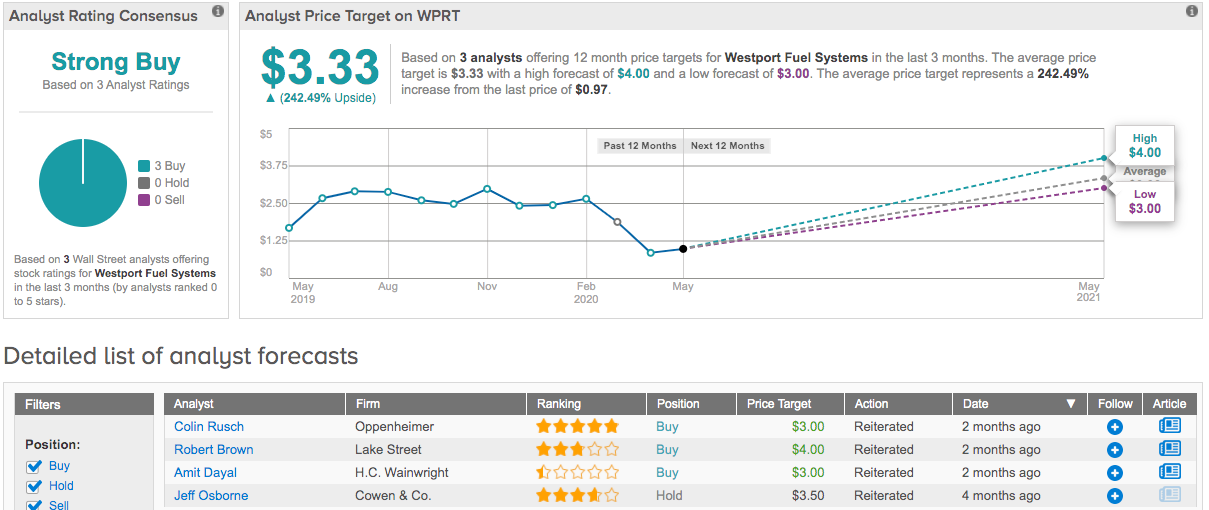

Westport Fuel Systems, Inc. (WPRT)

Next on our list is a company involved in clean transportation technology. Westport engineers and produces natural gas engines, along with fuel system components for passenger cars and on- and off-road commercial vehicles. The company is a leader in high pressure direct injection (HPDI) technology.

The coronavirus pandemic was hard on Westport in Q1. The company’s Italian manufacturing facility was forced to shut down, and only resumed operations on May 4. Looking ahead, the company is expected to report a Q1 net loss of 5 cents per share come June. On positive note, Westport faces these difficulties after a year of growing revenues and earnings in 2019, culminating in Q4’s break-even EPS – much better than the 1-cent loss predicted, and far better than the year-ago quarter’s 8-cent loss. Revenues were up 23% year-over-year in Q4, and reached $74.3 million.

5-star analyst Colin Rusch, of Oppenheimer, is optimistic that WPRT can weather this storm. He writes, “We believe the company is being prudent in declining to provide guidance given the clear uncertainty around the coronavirus containment efforts, particularly in Europe… We believe working capital management will be critical for WPRT as it navigates lower volumes for a period of time along with compressed margins. We remain constructive despite near-term headwinds.”

Rusch’s comments support his Buy rating on this stock. He gives WPRT shares a $3 price target, which indicates confidence – and a 209% upside potential for next 12 months. (To watch Rusch’s track record, click here)

Craig-Hallum’s Eric Stine is even more bullish on WPRT. The four-star analyst points out that the company will receive support from governments in Europe and Canada, and goes on to outline why the company has a strong future ahead. “With the shift to alternative fuels driven by straightforward economics and the competitive advantage gained, we believe that Westport Fuel Systems is at very early stages of a meaningful growth ramp,” he explained.

Stine places a $5 price target on this stock, to support his Buy rating. His target implies a whopping one-year upside potential of 415%. (To watch Stine’s track record, click here)

Westport Fuel is another company with a unanimous Strong Buy analyst consensus view. The rating is based on 3 Buy reviews set recently, and comes with an average price target of $3.33. This suggests room for an impressive 242% upside potential. (See Westport stock analysis on TipRanks)

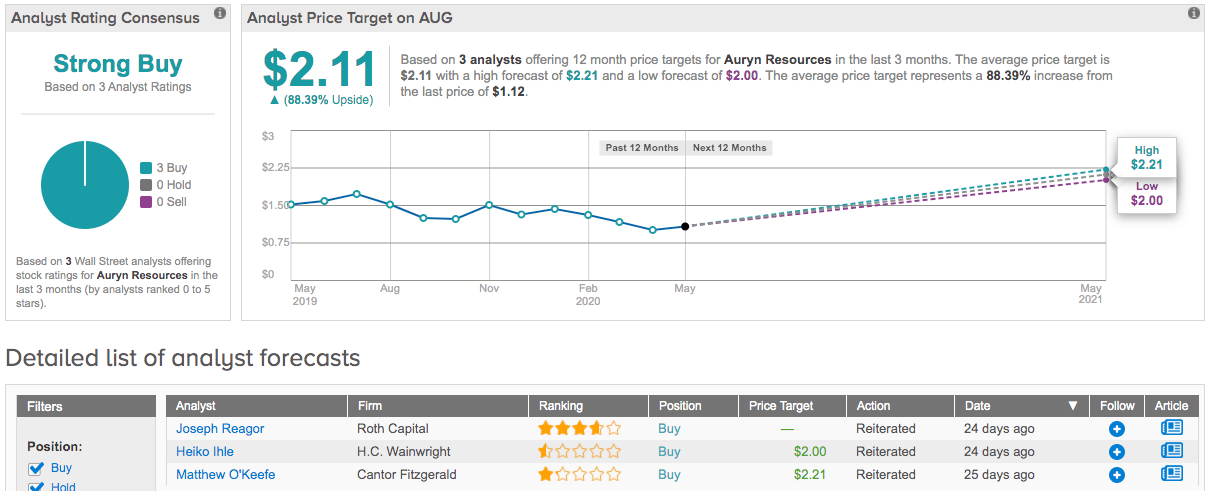

Auryn Resources, Inc. (AUG)

Our last stock is another mining company, operating in the Canadian North as well as in Peru. Auryn focuses on producing copper and high-grade gold. Working in the Arctic or the Peruvian mountains entails high overhead, and AUG operates at a net loss – but the loss has been narrowing steadily since 2H18. Even taking coronavirus disruptions into account, AUG is expected to show a further reduction in the net loss per share for Q1 2020.

In additional good news, Auryn enhanced its financial position at the end of 2019, securing C$10.1 million ($7.22 million US) in funding by closing its private placing offering. The sale closed just as Auryn also improved its interest rates on existing loans. These improvements to the balance sheet gave the company a firm footing just before the disruptions caused by COVID-19 occurred.

And finally, Auryn has also released the Preliminary Economic Assessment of the Canadian Homestake Ridge project. This assessment shows that the property has the potential to become a profitable, high-grade, small-footprint underground gold mine. The company estimates the new mine will produce up to 88,660 gold equivalent ounces when it reaches peak production, three years after opening, and will have a production lifetime of 13 years.

Joseph Reagor, 4-star analyst with Roth Capital, sees Auryn as a solid stock to buy, and bases his recommendation on the high potential of the Homestake mine. Ironically, Reagor believes the company can secure maximum value by not directly operating this asset: “We believe that AUG is likely to either sell Homestake or spin it out and merge it with a junior producer. Each of these outcomes would likely result in a premium valuation…”

Reagor places a Buy rating on AUG shares, and his $3.25 price target suggests an upside potential of 190%. (To watch Reagor’s track record, click here)

With a Strong Buy analyst consensus rating, based on 3 Buy reviews, it’s clear that Wall Street is in agreement with Reagor about this stock’s potential. The Street is a bit more cautious, however; the average price target on this stock is $2.11, which implies an upside potential of 88% from the current share price of $1.12. (See Auryn Resources price targets and analyst ratings on TipRanks)

To find good ideas for penny stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.