The stock market is heating up again, and some Wall Street pros see the light at the end of the tunnel. Among those adapting a bullish approach is Wells Fargo’s head of equity strategy, Chris Harvey, who believes the worst is behind us, freeing up the S&P 500 to continue its ascent.

“Typically the first impact is generally the worst impact. We’re sticking to this belief that the worst is over, that we’re going to be able to mitigate it […] Obviously it’s not all unicorns and rainbows, and we’ll have pullbacks from time to time. But we think the pullbacks will be shallow.”

Bearing this in mind, some investors are on the hunt, looking to snap up compelling names before shares re-embark on an upward trajectory. For the more risk-tolerant, focus has locked in on penny stocks, or tickers trading for less than $5 per share. The appeal is clear; the bargain price tag means you can get more bang for your buck and even what feels like inconsequential share price appreciation can result in huge percentage gains.

What’s the flip side? Minor share price depreciation can fuel major percentage losses. By nature of these massive movements, penny stocks are notoriously volatile.

With an understanding of the risk at play, we’ve used TipRanks’ database to pull the vitals on three penny stocks that have recent gotten the thumbs up from Wall Street’s analysts. All get a Strong Buy from the consensus view, and their upside potentials start at 100%. Let’s see what else makes them so compelling.

Synchronoss Technologies (SNCR)

We’ll start in the world of e-commerce. Synchronoss develops online vendor platforms, and helps customers create solutions for finding new revenue, reducing costs, and improving the buyer experience, and increasing site visitor engagement.

Synchronoss has been posting an enviable record on earnings – for three quarters in a row, including Q1 2020, the ‘coronavirus quarter,’ the company has shown sequential gains in EPS and beaten the estimates by wide margins.

An aggressive marketing strategy towards big-name commercial sites is paying off for Synchronoss, several analysts believe that at $3.07 per share, now is the time to pull the trigger.

Among them, Michael Walkley, 5-star analyst from Canaccord, stands out. He writes of SNCR, “With several Cloud deals starting to ramp including AT&T, continued growth potential at Verizon that experienced low-teens subscriber growth in 2019, progress on blue-chip DXP and IoT partnerships with Amazon, Rackspace, AT&T and others, and strong annual RCS revenue contributions anticipated from the CCMI deal, we believe there are several strong building blocks…”

“We believe the current <1x 2021E EV/revenue valuation levels versus peers at ~3x present a compelling entry point for investors,” Walkley concluded.

To this end, Walkley rates the stock a Buy, and his $10 price target implies an amazing 225% one-year upside to the stock. (To watch Walkley’s track record, click here)

Overall, three 5-star analysts have rates SNCR a Buy recently, making the analyst consensus on this stock a Strong Buy. Even the average price target suggests room for an impressive upside; at $8.50, it predicts 176% growth from the current share price. (See SNCR stock analysis on TipRanks)

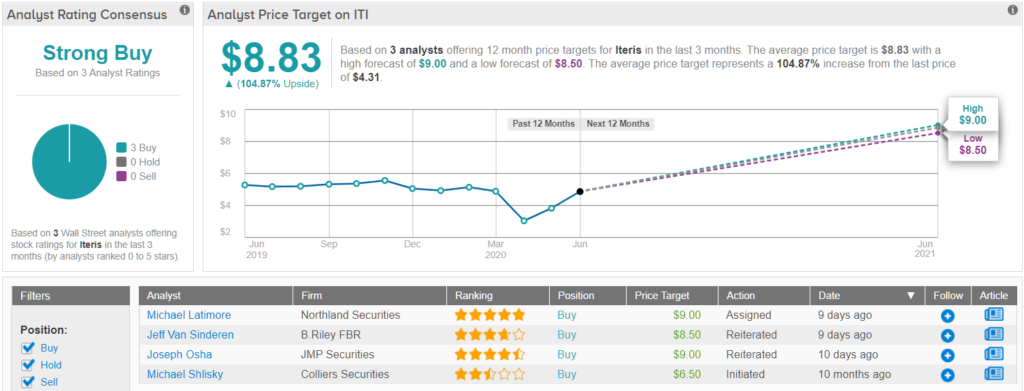

Iteris (ITI)

Next up is Iteris, a tech company which uses cloud computing systems, AI apps, advanced sensors, and managed services to predict both weather and traffic patterns, allowing clients to optimize transportation infrastructure to maximize efficiency and safety. Iteris boasts a consulting relationship with the Federal Government, as well as several states and numerous local agencies.

Having government as a client is nice work if you can get it, and Iteris has reported consistently rising revenues for the past year. The most recent quarter, Q1, showed $30.9 million at the top line, or 18% year-over-year growth. EPS, which shown a consistent 5-cent net loss for the previous three quarters, turned sharply upward to a 1-cent net profit in 1Q20. ITI’s position is only enhanced by the announcement, earlier this month, that the company has signed on as a sub-contractor with the State of Georgia Department of Transportation.

B.Riley FBR analyst Jeff Van Sinderen was particularly impressed by Iteris’ ability to withstand the recessionary pressures of the coronavirus pandemic. He writes, “ITI quickly adapted to remote working conditions early as the COVID-19 threat unfolded and minimized disruptions during 4Q while accelerating certain commercial activities. Some of this adaptability was possible solely because of the company’s software-enabled delivery model. The integration of AGI into the systems business in Florida, the Midwest and the MidAtlantic has continued successfully…”

Van Sinderen backs his Buy rating on ITI with an $8.50 price target, showing his own confidence in a 97% upside from the current share price of $4.31. (To watch Van Sinderen’s track record, click here)

The analyst consensus on ITI is just as bullish. Three out of three recent reviewers rated the stock a Buy, making the analyst consensus a unanimous Strong Buy. The average price target is slightly higher than Van Sinderen’s; at $8.83, it suggests a 104% upside for the coming 12 months. (See Iteris stock analysis on TipRanks)

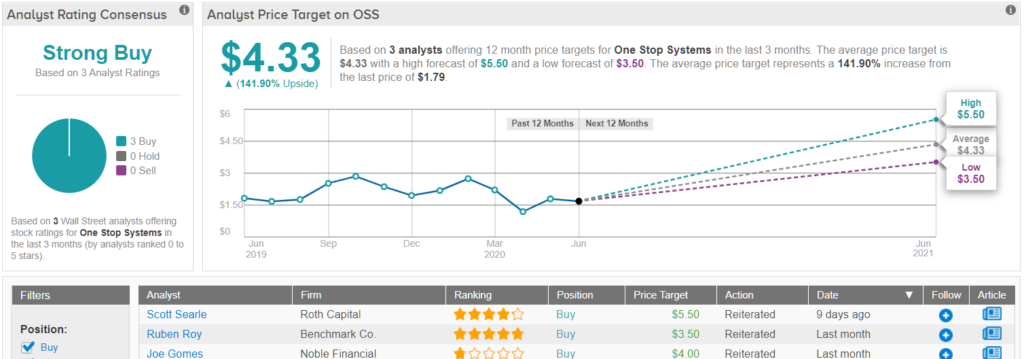

One Stop Systems (OSS)

Last on our list is One Stop Systems, a tech company specializing in high-performance computers (HPCs) in markets requiring the world’s fastest data processing and storage capacities. The applications include AI, deep learning, seismic research, financial modeling, and security and defense. One Stop offers systems for both single-HPC servers and rack-scale multi-HPC server deployments. The company’s record of success includes designing server systems for complex defense, manufacturing, and telecom clientele.

In the past three months, OSS has reported over $6.6 million in new sales, and for the quarter ending March 31 showed 33% year-over-year in revenues, to a total of $13.3 million. At $3.4 million, gross profits represented 25.4% of the total revenues. These strong results came even as the company is in the midst of a management transition, with CEO Steve Cooper stepping down this past February, and David Raun stepping up in an interim capacity.

With a price tag of $1.79 per share, some members of the Street believe the share price reflects an attractive entry point.

Covering the stock for Roth Capital, analyst Scott Searle was impressed by the company’s agility during the management transition. He wrote, “…we believe that OSS is taking meaningful strides under interim CEO Dave Raun. Notably, increased transparency, op-ex optimization and improved liquidity appear to be an early indicator for other changes as illustrated by a record pipeline of 27 large opportunities which continue to diversify the historically concentrated sales base.”

To this end, Searle rates OSS a Buy, while his $5.50 price target implies a hefty upside potential of 207% for the coming year. (To watch Searle’s track record, click here)

All in all, OSS shares rate a Strong Buy from a unanimous analyst consensus. Three reviewers have given approval of this stock in the past month. Meanwhile, the average price target of $4.33 implies a robust 142% one-year upside. (See OSS stock-price forecast on TipRanks)

To find good ideas for penny stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.