The coronavirus pandemic hasn’t gone away; there’s a growing realization that the virus will be with us, at least, for some time to come. An increase in cases has revived fears of a lockdown – although US Treasury Secretary Mnuchin has tried to allay those fears, stating that the US cannot afford another national lockdown. The month of May saw great news in the jobs report and the retail sales numbers, but international travel restrictions are still in place. While we’ve started reopening, it’ll be a long road back to normal.

Don't Miss Our Christmas Offers:

- Discover the latest stocks recommended by top Wall Street analysts, all in one place with Analyst Top Stocks

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

Which all makes dividend stocks a logical play. Return-minded investors can find a degree of safety in high-yielding equities, as the dividend will insulate the portfolio’s income stream. And even though dividend stocks tend to return less on share appreciation, there are still plenty out there that are showing high upside potential.

We’ve turned to TipRanks database to find three dividend stocks with yields starting at 7%, high by any standard, and with potential upsides starting at 13%. These are stocks that will both grow the portfolio and provide a steady income – and success on multiple fronts is a key strategy to surviving a difficult market environment.

Enbridge, Inc. (ENB)

We’ll start in the energy industry. Enbridge the largest natural gas distributor in Canada, and the owner/operator of North America’s longest network of crude oil transport pipelines. With a $62.6 billion market cap, Enbridge had both the deep pockets and the essential niche to weather the coronavirus crisis.

The company saw earnings rise sequentially during Q1, the ‘corona quarter.’ EPS, at 62 cents per share, was up 34% from Q4, and beat estimates by 21%. Quarterly revenues were down year-over-year, at $8.96 billion, but beat the estimates by 5%. Looking ahead, Enbridge is expected to gross more than $32 billion on the top line this year.

Enbridge also improved liquidity during the coronavirus crisis, adding a new $3 billion credit facility an issuing notes worth $4 billion. The company reports it now has access to $14 billion in cash and credit. The strong liquidity has allowed the company to maintain its dividend, which it declared on May 5 at 81 cents per common share. ENB dividend yield is 7.4%, a strong return when compared to the average dividend, just about 2%, found among S&P-listed companies.

Evercore ISI analyst Durgesh Chopra is bullish on the stock, noting “Perhaps not previously fully appreciated by the majority of US based equity investors, ENB offers surprisingly little sensitivity to volume fluctuation and overall supply dynamics of Western Canadian heavy and light production… ENB is set to emerge post COVID in a much better position. It has streamlined ownership as well as its portfolio and paid down debt. We expect ENB to trade at a premium…”

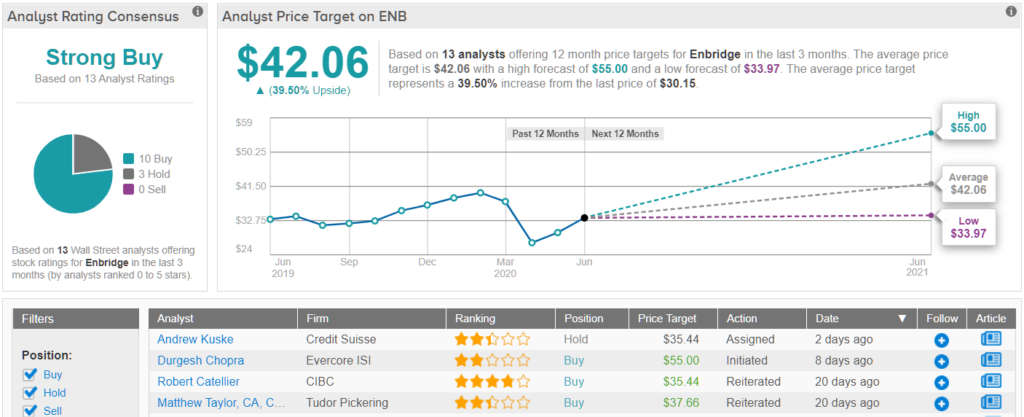

The analyst gives ENB shares a Buy rating, with a $55 price target indicating a robust 82% upside potential for the coming year. (To watch Chopra’s track record, click here)

Wall Street agrees that ENB is a buying proposition. The stock has a Strong Buy analyst consensus, based on 10 Buy and only 3 Holds. Enbridge shares are selling for $30.16, and the $42.06 average price target suggests it has room for 39.5% growth this year. (See Enbridge stock analysis on TipRanks)

Fortress Transportation and Infrastructure (FTAI)

The next company on today’s list, Fortress Transportation and Infrastructure, is an interesting investment. The company is structured as a REIT, but instead of investing in real estate, Fortress invests mainly in transportation assets. More than half of the company’s portfolio is composed of aviation equipment – meaning Fortress leases high-end commercial aircraft to operators. The company also has an oil refinery and terminal facility on the Texas Gulf coast, in addition to a number of smaller assets.

Fortress boasts a high level of lease activity, with 69 of 76 aircraft and 108 out of 168 aircraft engines currently on lease agreements. The average remaining lease term for planes is 33 months and for engines is 14 months, giving Fortress a high level of stability due to recurring revenue.

Steady recurring revenue allows Fortress to keep a reliable dividend. The company has paid out 33 cents per share quarterly without missing a beat since 2015. The annualized payment, at $1.32, makes the yield 11.1%. The high yield and solid reliability combine to make this an attractive equity for income investors.

5-star analyst Devin Ryan of JMP Securities is sanguine about Fortress’ future, writing of the company: “[We] appreciate the firm will need to navigate some pretty meaningful headwinds in the near term (specifically within Aviation), we do believe it is better positioned than most to ride out the storm, from a capital and business model perspective, following substantial de-levering and improved liquidity in late 2019/early 2020. Importantly, in conjunction with earnings, the company declared its regular quarterly dividend of $0.33, and management was clear that it fully expects to continue to pay this dividend unless the operating backdrop deteriorates significantly further from its current view.”

Ryan gives the shares a Buy rating, and his $20 price target implies room for a hefty 77% one-year upside. (To watch Ryan’s track record, click here)

The Strong Buy consensus rating on FTAI is unanimous – Wall Street’s analysts have given the stock 6 Buy ratings. The average price target is $15.83, which indicates room for 40% upside growth from the current share price of $11.31. (See Fortress stock analysis on TipRanks)

Two Harbors Investment Corporation (TWO)

Two Harbors, the last stock on our list, is a more tradition real estate investment trust. The company invests in real property, but its focus is on residential mortgage-backed securities. Management described the coronavirus crisis as ‘unprecedented,’ and used liquidity measures to shore up the company portfolio during Q1. As a result, TWO reported 25 cents per share earnings in the first quarter of 2020, steady from the previous quarter.

Steady earnings allowed the company to pay out 14 cents per common stock share in the quarterly dividend. This annualizes to 56 cents, and gives a yield of 10.4%. TWO has a history of adjusting its common stock dividend to maintain it at affordable levels; the result is a payout that may sometimes change from quarter to quarter, but which the company is committed to paying out to shareholders.

Trevor Cranston, 4-star analyst with JMP, was impressed by Two Harbors’ ability to manage the COVID-19 hit. He wrote, “Despite difficult market conditions, TWO was able to meet all margin calls during the first quarter, and sold substantially all of its non-agency credit assets in order to limit further risk going forward.” Of the company’s forward prospects, Cranston is optimistic: “However, we believe returns on new investments are attractive in the agency MBS paired with MSR strategy, which should result in improved earnings once peak advancing requirements are past.”

A $6 price target suggests a 16.5% upside to the stock, in Cranston’s view, and he accordingly rates the stock a Buy. (To watch Cranston’s track record, click here)

Two Harbors is currently selling for $5.15 and the average price target is in line with Cranston’s, at $6.07. This implies a 16% upside for the stock in the coming year. The analyst consensus here is another Strong Buy, based on 6 Buys and 2 Holds set in recent weeks. (See Two Harbors stock analysis on TipRanks)

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.