The worst monthly jobs report in the series’ 72-year history wasn’t able to derail the market’s recent rally. Labor Department data showed that the US lost 20.5 million jobs in April, sending the unemployment rate up to 14.7%.

But there may be some glints of hope. First, the unemployment number came in slightly lower than the 22 million predicted, in a sign that maybe – just maybe – the third quarter will be less bad.

There is one more point, sometimes overlooked, that may bear out the upbeat view. Unlike previous recessionary events, in which job losses were permanent, the Labor Department data this time shows that nearly 18 million of the unemployed are reported as ‘temporarily out of work;’ that is, they can expect to find their jobs waiting for them once the economy reopens. Yes, the recovery will take longer than the initial fall – but there is a chance that it will come on faster and stronger than the naysayers believe.

The market’s resilience in the face of high unemployment and the ongoing pandemic issues raises a question, of course: which stocks are best to buy into? The analysts at investment firm Needham have pinpointed three companies in the networking and cloud software fields that are primed for gains.

Using TipRanks’ Stock Comparison tool, we lined up the three alongside each other to get the lowdown on what the near-term holds for these top Needham picks.

Ceragon Networks, Ltd. (CRNT)

First on the list is Ceragon, a manufacturer of wireless networking hardware. Ceragon is heavily invested in both urban wireless infrastructure and the coming 5G rollout, making it uniquely well positioned to benefit from the lockdown orders. As people are required to remain at home, and hundreds of thousands of workers switched to remote work situations, demand for wireless services has increased.

Despite running net losses for the past two quarters, Ceragon shares have dramatically outperformed the broader markets. Since the bear cycle began on February 19, Ceragon has actually gained 12%, making a sharp contrast with the 13% net loss on the S&P 500 index.

Covering this stock for Needham, 5-star analyst Alex Henderson writes: “We expect Ceragon to weather the current economic challenges as it sells to Service Providers. The company noted a strengthening of demand due to sharp increases in network traffic. We expect demand to outstrip Revenue, driving a positive Book-to-Bill across CY20… Longer term, we see Ceragon as a clear 5G beneficiary. As we move into CY21, demand for higher speeds and greater software flexibility play to Ceragon’s key product advantages.”

In line with his long-term optimism, Henderson upgraded his stance on Ceragon from Neutral to Buy. His $3.25 price target implies an impressive upside potential of 46%. (To watch Henderson’s track record, click here)

Looking at the consensus breakdown, only one other analyst has thrown an opinion into the mix. The rating is a Hold, making the Street consensus a Moderate Buy. (See Ceragon stock analysis on TipRanks)

CommVault Systems (CVLT)

Next up is a software company, in the cybersecurity niche. CommVault offers products for data management and protection, as well as backup and recovery, retention and compliance, and cloud management. The value of Commvault’s product in today’s digital world is clear: in fiscal 2019, the company brought in $711 million in total revenues.

CommVault will report earnings for the current quarter (fiscal Q4) on May 12, and is expected to show EPS of 9 cents, up 28% year-over-year despite the recessionary pressures of recent months. In its last quarter, fiscal Q3 reported in January, CVLT beat the forecasts on both earnings (showing 18 cents per share) and revenues (showing $176.4 million).

Jack Andrews, another 5-star analyst with Needham, was impressed enough with CVLT to initiate coverage of the stock with a Buy rating and a $55 price target, suggesting a 22% growth potential for the coming year. (To watch Andrews’ track record, click here)

Andrews lays out a clear case for near-term value here: “We believe revenue growth could benefit from a renewal cycle which should begin to occur in FY21. In essence, CVLT has transitioned its perpetual software business to a recurring model and these contracts are expected to come up for renewal… we believe this should provide a tailwind to growth.”

CommVault has attracted more attention from Wall Street than Ceragon above, and that attention is mainly positive. Of 5 recent reviews, 4 are Buys and one is a Hold, giving the stock an analyst consensus rating of Strong Buy. Shares are selling for $45, and the $50 average price target implies room for an 11% upside potential. (See CommVault stock analysis on TipRanks)

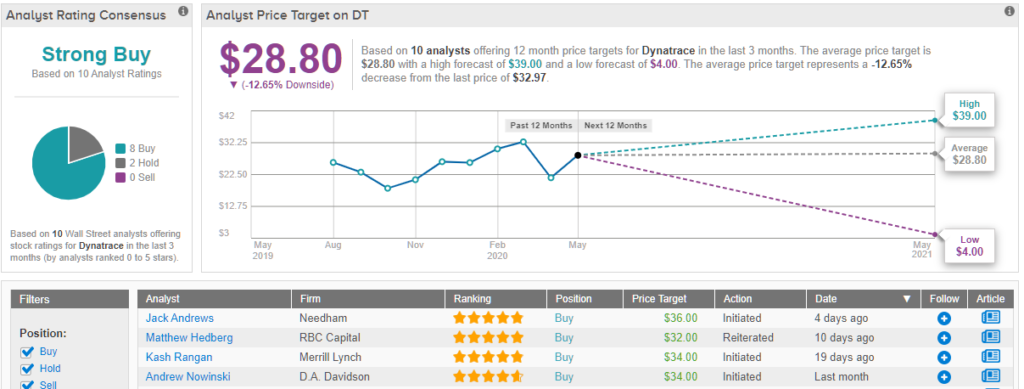

Dynatrace, Inc. (DT)

Last up is Dynatrace, another software company. Dynatrace focuses on AI software designed to monitor and manage cloud infrastructure, important functions for cloud and networking companies. DT’s products help minimize networking strains by tagging potential problems before they disrupt systems.

Dynatrace went public just one year ago, and turned profitable in Q4 2019, when it showed 6 cents EPS. The estimate for the coming earnings report is for a 3-cent per share profit. The fact that DT is turning profits so soon after its IPO, and even in the current COVID-19 environment, is testament to the strength and necessity of the company’s niche.

This is another company that impressed Needham’s Andrews enough to initiate coverage as a Buy. He wrote of Dynatrace, “We believe Dynatrace has room to grow its already leading position within enterprise customers, which are only ~10% penetrated. Additionally, we believe the expansion opportunity is still nascent as ~80% of DT’s expansion business is derived from the growth of APM to additional hosts… new catalysts that should drive improved monetization, and an attractive valuation on both an absolute and relative basis.”

Andrews backed his Buy rating with a $36 price target, indicating his confidence in a 10% upside potential for the stock.

DT shares have recently powered right through their average price target, another indicator of investor confidence. The stock sells for $32.99, about 13% above the average price target of $28.80. Expect Wall Street’s investors to revisit their expectations here in the near future. In the meantime, 8 of 10 reviews on this stock are to Buy, giving DT a Strong Buy analyst consensus rating. (See Dynatrace stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.