Disconnected. This seems to be the best way to describe the current economic environment. Amid high levels of unemployment and tanking earnings, stocks aren’t just hanging in there, they’re charging forward. As a result, traditional metrics might not be enough to display the big picture. In this case, other tools are needed.

TipRanks offers one such tool that can make finding compelling plays feel less like a fool’s errand. The Smart Score feature utilizes the comprehensive market data collected by the platform, collating it according to 8 key metrics often used to gauge the trajectory of a given name. After all of this information is aggregated, each stock is assigned a single-digit score, from 1 to 10, that can indicate the direction it is heading in.

Bearing this in mind, we used TipRanks’ database to pinpoint three healthcare stocks that have received the highest possible Smart Score, a “perfect 10”. Speaking to the strength of these names, each scores a “Strong Buy” consensus rating from the Street and boasts substantial upside potential.

United Therapeutics Corporation (UTHR)

With multiple therapies approved for the treatment of pulmonary arterial hypertension (PAH) and pediatric neuroblastoma, United Therapeutics is already profitable. That said, this name is under Wall Street’s microscope thanks to its ongoing clinical activity.

UTHR recently presented positive results from the Phase 3 INCREASE trial evaluating Tyvaso in pulmonary hypertension associated with interstitial lung disease (PH-ILD) at the Breaking News Session hosted by the American Thoracic Society (ATS). The data, which was in line with data released back in February, showed that the drug significantly improved exercise capacity.

Writing for Wedbush, four-star analyst Liana Moussatos notes that during the event, Dr. Steven D. Nathan, M.D., Director of the Advanced Lung Disease Program and Director of the Lung Transplant Program at Inova Fairfax Hospital, weighed in on the results. According to Dr. Nathan, the fact that the INCREASE study hit the secondary endpoint of reduction in risk of clinical worsening events is “a key differentiator for Tyvaso as well as a clinically meaningful outcome.”

Moussatos added, “Dr. Nathan was not too concerned about no changes observed in patient-reported outcome measures/quality of life due to the short study duration (16 weeks). Dr. Nathan was impressed with the improvement in forced vital capacity (FVC; a marker of disease progression) observed with Tyvaso treatment.”

Speaking to the opportunity for this indication, there’s a substantial unmet medical need among the 30,000 PH-ILD patients in the U.S. Moussatos also highlights that other ILD clinical trials excluded severe ILD patients.

“We came away from the presentation confident about Tyvaso prospects in PH-ILD. The Company recently submitted the sNDA to revise the Tyvaso label to reflect the positive results from the INCREASE study and we anticipate FDA acceptance of the filing for review in Q3:20,” Moussatos concluded.

Unsurprisingly, Moussatos continues to give UTHR her stamp of approval. Along with an Outperform rating, she keeps the price target at $243. Should the target be met, a twelve-month gain of 103% could be in store. (To watch Moussatos’ track record, click here)

Do other analysts agree with Moussatos? As it turns out, most do. 6 Buy ratings and a single Hold add up to a Strong Buy analyst consensus. At $155.14, the average price target indicates 29% upside potential. (See United Therapeutics stock analysis on TipRanks)

Axsome Therapeutics (AXSM)

Focusing primarily on central nervous system (CNS) disorders, Axsome Therapeutics wants to provide patients battling these conditions with better treatment options. After getting good news from the FDA, it’s no wonder this company is scoring major analyst attention.

At the end of June, AXSM revealed that the FDA had granted its Alzheimer’s disease (AD) agitation treatment, AXS-05, Breakthrough Therapy Designation (BTD). It should be noted that this isn’t the first BTD the therapy has received, with the designation also given to the candidate for the major depressive disorder (MDD) indication.

With no approved therapies currently available to treat AD agitation, H.C. Wainwright’s Raghuram Selvaraju sees a large opportunity, noting that the BTD could help AXSM bring the product to market much more quickly.

The 5-star analyst explained, “BTD provides an organizational commitment involving senior managers from the FDA, more intensive FDA guidance on an efficient development program, and greater access to and more frequent communication with the agency throughout the entire drug development and review process. It also provides the opportunity to submit sections of a New Drug Application (NDA) on a rolling basis. In addition, BTD-reviewed products are eligible for Priority Review, which implies action on an application within six months vs. ten months under standard review.”

The candidate got the designation as a result of robust data from the pivotal Phase 2/3 ADVANCE-1 study. “In this trial, treatment with AXS-05 resulted in a rapid, substantial, and statistically significant improvement in agitation as compared to placebo. On the primary endpoint, AXS-05 demonstrated a statistically significant mean reduction from baseline in the Cohen Mansfield Agitation Inventory (CMAI) total score vs. placebo at Week 5,” Selvaraju stated. He also points out that AXS-05 was well-tolerated and achieved a better CMAI total score than bupropion.

The news just keeps getting better. Axsome should be able to complete regulatory filings for AXS-05 in MDD and AXS-07 in migraine within the next six months, in Selvaraju’s opinion. “In addition, we believe that 2021 could prove even more impactful than 2020 for Axsome, since the company might not only secure approvals for AXS-05 (in MDD) and AXS-07 but also generate confirmatory pivotal clinical data with AXS-05 in treatment-resistant depression (TRD) and possibly AD-associated agitation along with Phase 3 data for AXS-12 in narcolepsy,” he commented.

Everything that AXSM has going for it prompted Selvaraju to stay with the bulls. To this end, he reiterated his Buy recommendation and $210 price target. This target implies shares could climb 159% higher in the next year. (To watch Selvaraju’s track record, click here)

Looking at the consensus breakdown, other analysts are on the same page. Only Buy ratings, 6, in fact, have been issued in the last three months, so the consensus rating is a Strong Buy. With a $142.80 average price target, the upside potential lands at 76%. (See Axsome Therapeutics stock analysis on TipRanks)

ChemoCentryx Inc. (CCXI)

Like the name implies, ChemoCentryx’s drug candidates focus on a specific chemokine or chemoattractant receptor that blocks the negative inflammatory or suppressive response induced by that particular receptor, while leaving the rest of the immune system unharmed. Following a recent call with key opinion leaders (KOLs), one Wall Street pro believes that now is the right time to snap up shares.

5-star analyst Michelle Gilson, of Canaccord Genuity, recently discussed the company’s positive Phase 3 ADVOCATE trial results for its avacopan product with two KOLs. Even though access to the therapy remains a concern for physicians, both KOLs stated that they plan to use avacopan in their clinical practice and in all or almost all ANCA-associated vasculitis (AAV) patients, if they have broad access.

Physicians have been trying to limit steroid exposure when treating AAV. Therefore, Gilson believes “having a drug to replace the steroids should aid in physician comfort to reducing steroid exposure.” She added, “One physician seemed somewhat shocked that avacopan performed so well on some subsets, such as in combination with RTX and in relapsing patients, though the other cautioned that it looks good in all patients and shouldn’t be limited to certain subsets. Additionally, one of these KOLs mentioned that kidney improvement was a cherry on top, especially as GFR continued to improve from weeks 26-52.”

However, when it comes to the kidney results, they did stir up some controversy based on the slight baseline imbalance in eGFR. Having said that, Gilson thinks “a publication should help characterize kidney results/effect of avacopan, as other nephrologists have expressed to us the speed and magnitude of the kidney improvements were exciting.”

To sum it all up, Gilson said, “We continue to view the positive data from ADVOCATE presentations as paving a path toward broad incorporation of avacopan into standard of care AAV treatment. These two KOL calls indicated strong demand for avacopan.”

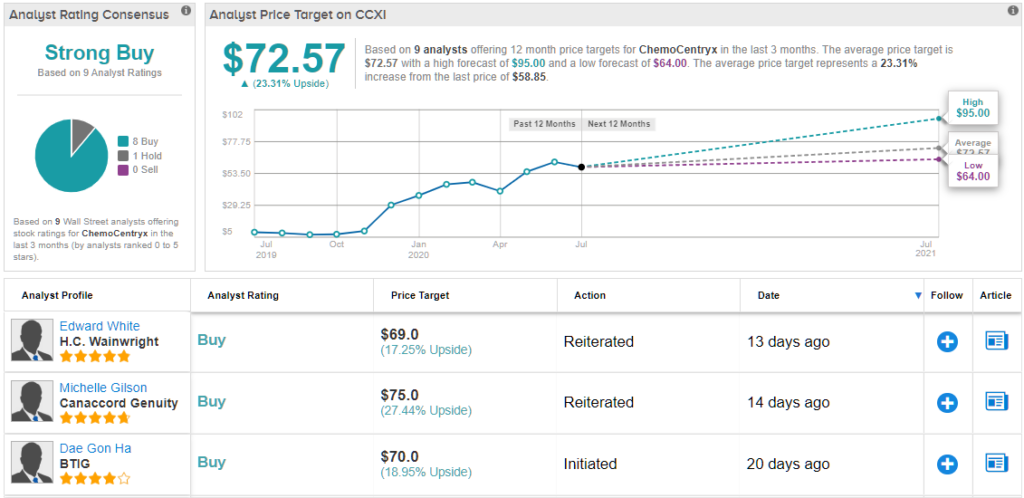

Sealing the deal for Gilson, according to one of the KOLs, the results suggest avacopan could potentially be used in other indications like C3 glomerulopathy, IgA nephropathy and lupus nephritis. As a result, she maintained both her bullish call and $75 price target, implying 30% upside potential. (To watch Gilson’s track record, click here)

Turning now to the rest of the Street, other analysts also like what they’re seeing. CCXI’s Strong Buy consensus rating breaks down into 8 Buys versus a lone Hold. Based on the $72.57 average price target, shares could surge 25% in the next year. (See ChemoCentryx stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.