The average retail investor, looking for a route toward profits in today’s confusing market environment, can usually choose one of two basic strategies. The first is the traditional stock market path, that of share appreciation, while the second is the safer, more defensive, route through dividend payers. But what if an investor doesn’t need to choose between these routes?

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

A number of dividend champs are offering potential investors a double whammy right now: to go along with high dividend yields, they also boast high upside potential. This is a possible win-win for defensive investors, as high dividends and high share price gains typically do no walk together. When they do, it presents a powerful opportunity for investors seeking to pad their portfolio gains against economic headwinds.

Using the TipRanks platform, we’ve pulled up the details on three stocks that are showing exactly this combination: dividend yields of 5% or better, strong upside potential of over 90%, and recent approval from some of Wall Street’s analysts. Let’s take a closer look.

Riley Exploration Permian (REPX)

We’ll start with Riley Exploration Permian, one of the many independent hydrocarbon exploration and development companies operating in the Permian Basin of West Texas and New Mexico. This geological formation has made headlines over the past decade, as it has powered Texas’ resurgence into the forefront of the global energy sector. Riley bills itself as a growth-oriented oil and natural gas company, engaged in acquisition, exploration, development, and production activities in the oil, natural gas, and natural gas liquids reserves on its land assets in the Permian.

One of the smaller players in its niche, with a market cap of $458 million, Riley saw total production in its recently reported Q2 of fiscal year 2022 (the quarter ending this past March 31) of 7.5 MBbls per day. This represented a 24% increase year-over-year, and came in at the high end of guidance.

The company generated an adjusted EBITDAX of $34.4 million, on income from operations of $41 million. Operating cash flow in the quarter came to $30 million, of which $20.3 million was listed as free cash flow. Riley was able to fund dividend payments totaling $6 million in the quarter, with the most recent payment going out after the quarter ended, on May 5. The company’s current common share dividend payment is set at 31 cents; at this rate, the dividend annualizes to $1.24 and gives a yield of 5.3%.

Among the bulls is Truist 5-star analyst Neal Dingmann who writes: “Riley continues to offer unique opportunities for investors as we believe the shares trade at a notable discount versus its peers despite having one of the highest production growth rates, while simultaneously offering over a 5% dividend yield… we forecast cash flow and earnings to continue ramping as volumes and prices likely remain strong.”

In line with this bullish stance, Dingmann sets a $52 price target on REPX shares, suggesting a one-year gain of 124% in the offing. Unsurprisingly, Dingmann rates the stock as a Buy. (To watch Dingmann’s track record, click here)

Riley has slipped under most analysts’ radar; the stock’s Moderate Buy consensus is based on just two recent ratings. With shares trading at $23.17, the $47 average price target suggests room for 103% upside. (See REPX stock forecast on TipRanks)

Deluxe Corporation (DLX)

We’ll switch over to the business technology sector where Deluxe offers a suite of packages that facilitate billing and payments, growth and operations for its enterprise customers. The company’s products include solutions for business management, payroll & HR, business forms, digital marketing, online reputation management, business checks, echecks, and digital payments – and that list is far from complete. Deluxe has been in operation for over a century, streamlining its clients’ operations, and today boasts over 4,000 financial institutional clients, and more than 4 million active small business customers.

Deluxe has been experiencing generally rising revenues since emerging from the pandemic crisis in early 2020. Deluxe reported $556 million at the top line in 1Q22, up 26% from the $441.3 million reported in the year-ago quarter.

While revenues reflected an increase in business, earnings and cash flow reflected an environment that is growing more difficult. Adjusted EPS fell 16% y/y to $1.05, and free cash flow dropped $4.4 million, to $13.5 million. Per management, the drop in free cash flow was due at least in part to increased cash interest payments.

Of particular interest to dividend investors, Deluxe has maintained a steady payment of 30 cents per common share, every quarter, going back to 2017. This dividend, annualized to $1.20, gives a yield of 5.6%.

Analyst Lance Vitanza, writing from Cowen, notes that Deluxe’s results have slipped in some ways, but points out that the current inflationary environment, and associated headwinds, had already baked that in.

Expecting better results long term, when headwinds fade, Vitanza writes: “Though seasonal patterns suggest sequential improvement over the balance of the year, margins will continue to reflect the ongoing inflationary cost environment, we expect. Accordingly, while our estimated Adj. EBITDA margin improves sequentially throughout the rest of the year, results will likely fail to reflect the full potential of intrinsic earnings power, in our opinion. We believe Deluxe can and will demonstrate a more-favorable margin structure in a more-normalized cost environment.”

In Vitanza’s view, Deluxe has plenty of potential. The analyst rates the stock an Outperform (i.e. Buy), while also setting a $42 price target that indicates confidence in a 102% upside ahead. (To watch Vitanza’s track record, click here)

Some stocks fly under the radar, and DLX is one of those. Vitanza’s is the only recent analyst review of this company, and it is decidedly positive. (See DLX stock forecast on TipRanks)

Rent-A-Center (RCII)

Rent-A-Center, or RAC, is a rent-to-own company, a leader in the industry, and offers down-scale – or even just very frugal – customers access to a wide range of consumer products such as electronics, appliances, furniture, and computers through flexible leases-purchase agreements. Customers get the benefit of the product, an option to buy at the end of the lease, and the avoidance of long-term, high-interest debt obligations. RAC operates through more than 1,900 brick-and-mortar retail locations.

But brick-and-mortar is old school – and RAC has moved to modernize its business model through the acquisition last year of Acima. Acima is a tech-based leasing company, in a similar niche to RAC – but operating mainly online or through its mobile app, supplemented by retail locations. The acquisition, which cost RAC approximately $1.6 billion, pools the company’s networks, but more importantly, gives RAC access to the app-based sales pathway.

In terms of raw numbers, RAC continues to produce. The company saw $1.2 billion at the top line in 1Q22, up from $1.04 billion in the year-ago quarter. On earnings, the company showed a decline, with non-GAAP diluted EPS falling by almost half – from $1.32 to 74 cents.

On cash, however, RAC generated $205.3 million from operations, of which total some $188.9 million was free cash flow. This supported the generous dividend policy, under which the company returned a total of $21.1 million to shareholders. The common share dividend is currently set at 34 cents; the last payment was made in late June. The dividend has been increased three times in the last three years, and at its current rate annualizes to $1.36 per common share. This gives a yield of 6.6%, more than triple the average found among S&P-listed firms.

Covering the stock for Raymond James, 5-star analyst Bobby Griffin acknowledges the headwinds but sees a path forward for this lease-to-own company: “As with any portfolio style business, improvements will take time, but Rent-A-Center is showing progress and the business is not ‘broken’ (still profitable, generating a sizable FCF, and is an important source of products for a subprime customer). Accordingly, with the stock down [56%] YTD, we see a lot of the downside risk already priced in, and a favorable risk/reward, especially considering potential tighter credit conditions through 2022/2023.”

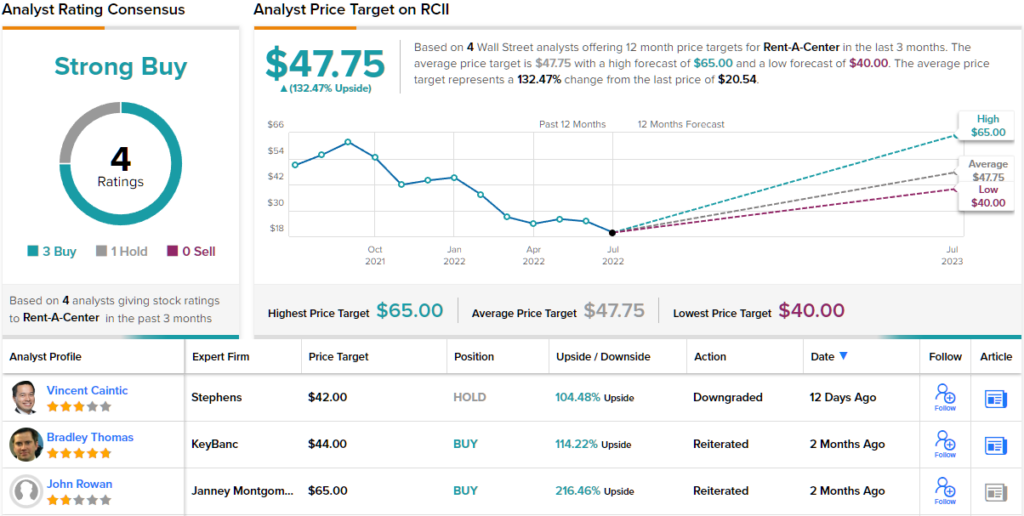

To this end, Griffin rates RCII an Outperform (i.e. Buy), and his price target, which he puts at $40, implies a one-year upside potential of 95%. (To watch Griffin’s track record, click here)

All in all, this stock has picked up 4 recent analyst reviews, which include 3 to Buy and 1 to Hold, for a Strong Buy consensus rating. Shares in Rent-A-Center are trading for $20.54 and their average price target of $47.75 suggests we’ll see a robust gain of ~132% in the next year. (See RCII stock forecast on TipRanks)

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.