Which stocks are leading the pack out on Wall Street? Biotechs. Understandably, investors have taken a more cautious approach when navigating the confused financial environment, but focus is locking in on the healthcare sector as it has been able to withstand the COVID-19-induced pressure on the market.

Don't Miss our Black Friday Offers:

- Unlock your investing potential with TipRanks Premium - Now At 40% OFF!

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

The space’s resilience combined with a limited impact on Q1 fundamentals and the elimination of macro headwinds regarding drug legislation, has caused sentiment surrounding 2H20 performance to swing strongly positive.

While there certainly are exciting opportunities at play, biotech stocks aren’t for the faint of heart. Seasoned market watchers know that they are notoriously volatile, prone to huge movements on account of a single update. This makes them riskier investments, but it also enables them to deliver massive returns.

As a result, it can be hard to gauge which biotech names are primed for explosive growth. Not to worry, there are strategies that can help make this process a little easier like taking a cue from the analysts.

With this in mind, we turned to investment firm Wedbush to get some investing inspiration. Using TipRanks database, we got a closer look at three of the firm’s Buy-rated picks, which happen to trade for less than $10 per share. The cherry on top? The firm’s analysts believe that each of the tickers could see their share prices take flight over the next months.

Five Prime Therapeutics (FPRX)

Developing protein therapeutics designed to address the needs of patients, Five Prime Therapeutics hopes to be able to provide innovative new treatment options. Ahead of potential near-term inflection points, shares are changing hands for $4.65 apiece, reflecting an attractive entry point, according to Wedbush.

Pointing to the upcoming clinical data readouts for FPT155 and bemarituzumab, firm analyst Robert Driscoll believes these events are “important value drivers for the company.” Phase 1 monotherapy data for FPT155 in advanced solid tumors, which will include a first look at efficacy, could come by YE:20. As for bemarituzumab, data from the Phase 2 FIGHT study evaluating the therapy in combination with mFOLFOX6 in frontline Gastric/ GEJ cancer is slated to readout by YE:20 or early 2021. Management is expecting the FIGHT study to yield enough PFS and OS events to meet this timeline.

“Given these upcoming readouts, we see a favorable risk/reward profile for shares, particularly given management’s recent substantial strategic clinical development adjustments and corporate restructuring,” Driscoll commented.

Looking more closely at FPT155, the Wedbush analyst noted, “We see a lot of value in FPT155’s dual mechanism of action which includes CTLA-4 antagonism and CD28 agonism. We are excited about this mechanism for two reasons – first, CTLA-4 is a clinically validated target that has demonstrated monotherapy and clear combination activity with anti-PD-(L)1s, and second, it has been shown preclinically that CD28 co-stimulation contributes critically to the efficacy of anti-PD1 therapy.”

To this end, Driscoll rates FPRX an Outperform (i.e. Buy) along with a $9 price target. Should his thesis play out, a potential upside of 94% could be in the cards. (To watch Driscoll’s track record, click here)

FPRX has kept a relatively low profile, as only one other analyst has thrown an opinion into the mix in the past 3 months. The additional Buy rating means that the stock has a Moderate Buy consensus rating. At $9, the average price target is identical to Driscoll’s. (See FPRX stock analysis on TipRanks)

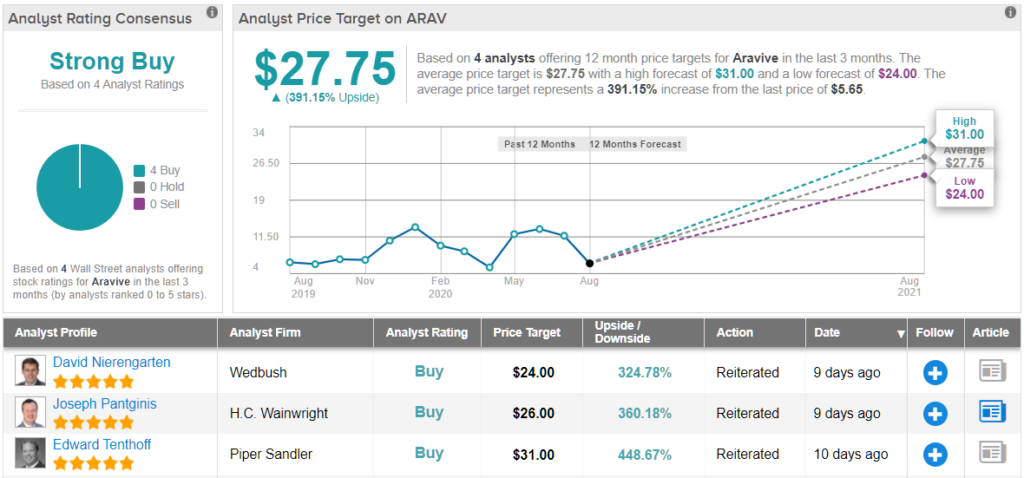

Aravive Inc. (ARAV)

Focusing on the targeting signaling pathways that drive the activation, migration and invasion of abnormal cells into healthy tissues, Aravive develops treatments designed to stop life-threatening diseases like cancer and fibrosis in their tracks. Based on its recent clinical results and $5.83 share price, the stock looks “undervalued” to Wedbush.

Writing for the firm, 5-star analyst David Nierengarten tells clients that the recent results for AVB-500 in ovarian cancer are encouraging. In the Phase 1b/2 study, the candidate in combination with paclitaxel (PAC) produced overall response rates of 35%, with 3 out of 5 responses in patients dosed in the 15 mg/kg cohort. Additionally, progression free survival (PFS) in patients dosed with the AVB-500 plus paclitaxel combination was 7.4 months.

It should be noted that prior Avastin (bevacizumab) treatment in AVB-500 and PAC patients could lead to worse outcomes (6/10 ORR without prior bevacizumab vs. 2/13 ORR with prior bevacizumab). “Given these Avastin outcomes, it would be interesting to determine if AVB-500 has additional activity in combination, before the patients are Avastin-experienced. We expect the company to explore these and other combinations to move AVB-500 into earlier lines of therapy,” Nierengarten commented.

Given other positive trends demonstrating improvements at higher doses and in patients with high sAXL/GAS6 ratios, Nierengarten argues “there is additional evidence that AVB-500 combination therapy could be efficacious in ovarian cancer patients.” He also points out that ARAV wants to design an adaptive study using biomarkers to support eventual approval.

With the significant unmet need in the space, Nierengarten believes it’s very likely that the trial will ultimately come to fruition. He added, “With an adaptive design, we could see an interim look at the pivotal study data in 2021.” If that wasn’t enough, Nierengarten highlights the fact that “ARAV is planning to begin its Phase 1b/2 study in clear cell renal carcinoma (ccRCC) in 2H20 and potentially look at combinations in earlier lines of ovarian cancer in 2021.”

All of this prompted Nierengarten to state, “At just under $4 per share in cash, and ~$35 million enterprise value, with a soon-to-be registration-enabling study in ovarian cancer patients, we view the risk/reward as favorable.”

In line with his optimistic take, Nierengarten rates ARAV an Outperform (i.e. Buy), along with a $24 price target. This figure implies upside potential of a massive 320%. (To watch Nierengarten’s track record, click here)

Overall, based on all the above factors, Wall Street analysts are thoroughly impressed with ARAV. It boasts 100% Street support, or 4 Buy ratings in the last three months, making the consensus a Strong Buy. If this wasn’t enough, the $27.75 average price target implies that shares could surge 391% in the next twelve months.(See Aravive stock analysts on TipRanks)

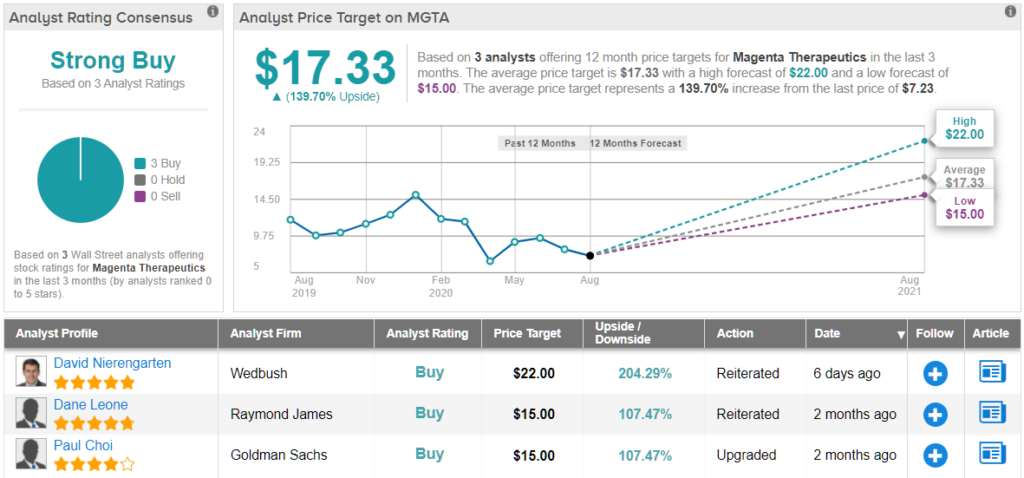

Magenta Therapeutics Inc. (MGTA)

Through its research efforts, Magenta Therapeutics wants to create a world in which patients’ immune systems can be reset via stem cell transplant to cure autoimmune diseases, blood cancers and genetic diseases. With more clarity on its clinical programs set to come in the second half of the year, its $7.28 share price presents investors with an opportunity to get in on the action, if you ask Wedbush.

Analyst David Nierengarten, who also covers ARAV, is looking forward to data from the first subjects in MGTA-145’s Phase 2 stem cell mobilization studies in H2:20, with the results expected to be readout shortly after enrollment wraps up. On top of this, the company has partnered with the National Marrow Donor Program (NMDP)/Be The Match organization to conduct a Phase 2 study to advance the therapy’s development.

Reflecting another positive, Nierengarten commented, “MGTA is currently advancing their anti-CD-117 amanitin-based ADC for non-genotoxic, selective stem cell ablation in IND-enabling studies and expects to enter the clinic soon and have data next year. We look forward to early data, which should also be rapidly obtained once the company enters the clinic.”

It should also be noted that the company is working with AVROBIO and Beam Therapeutics, with MGTA potentially applying its technology to their gene therapy and gene editing programs. Nierengarten added, “The company is also advancing their CD45-ADC lead candidate through IND-enabling studies program for eventual use immune reset via killing disease-causing aberrant T-cells.”

To sum it all up, the Wedbush analyst stated, “Overall, 2021 should have several data releases from clinical studies that will be predictive of future success, given the nature of MGTA’s programs.”

Everything that MGTA has going for it convinced Nierengarten to stay with the bulls. As a result, he rates MGTA an Outperform (i.e. Buy) rating, along with a $22 price target. This target conveys his confidence in MGTA’s ability to climb 202% higher in the next twelve months.

Other analysts don’t beg to differ. Out of 3 total reviews published in the last three months, all 3 analysts rated the stock a Buy. Therefore, MGTA is a Strong Buy. The $17.33 average price target implies shares could appreciate by 138% in the coming year. (See Magenta stock analysis on TipRanks)

To find good ideas for healthcare stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.