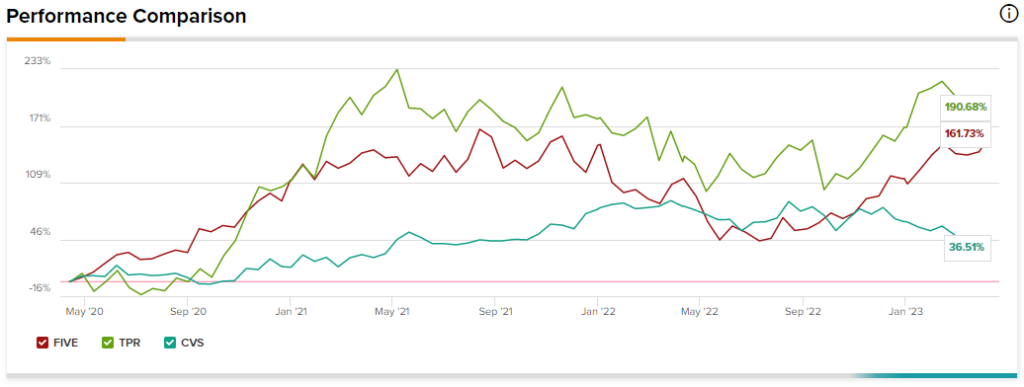

As recession storm clouds get closer, it’s only prudent to play stocks cautiously. Though a 2023 recession has been on our radars for some time, the top-tier consumer-facing stocks are still modestly priced, according to analysts. Therefore, in this piece, we’ll tune into TipRanks’ Comparison Tool to gauge the value to be had in these three highly-rated consumer stocks — FIVE, TPR, and CVS.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

Five Below (NASDAQ:FIVE)

FiveBelow is a discount retailer that’s really thrived with younger consumers. After last year’s wave of high inflation, FiveBelow now sells some goods above $5, with more premium products going for as much as $25. Indeed, it’s about time to change the company’s name to FiveAbove! Despite price hikes, FiveBelow remains a terrific place to shop for those seeking price certainty. Nonetheless, as we wander into a recession, I’m neutral about the stock’s prospects, mainly due to its valuation.

The retailer saw shares suffer a 50% haircut from peak to trough. After some remarkable quarters, though, FiveBelow has recouped almost all of the ground lost. As the name looks to break new highs in the face of a recession, there are reasons for investors to stick with the name even though the discount on shares is less appealing than it was just a few months ago.

For instance, FiveBelow knows its target consumer really well, and the inclusion of pricier items hasn’t hurt the firm’s reputation as a place to save money on various specialty goods. If anything, pricier items have drawn bigger crowds looking for a better balance between affordability and quality.

Despite recent share momentum, FiveBelow sports a relatively modest outlook for 2023. Management expects sales in the $3.49 billion to $3.59 billion range (other analysts expected $3.66 billion) as the firm wanders into a recessionary environment. Indeed, it’s far better to err on the side of caution when setting up targets in the face of the unknown.

Given its recession-resilient traits, the low bar makes FiveBelow more enticing. It’s a value retailer, after all, and these days, the appetite for good value seems to be getting higher by the day.

However, although I like the company and its ability to weather the storm, I’m no fan of its valuation. At 46.2 times trailing price-to-earnings (P/E), FIVE stock is far pricier than the department store industry average of 27.3 times.

Sure, FiveBelow is the hot new retailer on the block, and it can do well in bad times. Still, I’m uncomfortable paying such a premium over the peer group. Though FiveBelow set a low bar for itself this year, I think the valuation implies a high bar set by the market.

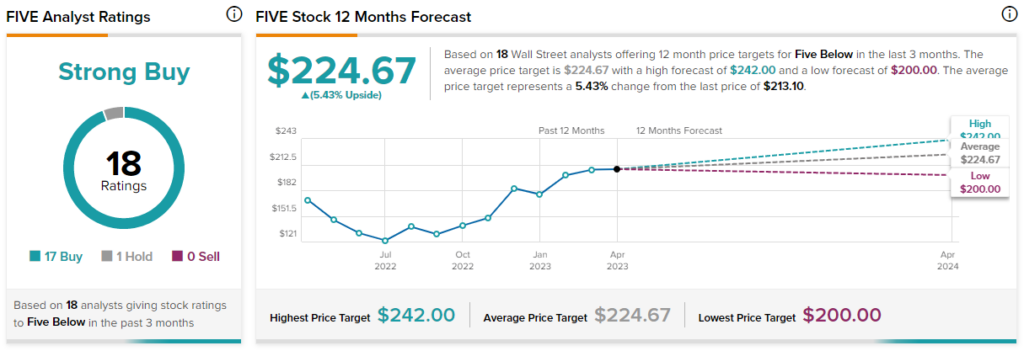

What is the Price Target for FIVE Stock?

FiveBelow commands a Strong Buy, with 17 Buys and one Hold. The average FIVE stock price target of $224.67 implies a mere 5.4% gain.

Tapestry (NYSE:TPR)

Tapestry is an upscale house of high-end brands such as Coach and Kate Spade New York. Most notably, the firm is best known for selling fashionable luxury handbags. Even with macro headwinds, high-end luxury firms have fared well in recent years. Tapestry has been more of a mixed bag (please, forgive the pun), with shares “roller-coastering” around over the decades. Nonetheless, I am bullish.

After a strong past year of performance (23.7% in gains), TPR stock has begun to stall, slowly correcting 13% over the last few months. Despite macro concerns, the company has levers to continue its growth. Most notably, the firm’s direct-to-consumer push and international expansion could help Tapestry make the most of its next cyclical upswing.

Further, the company is also starting to reap the rewards from previous efforts to improve the effectiveness of inventory management. Though Tapestry doesn’t sport the most expensive upscale brands on the planet, it can still shrug off inflation better than some of its less-premium peers.

Finally, the stock presents good value with a 2.8% dividend yield and 12.2 times trailing price-to-earnings multiple, which is far cheaper than the apparel and accessories industry average multiple of 26.7 times. Shares may be cheap with a decent yield, but fasten your seatbelt for wild swings. The 1.47 beta implies far more volatility than the market averages.

What is the Price Target for TPR Stock?

Tapestry sports a Strong Buy rating, with 12 Buys and four Holds assigned in the past three months. The average TPR stock price target of $51 implies 23.5% upside potential.

CVS Health (NYSE:CVS)

CVS is a popular drugstore chain that’s doing its best to become more of a healthcare company. The merger of Aetna opened many doors to the healthcare market, and other acquisitions (like Oak Street Health) have only further bolstered the firm’s healthcare position. I remain bullish on the stock due to its valuation.

While CVS shares are inexpensive compared to its competitors, it’s also important to note that the healthcare industry is difficult to navigate. CVS still has a lot to learn as it looks to make healthcare more affordable and accessible without taking too big a hit to its margins. Though I do think CVS will ultimately be successful with its health expansion, I acknowledge it could take a lot of time and effort for integration efforts to really pay off.

Not many were big fans of CVS’s $10.6 billion acquisition of primary-care firm Oak Street Health. Still, I think the sell-off in the name is becoming overdone. The stock is down 30% from its high, trading at 24.4 times trailing earnings. That’s well below the healthcare facilities industry average of 46 times.

For now, I view CVS as a compelling value play for long-term investors enticed by its 3.1% dividend yield. Just don’t expect any catalysts to send shares much higher over the medium term.

What is the Price Target for CVS Stock?

CVS has a Strong Buy consensus rating, with nine Buys and one Hold assigned in the past three months. The average CVS stock price target of $112.10 implies 49.6% upside potential.

Conclusion

Each consumer stock looks attractive here, according to most analysts. Out of the three stocks, however, Wall Street expects the most from CVS stock (by far).