Gold has shown high volatility this year as traders try to react to the coronavirus crisis. The metal started the year sedately, but began to rise in February as the crisis spread out of China.

Don't Miss our Black Friday Offers:

- Unlock your investing potential with TipRanks Premium - Now At 40% OFF!

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

As central banks inject money into the global economy via an unprecedented qualitative easing, and cut interest rates in an effort to restart economic activity, the mid- to long-term result will likely be steady increases inflation — a favorable environment for gold.

As Stifel analyst Tyron Breytenbach notes in his recent report on precious metals, “Gold has traditionally outperformed during periods of high inflation as a store of value and those producing it are likely to see the positive effect on their business.”

The analyst goes on to point out that demand for physical metal is also increasing, more even than traders’ demand for the ‘spot’ price. This demand for physical gold is a natural hedge against recessionary pressures, as customers with the means to do so are seeking a solid, and reliable, way to hold their money in negotiable form. Demand is also up for physical silver, which Breytenbach points out as a difference between central bank and retail interest in precious metals.

It’s clear that the stars are lining up for precious metals, and investors seeking to cash in have two routes available: they can buy physical metal, or they take a longer-term view, they can buy stock in metal producers.

With this in mind, we’ve used the TipRanks database to pick out three gold mining stocks that have shown a combination of strong attractions: recent outperformance of the broader markets, high upside potential, and strong overall gains in 2020.

SSR Mining, Inc. (SSRM)

Vancouver based SSR Mining focuses on precious metal mining, exploration, and development throughout the Americas. The company produces gold, silver, and other minerals, and markets them for industrial, pharmaceutical, minting, dentistry, and other commercial uses. Unlike most companies, which have seen heavy losses in Q1 due to the ongoing coronavirus pandemic, SSR Mining has seen sequential earnings gains in every quarter since Q4 2018.

In the company’s most recent report, for Q1 2020, EPS rose 3% to 31 cents per share – and more importantly, beat out the 27-cent estimate by 14%. Net earnings were just one measure of success in the quarter. The company also reported reduced debt levels, and a healthy cash-on-hand balance of $398.4 million. Positive results were supported by metal production, which reached 87,969 ounces of gold and 1.8 million ounces of silver for the quarter.

Also this month, SSR announced that it will enter a merger-of-equals agreement with competitor Alacer Gold. The agreement will allow the join entity to streamline operations and more efficiently allocate capital.

SSR Mining has seen a dramatic spike in share value since announcing the merger and reporting Q1 earnings, rising over 50% in the past two months.

B Riley FBR analyst Adam Graf notes that SSR Mining has seen headwinds recently – “As with other mines in Latin American and Canada, SSRM experienced government mandated temporary suspensions at Seabee and Puna operations.” – but that the company has the resources needed to master them. His bottom line on the stock: “We believe shares are well positioned to benefit from a rising gold price and increased investor interest as SSRM gains market cap and liquidity post the Alacer merger.”

Graf backs his Buy rating with a $44 price target, implying an eye-opening 132% upside potential to the stock. (To watch Graf’s track record, click here)

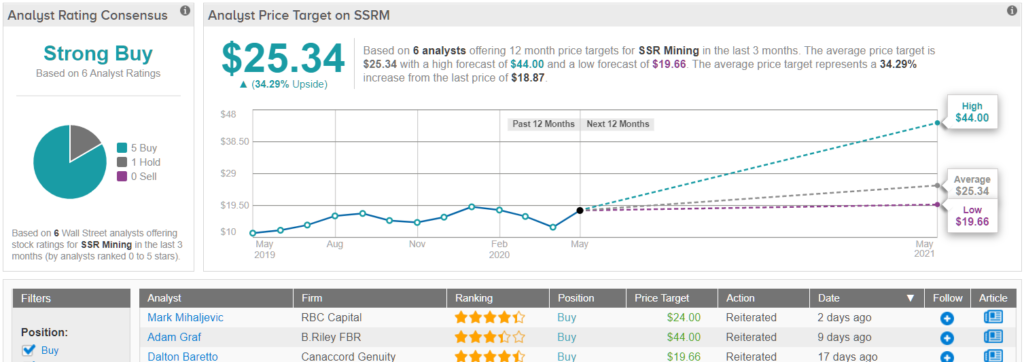

Not surprising, considering the high prospects here, SSRM shares have a unanimous Strong Buy rating from the analyst consensus, based on 5 recent bullish reviews. The stock is selling for $18.87, and the $25.34 one-year price target suggests room for 34% upside growth. (See SSR Mining stock analysis on TipRanks)

Pretium Resources (PVG)

The next stock on our list is Pretium Resources, another player in the Canadian gold mining scene. Specifically, the company owns the Brucejack mine in northern British Columbia, an asset which has produced 965,788 ounces of gold since 2017. Of that total, 82,888 ounces were produced in Q1 2020. PVG managed to continue operations in the quarter without disruption form the COVID-19 pandemic – social distancing restrictions put in place at the mine have allowed the company to report that, so far, they have no positive cases.

Corporate earnings have also been health. While Q1 saw a sequential decline (in part due to high expenses incurred against the pandemic), the 14 cents reported were 16% higher than expected. This steady performance – consistent production, an effective health response, and an earnings beat – have combined to push PVG shares up 20% from their February levels. Pretium has beaten the S&P’s bear market performance by a wide margin, and the stock continues to trend upwards.

Adam Graf, quoted above, also reviewed PVG. Noting the above points, he sums up this stock’s potential: “Going forward, we expect operational results to trend higher, driven by higher gold prices and rising ore grades, as well as benefit from a weakening C$ FX rate. Management maintains full year production and cost guidance… we expect the market to look at PVG with fresh eyes – awarding an improved valuation vs. the peer group.”

Graf’s $27 price target back up his Buy rating, and suggests that PVG has a stellar upside potential in the coming year of 212%. Not many companies, of any sort, can match that sort of return potential.

The analyst consensus on PVG is somewhat more cautious than Graf’s. The stock has a Moderate Buy consensus rating, based on 4 Buys and 4 Holds. Shares are selling for $8.68, and the $11.47 average price target implies a 32.5% upside potential. (See Pretium stock analysis on TipRanks)

Seabridge Gold (SA)

Last on our list is Seabridge Gold, part of Canada’s huge mining industry. The company’s projects are in western and northern Canada. During Q1, Seabridge announced a revised production outlook at its KSM project, in northern British Columbia. The new outlook includes a 44-year plan to recover up to 19.6 million ounces of gold and 5.4 billion pounds of copper.

SA shares saw shares climb 50% higher over the past 3 months, and one analyst is betting that this run can continue.

Covering Seabridge and its gold mine potential for Roth Capital, analyst Joe Reagor writes, “We believe the PEA clearly demonstrated the impact Iron Cap has on the project economics. We also believe Seabridge will need to complete significant additional drilling to incorporate Iron Cap in a future PFS.”

In line with his optimistic outlook, the analyst has raised his price target by 23%, to $21, suggesting an upside potential of 42% for the coming year. (To watch Reagor’s track record, click here)

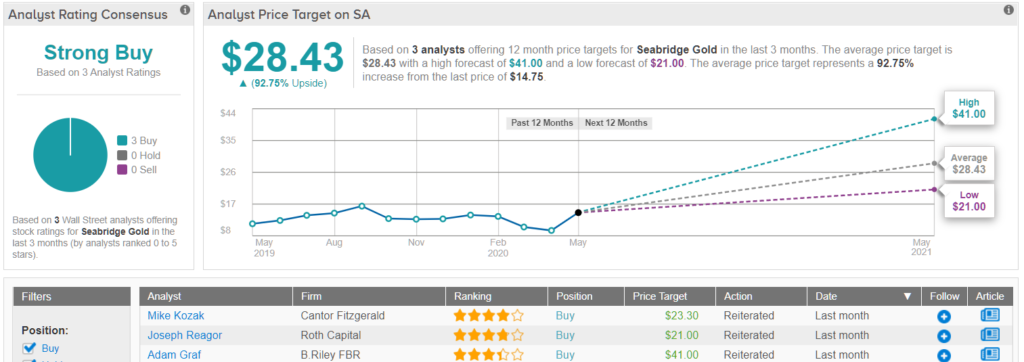

With 3 recent Buy reviews, the analyst consensus on Seabridge is another unanimous Strong Buy. Shares are currently trading at $14.75, while the average price target, of $28.43, incorporates the potential of the company’s gold reserves – and predicts a stellar 93% upside in the next 12 months. (See Seabridge stock analysis on TipRanks)

To find good ideas for gold stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.