Is it May 2020 or March 2009? As Wall Street observers traverse the confused economic environment, flashbacks of the Great Recession are coming to mind. Those looking at the glass half empty will point out the bear market that emerged took 18 months to reach the lowest point. However, the optimists are singing a different tune.

Among the bulls is Morgan Stanley’s head of U.S. equity strategy, Michael Wilson. In a recent note to clients, he argues that the current state of the market bears a striking resemblance to March 2009, the period in which the U.S. economy began to recover, with the S&P 500 embarking on what would become the longest bull-market run on record.

“Markets are tracking the Great Financial Crisis period very closely in many ways,” Wilson wrote. To support this claim, the strategist highlights the fact that stocks are bouncing back in a “similar pattern,” at the same time the amount of stocks, especially cyclicals, that have exceeded their 200-day moving average is on the rise. This is important as cyclicals usually lead the charge when a market recovery kicks off. Wilson also notes that the equity-risk premium, or the expected earnings yield for the S&P 500 minus the ten-year Treasury yield, looks the same as it did in March 2009, which played into his decision to call a stock-market bottom on March 16 of this year.

Taking Wilson’s views into consideration, risk-tolerant investors are on the hunt for promising names now trading at lower levels, specifically within the biotech space. As it just takes one positive catalyst like strong data or a favorable FDA ruling to send shares skyrocketing, massive returns are on the table. That being said, as the opposite also holds true, these stocks come with their fair share of risk.

Acknowledging the risk involved, we used TipRanks’ database to pinpoint compelling, yet affordable biotech stocks. We found three trading for under $5 that have not only received enough bullish recommendations from analysts to earn a “Strong Buy” consensus rating, but also sport colossal upside potential.

Gamida Cell Ltd. (GMDA)

It has certainly been a rough week for Gamida Cell, which develops therapies that could potentially cure blood cancers and other blood diseases.

On Tuesday, the company unveiled the pricing for its underwritten public offering of 13,333,334 ordinary shares, which landed at $4.50 per share. The fund raise sent shares tumbling, with GMDA walking away from the day’s trading session down 26%. However, the new share price, $4.42, offers an attractive entry point, according to the analyst community.

Weighing in for Oppenheimer, five-star analyst Mark Breidenbach cites recently released positive top-line data from its randomized Phase 3 trial of omidubicel in patients receiving bone marrow transplants as a key component of his bullish thesis. The trial had 125 participants between the ages of 12-65 with high-risk hematologic malignances (AML, CML, MDS, lymphoma), and GMDA’s candidate was studied against standard umbilical cord blood (UCB) grafts.

Not only did omidubicel meet its primary endpoint, but the asset’s failure rate came in at 4% while the UCBs had a failure rate of 12%. After the readout, the company announced that it plans on initiating a rolling BLA submission in the fourth quarter.

Expounding on the implications of the results, Breidenbach stated, “While expecting to see full results are at a medical meeting later this year (likely ASH), we believe these data could support a 2021 FDA approval and help spur uptake at transplant centers.” He added, “We believe omidubicel has been de-risked with the successful Phase 3 results.”

Adding to the good news, Breidenbach argues that the results show omidubicel is “competitive with more widely used grafts, including matched unrelated donor (MUD) and mismatched-related donor grafts.” He noted, “As such, these data may support wider adoption of omidubicel among transplant physicans, although longer follow-up will be required to assess relapse rates and treatment-related mortality.”

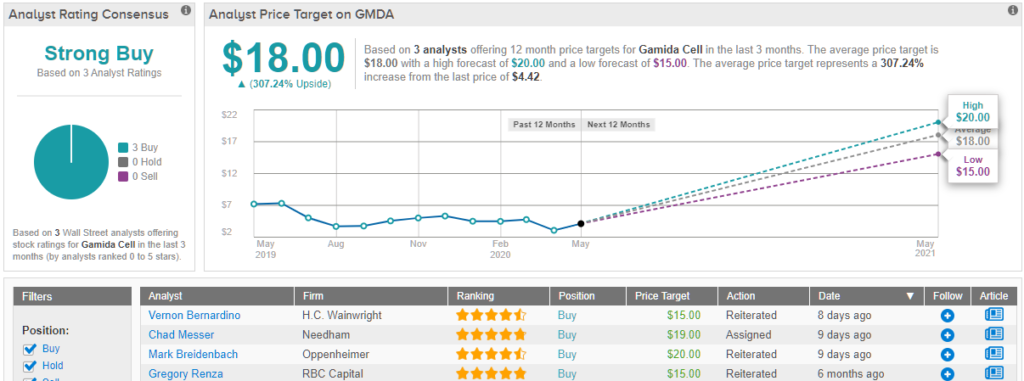

Based on all of the above, Breidenbach keep an Outperform (i.e. Buy) rating on the stock. Along with his bullish call, he also bumped up the price target from $18 to $20. This implies upside potential of a massive 352%. (To watch Breidenbach’s track record, click here)

Turning now to the rest of the Street, other analysts are on the same page. Only Buy ratings have been received in the last three months, 3, in fact, so the consensus rating is a Strong Buy. In addition, the $18 average price target puts the upside potential at 307%. (See Gamida Cell stock analysis on TipRanks)

VBI Vaccines (VBIV)

Using its enveloped virus-like particle (eVLP) platform, VBI Vaccines develops vaccines that could be capable of addressing unmet needs in infectious disease and immuno-oncology. With one analyst, Canaccord Genuity’s John Newman, expecting a “catalyst-rich” second half of the year for the company, its $2.49 share price could mean that now is the time to pull the trigger.

The five-star analyst tells investors the fourth quarter of 2020 will see VBIV submit regulatory approval filings for Sci-B-Vac, its vaccine against hepatitis B. These will be comprised of data from the CONSTANT and PROTECT Phase 3 trials in the U.S., Europe and Canada. “We continue to expect the agencies will view Sci-B-Vac’s regulatory applications favorably and expect approvals in 2021…We continue to believe a key factor for VBIV will be whether the Advisory Committee on Immunization Practices (ACIP) recommends Sci-B-Vac at a two-dose immunization schedule, for their commercial launch,” he commented.

As for its chronic hepatitis B virus (HBV) therapy, VBI-2601, initial human proof-of-concept data from the Phase 1b/2a study could be published in the second half of this year as well.

Looking at its VBI-1901 asset, which was designed for use in recurrent Glioblastoma Multiforme (rGBM) patients, expanded immunologic, tumor and clinical data from the GM-CSF arm and initial immunologic and tumor response data from the AS01B arm are slated for release mid-year and in Q4, respectively. “We look for continued positive data for VBI-1901 in GBM,” Newman said.

If that wasn’t enough, a pan-coronavirus vaccine is in the works, with VBIV expecting IND-enabling animal testing for the candidate, VBI-2901, to start in the second quarter. On top of this, the company could have clinical candidates selected and enough clinical supply ready in Q4 2020.

As VBIV’s operations through 2021 will most likely be supported by the $57.5 million equity raise last month and its $35.8 million in cash as of Q1 2020, it’s no wonder Newman is optimistic. In addition to maintaining a Buy recommendation, he did trim the price target by $1 to account for share dilution. That being said, the $3 figure still leaves room for a possible twelve-month gain of 20%. (To watch Newman’s track record, click here)

Do other analysts agree with Newman? As it turns out, they do. With 100% Street support, or 3 Buy ratings to be exact, the consensus is unanimous: VBIV is a Strong Buy. At $4.33, the average price target is more aggressive and suggests 74% upside potential. (See VBI Vaccines stock analysis on TipRanks)

Cyclacel Pharmaceuticals (CYCC)

The last biotech on our list, Cyclacel Pharmaceuticals, uses cell cycle, transcriptional regulation and DNA damage response biology to develop cancer therapies. Currently going for $4.59 apiece, some members of the Street are telling investors to get onboard before shares take off on an upward trajectory.

Writing for Roth Capital, analyst Jonathan Aschoff believes the strength of CYCC’s development program makes it a stand-out. The company is focused on solid tumors, with it conducting its clinical trials so that it can still report updated fadraciclib Phase 1 data with the higher frequency IV dosing schedule in advanced solid tumors, initial Phase 1 safety and PK results with oral fadraciclib as well as kick off its Phase 1/2 precision medicine trial in early 2021. It should be noted that oral fadraciclib has already demonstrated concordance with IV pharmacokinetics based on early clinical data.

With this strong technology, Aschoff argues that CYCC is targeting the unmet need in the cyclin E overexpressing tumors of the breast, endometrium/uterus and ovaries space. “The solid tumor program is key to our CYCC valuation, as projected revenue from this cyclin E overexpressing population represents more than 70% of projected revenue. We note that cyclin E is overexpressed in one-third of HR+ breast cancer patients resistant to first-line therapy, where patients could receive fadraciclib alone or potentially in combination with hormonal therapy. This population, combined with resistant second-line ovarian and endometrial/uterine cancer patients with high cyclin E amount to just over 100,000 patients in the U.S.,” he explained.

Additionally, CYCC is set to publish initial Phase 1 fadraciclib/ venetoclax results in rel/ref AML/MDS and CLL, initial Phase 1 sapacitabine/venetoclax results in rel/ref AML/MDS and initial Phase 1 CYC140 data in advanced leukemias. While Phase 1b/2 sapacitabine/olaparib results in BRCA mutant metastatic breast cancer are also expected, the timing is uncertain.

Some investors have expressed concern regarding COVID-19’s impact on the company’s trials, but Aschoff points out that thus far, CYCC hasn’t experienced any enrollment delays. He added, “CYCC recently announced its intent to study the potential of fadraciclib to be an early inhibitor of the detrimental inflammatory response observed in COVID-19 patients, specifically to induce MCL1 downregulation and apoptosis of inflammatory neutrophils.”

Consider all of this combined with its $27.3 million cash position that will support its development programs through 2022, and it makes sense why Aschoff remains squarely in the bull camp. To this end, he reiterated a Buy rating and $24 price target, indicating 423% upside potential. (To watch Aschoff’s track record, click here)

Like Aschoff, other analysts also take a bullish approach. CYCC’s Strong Buy consensus rating breaks down into 3 Buys and zero Holds or Sells. Given the $16.33 average price target, shares could soar 256% in the next year. (See Cyclacel stock analysis on TipRanks)

To find good ideas for biotech stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.