The key to profitable investing is building a profile that combines powerful potential with an economical point of entry. It’s a strategy that will frequently suggest a closer look at stocks in the micro- and small-cap size range, companies with valuations less than $2 billion. These smaller firms frequently feature share prices below $10, and triple-digit upsides to sweeten the pot.

Don't Miss our Black Friday Offers:

- Unlock your investing potential with TipRanks Premium - Now At 40% OFF!

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

Using TipRanks’ database, we’ve found two stocks that fit this profile: A market cap under $500 million and a share price below $10. Even better, these small-cap tickers have Strong Buy consensus ratings from the analyst community, and boast strong upside potential.

Spruce Biosciences (SPRB)

We’ll start with Spruce Biosciences, a small-cap biopharmaceutical company that has taken a specific focus for its developmental program. That focus is the treatment of rare endocrine disorder that have ‘significant unmet need’ – industry speak for ‘no current effective treatments.’ Spruce is working on the development and commercialization of tildacerfont, a potential treatment for congenital adrenal hyperplasia (CAH) in both adults and children, and for polycystic ovary syndrome (PCOS).

Tildacerfont is used in treating diseases characterized by excessive production of adrenocorticotropic hormone (ACTH), by binding to CRF1 receptor in the pituitary gland. The drug limits the production of adrenal androgens.

In June of this year, the company announced results from two Phase 2 clinical trials of tildacerfont in adult CAH. The results showed that tildacerfont was safe and well-tolerated – and better, that it pushed key hormone biomarkers toward normal levels in the baseline disease control group. In that group, levels of ACTH and A4 normalized in 60% and 40% of patients respectively. These results, from the Phase 2 trials, tend to support the ongoing late-stage trials of tildacerfont, CAHmelia-203 and CAHmelia-204.

Spruce entered the public trading markets last October, when the company closed out its IPO. The event was considered successful, as the company sold all 6.9 million shares offered – including the fully exercised underwriters’ options – at or above the initial price of $15 each. Share price, however, is down 45% in the months since.

Even though the share price is down, it was the initial positive data on tildacerfont that caught the attention of H.C. Wainwright analyst Raghuram Selvaraju. The analyst wrote in detail of tildacerfont’s potential – and noted the long-term profits possible in the company’s target market.

“Spruce is seeking to position tildacerfont in both treatment of CAH patients with poor disease control—for whom glucocorticoid (GC) agents are not working well—and CAH patients with good disease control, in whom GC agents are effective but for whom reduction in reliance on such drugs is highly desirable. We believe that tildacerfont could facilitate achievement of normalized steroid hormone levels in patients with poor disease control, while decreasing the levels of GCs that need to be administered in those with good disease control. As such, therefore, we consider tildacerfont capable of addressing a broad market opportunity within the CAH indication. This arena alone constitutes a $3B-a-year market opportunity,” Selvaraju opined.

In line with these comments, the analyst rates Spruce shares a Buy along with a $30 price target. Investors stand to take home about 220% gain, should the target be met over the next 12 months. (To watch Selvaraju’s track record, click here)

It appears the rest of the Street sees plenty of upside, too. Based on Buys only – 4, in fact – the analyst community rates SPRB a Strong Buy. The average price target hits $29.50, and implies potential upside of ~216% over the coming months. (See SPRB stock analysis on TipRanks)

Magenta Therapeutics (MGTA)

The second name we’ll look at is Magenta Therapeutics, a clinical-stage biopharma company focused on stem cell research. Stem cells are the natural precursors to every specialized cell in the body – and the transplantation processes that Magenta is working on aims to harness stem cells and use their unique developmental properties to kick-start the patients’ own physiological systems into regenerating and repairing disease-affected areas. Magenta is working on modes of harvesting, conditioning, and mobilizing stem cells for the treatment of autoimmune disorders, genetic diseases, and hematologic cancers.

The company has two key products in the pipeline. First, MGTA-145 is designed to work in the stem cell mobilization and collection step. The drug candidate is currently undergoing two Phase 2 clinical trials. One is testing its efficacy in the stem cell treatment process for hematological cancer multiple myeloma. This is being conducted in combination with the existing drug plerixafor, and preliminary results from the 25-patient study are expected in 2H21.

The second Phase 2 trial for MGTA-145 is a collaboration with the National Marrow Donor Program, and is examining MGTA-145’s use for patients with acute myeloid leukemia (AML), acute lymphocytic leukemia, and myelodysplastic syndromes (MDS). As with the study above, this is being conducted in combination with plerixafor and initial data are expected in the second half of this year.

Also in 2H21, Magenta will initiate a Phase 2 study of MGTA-145 in the treatment of sickle cell disease.

The company’s second drug candidate, MGTA-117, has been in the news lately – and not for good reasons. On Wednesday, Magenta announced a clinical hold on the investigational new drug (IND) application for MGTA-117. As a reminder, the IND was filed to initiate a Phase 1/2 trial of MGTA-117 in acute myeloid leukemia (AML) and myelodysplastic syndrome (MDS). The FDA is now requesting a bioassay to help inform dose escalation during the company’s initial study in patients with hematologic malignancies. The company does not believe this bioassay is a significant technical hurdle but now anticipates starting the Phase 1/2 study in 4Q21, a roughly one quarter delay.

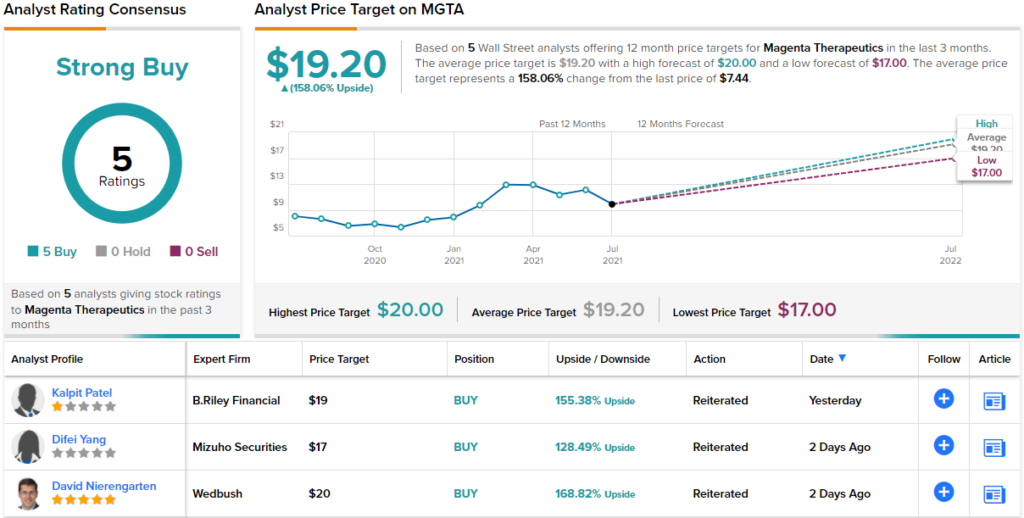

Covering MGTA for B. Riley, analyst Kalpit Patel believes the company’s fundamentals remain intact.

“While the clinical hold serves as a minor setback in terms of development timelines, we are encouraged that the hiccup is unrelated to any toxicology or manufacturing issues. Our fundamental thesis that ‘117 could increase the proportion of patients eligible to receive transplants and gene therapies remains unchanged,” Patel noted.

The analyst added, “In terms of next catalysts, a final clinical update of MGTA-145 for autologous stem cell mobilization in multiple myeloma is expected in 2H21. In addition, initial mobilization clinical data for the allogeneic study in leukemia are also slated to readout in 2H21. Based on promising early mobilization data, we estimate results from the allogeneic study to at least match the efficacy unveiled in the autologous setting.”

These comments back up Patel’s Buy rating on the stock, and his $19 price target implies a robust upside potential of 155% for the year ahead. (To watch Patel’s track record, click here)

There is evidence that Wall Street’s biotech analysts agree with Nealon here; the stock has a unanimous Strong Buy consensus rating, based on 5 positive reviews. The shares are currently trading for $7.44; their average price target of $19.20 indicates room for ~158% growth on the path ahead. (See MGTA stock analysis on TipRanks)

Read more: 3 Stocks JPMorgan Says Are Ready to Rip Higher

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.