What to do in today’s market? The last few trading sessions of declining stocks would seem to indicate that the late-May rally we saw has run its course. But that doesn’t mean the opportunities for buy-minded investors are all gone.

The recent declines, and the overall downward trend we’ve seen year-to-date, have left many fundamentally sound stocks trading at rock bottom prices. And that may have created an opportunity for investors willing do a bit of bottom fishing.

The trick for investors, however, is to tell the difference between stocks that are cheap at their new low prices and stocks that are truly broken. That’s where the Wall Street pros come in.

These expert stock pickers have identified two compelling tickers whose current share prices land close to their 52-week lows. Noting that each is set to take back off on an upward trajectory, the analysts see an attractive entry point. Using TipRanks’ database, we found out that the analyst consensus has rated both a Strong Buy, with major upside potential also on tap. We’re talking about over 100% upside potential here.

SeaSpine Holdings (SPNE)

The first stock we’ll look at is SeaSpine Holdings, a medical technology company focusing on the treatment of injuries and disorders of the spine. The company uses a series of advanced materials and techniques to develop a range of surgical implants and procedures, including orthobiologics and spinal fusion hardware, to meet the needs of orthopedic and neurosurgical specialists.

SeaSpine offers solutions for anterior and posterior spinal fusions, along with surgical access and navigation technologies for a wide range of operations. In recent months, the company has announced the commercial launches of new products, such as the Explorer TLIF Oblique TO, Expandable Interbody system, the WaveForm TO system, and the OsteoTorrent DBM product family. These new launches continue SeaSpine’s history of offering best-in-class products.

Last year, SeaSpine moved to shore up its product lines, through the acquisition of Toronto-based 7D Surgical. The acquisition brought 7D’s Flash Navigation into SeaSpine’s range of offerings.

The company’s strong product line supports its growing revenue stream. The company reported $50.7 million in global revenues for 1Q22, up 21% from the year-ago quarter. Of this total, $45.5 million came from US sales. The revenue totals beat the forecast by 3.5%, which helped to compensate for somewhat disappointing earnings in the quarter. EPS was reported at a net loss of 45 cents per share, well below the 36-cent estimate.

SeaSpine had $81.4 million in cash assets on hand at the end of Q1, a total that included $25 million borrowed against an existing credit facility. SeaSpine’s credit limit on that facility was set at $30 million, and the company is negotiating to expand it to $40 million.

Looking ahead, the company is predicting year-over-year revenue growth of 21% to 23% for the full year 2022. This represents an increase of the guidance range by $5 million at the midpoint, to $231 million to $235 million. While the company’s outlook appears positive, its stock shares are down 46% so far this year.

However, Piper Sandler analyst Matt O’Brien thinks this new, lower stock price could offer new investors an opportunity to get into SPNE on the cheap.

“SeaSpine is experiencing strong recovery in volumes following COVID and has seen encouraging signs so far with the launch of 7D. This includes 4 earnouts now signed representing up to $2M of annual revenue as well as some of the first signs of implant pull through in select accounts that have purchased the system outright. Enabling technologies have been a big source of value creation for others in the ortho space, and we expect 7D to provide a similar boost to SPNE,” O’Brien opined.

“Simply put, we believe SPNE has the right leadership and strategy, coupled with an impressive product offering, to continue delivering some of the best growth in spine,” the analyst summed up.

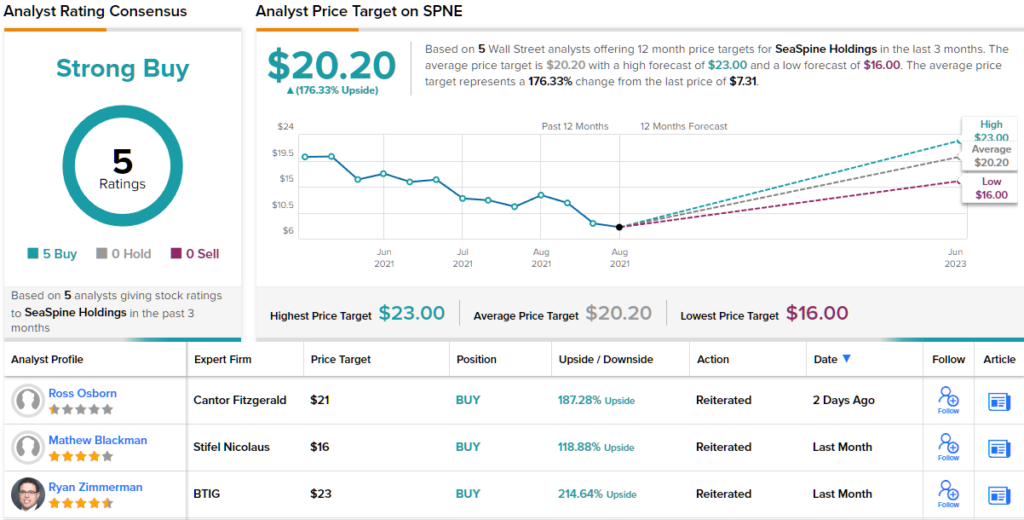

All of that is enough to back up an Overweight (i.e. Buy) rating, and O’Brien’s price target, at $21, implies a one-year upside of 187% for the year ahead. (To watch O’Brien’s track record, click here)

The bulls are out in for this stock, who’s Strong Buy consensus rating is based on 5 unanimously positive analyst reviews. The current share price of $7.31 and the average price target of $20.20 together suggests an upside of 176% for the next 12 months. (See SPNE stock forecast on TipRanks)

Organogenesis Holdings (ORGO)

For the second stock on our list, we’ll stick with the medical technology sector. Organogenesis Holdings works in the field of regenerative medicine, where it develops, manufactures, and commercializes products for advanced wound care and surgical & sports medicines. The company focuses on products to promote both patient support and regenerative medicine.

The company’s wound product lines include the PuraPly and NuShield families of dressings, designed to promote faster healing and prevent infection, along with the Affinity and Apligraf lines of living cell therapies, for the treatment of various types and sizes of wounds. The same products are also used in the surgical and sports medicine field, which also includes Osteoconductive Matrix PLUS cancellous chips and the FiberOS lines of demineralized cortical fibers.

Organogenesis’ revenues grew from 2020 through 2021, but dropped off in 1Q22. The top line for the first quarter came in at $98.1 million, down from the $128.5 million reported in 4Q21 – and also down slightly from the $102.5 million in 1Q21. The company’s total sales were impacted by a 39% year-over-year decrease in the surgical & sports medicine lines that was partly offset by a 29% increase in y/y PuraPly sales.

Unfortunately for investors, Organogenesis stock has been falling, and is down 45% this year. Nevertheless, SVB Securities analyst Danielle Antalffy sees plenty of reasons to stay hopeful.

“With reimbursement noise seemingly behind us, a tough COVID operating environment hopefully improving as we move through 2022… we hope that investors will increasingly shift focus to the positive underlying growth drivers of the business, which we believe will return the company to a sustainable double-digit sales growth trajectory in 2023 if not in 2022. These growth drivers include the amnion portfolio, as well as sales force expansion and channel expansion — all of which widen ORGO’s competitive moat and successfully position the company for sustained above-market growth,” Antalffy wrote.

To this end, Antalfy puts an Outperform (i.e. Buy) rating on ORGO stock, along with a $13 price target to suggests a growth potential of 154% by next year. (To watch Antalfy’s track record, click here)

Other analysts don’t beg to differ. With 4 Buy ratings and no Holds or Sells, the word on the Street is that ORGO is a Strong Buy. The shares have an average price target of $16.75, suggesting a 12-month upside of ~228% from current levels. (See ORGO stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.