Volatility, and descending trends, that’s the path the markets are taking these days. While the usual headwinds are all in play, the chief worry now is coming from Eastern Europe. Will Russia invade, or won’t it?

A shooting conflict, involving a superpower, taking place in one of Europe’s most agriculturally productive and mineral-rich countries, has huge potential for political and economic fallout, enough to keep pundits and market watchers awake at night. But an in-depth analysis of geopolitical events over the past several decades, by Truist Advisory, would suggest that investors may not need to worry quite so much.

The firm looked at 12 major events, including the Cuban missile crisis of 1962, the Iran hostage crisis of 1979, and the Iraq War of 2003, and followed market fluctuations for a year after each event. On average, the S&P 500 gained 8.6% in the ‘post-event’ period; the index posted a one-year gain in 9 of the 12 periods examined.

Truist’s co-chief investment officer, Keith Lerner, sums up this findings, saying, “When you look at the history of geopolitical events, they tend to have a short-term impact on the markets, and as long as they don’t drive you into recession, then the markets tend to rebound… The conclusion is that we don’t think investors should overreact to this situation by itself.”

With all of this in mind, let’s take a look at two stocks that have shown sharp losses recently – and are still showing substantial upside, suggesting they may jump when the geopolitical situation calms down. According to the latest TipRanks data, both are Strong Buy stocks, and both show potential for triple-digit percentage gains in the coming months.

Porch Group (PRCH)

The first stock we’re looking at is Porch Group, an online service company offering software and platforms that connect homeowners with the services they need to maintain and improve their properties. These include home improvement and warranty, contracting, moving, and home inspection. Taken together, Porch can connect customers with service providers in every segment of the $500 billion annual home improvement market.

The company went public, in December of 2020, through a SPAC transaction, and the shares saw a volatile 2021 before falling sharply from their November peak into the beginning of this year. The stock is down 68% from that peak.

It’s important to note, however, that even as Porch’s share price has declined the company has continued to execute on its expansionary strategy. It announced in December the addition of the newest module in its software offerings for home inspection services, the Inspection Support Network. The new module allows homebuyers and agents to pay for inspections at the home closing.

In another expansion move, in January, the company’s property and casualty insurance subsidiary Homeowners of America (HOA) announced that it is introducing services in New Mexico and Montana. HOA now operates in 14 states.

Porch’s expansion continues, and the company is looking forward to its 4Q21 earnings release, set for March 1. In the last release, for 3Q21, the company increased its full-year 2021 revenue guidance from $187.5 million to $195 million. Achieving the new guidance will put the company on track for 170% year-over-year revenue growth.

Looking at Porch for Berenberg Bank, analyst Nate Crosset gives an upbeat take on the broad picture.

“PRCH’s differentiated business model essentially gives home service providers early access to high-intent customers (i.e., new homebuyers), delivering solid growth. The company has a substantial TAM with low penetration, which we believe leaves room for growth, while continued M&A execution could increase the TAM. Lastly, we believe the Street is underappreciating PRCH’s differentiated business model and solid growth; we think PRCH deserves a higher multiple,” Crosset opined.

Crosset thinks the stock has some way to go, and by some way, we mean 157% of upside. Those are the returns investors are looking at, should the stock make it all the way to Crosset’s $21 price target. No need to add, the analyst’s rating is a Buy. (To watch Crossett’s track record, click here)

Overall, even though this stock’s price is down, the analysts remain bullish; PRCH has 4 positive reviews for a unanimous Strong Buy consensus rating. The shares are selling for $8.15 and their $21.63 average price target suggests a strong upside of 165% for the year ahead. (See PRCH stock forecast at TipRanks)

Renewable Energy Group (REGI)

From homes, we’ll turn to energy. Renewable Energy Group, REGI, is in the biofuel business, producing renewable fuels for a variety of markets. The company has facilities to produce, distribute, and retail a wide range of fuels, including biodiesel and other transportation fuels, oils for blended heating fuels, and bio-based glycerine and methyl esters for industrial and agricultural uses. The company has 12 biorefineries — ten located in the United States and two in Germany. Eleven of its biorefineries produce biodiesel, while its Geismar, LA biorefinery produces renewable diesel.

These assets have allowed REGI to post two consecutive quarters (2Q21 and 3Q21) of rising revenues. The 3Q21 result, the last reported, of $1.01 billion was up 22% from Q2, and an impressive 73% year-over-year. The company attributed the gains to ‘higher average selling prices’ in the past six months. Earnings per share also rose, although not as much as revenues. The 83 cent EPS reports in Q3 was up from 60 cents (a gain of 38%), but was only half the Q2 value of $1.62. The divergence reflects the volatile nature of the fuel industry.

In recent weeks, REGI has been expanding its operations. In January, the company acquired Amber resources, a California-based distributor of gasoline, diesel, lubricating oils, and other transportation fuel components. The move adds more than 60 million gallons per year of sales to REGI’s portfolio.

In February, the company made two important announcement. First, that it will be investing in a pretreatment facility in Germany, in a project in Emden. The project will improve REGI’s ability to refine low-carbon-intensity, hard-to-convert waste fats and oils for biodiesel production in the European markets. And in the US markets, REGI has entered into a partnership with Bunker Holding Group, the world’s largest marine fuel supplier. The move will expand REGI’s footprint in the US and EU markets for marine biodiesel fuels.

Despite the company’s rising revenues and continued profitability, REGI has seen its share price drop 65% over the past 12 months. In coverage for Cowen, analyst Jason Gabelman explains why he sees this drop as an opportunity for investors.

“We estimate REGI is getting 0 value for its biodiesel business (ex volumes sold with RD), and see current price levels as an attractive entry point, especially for those willing to wait until Geismar value is more reflected in equity. The stock could also benefit as investors embed value for Cali’s cap-and-trade,” Gabelman noted.

“The stock has been impacted by concerns around Renewable Volume Obligations (RVOs) and declining LCFS prices. Proposed RVOs should accommodate new biomass-based diesel coming online in ’22, reducing competitive risk to REGI’s biodiesel business,” the analyst added.

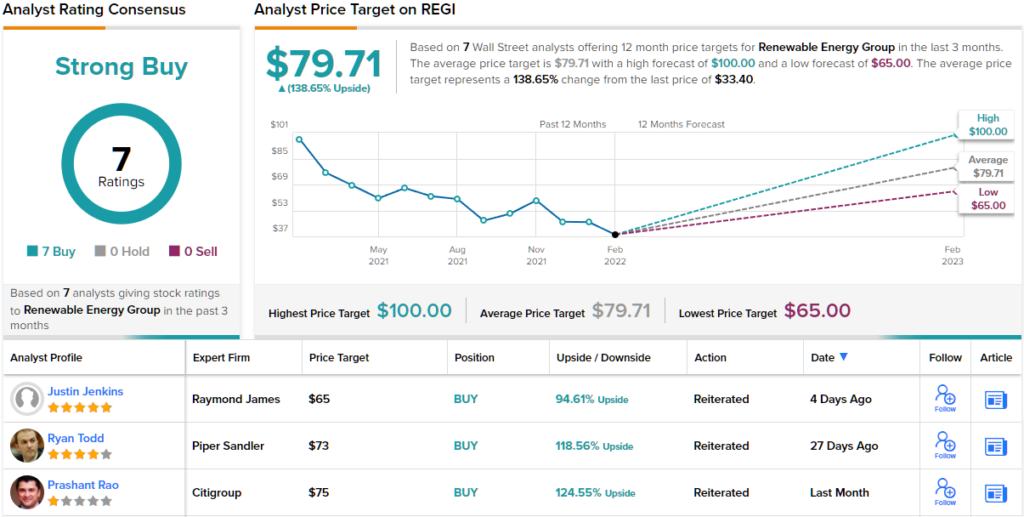

To this end, Gabelman sets an Outperform (i.e. Buy) rating on REGI, and his $75 price target indicates its potential for ~125% upside by the end of 2022. (To watch Gabelman’s track record, click here)

Overall, REGI has managed to pick up a unanimous Strong Buy consensus rating from Wall Street, based on 7 positive reviews. The stock is selling for $33.40 and the $79.71 average price target implies ~139% upside from that level. (See REGI stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

Questions or Comments about the article? Write to editor@tipranks.com