The energy sector’s production companies benefit from dealing in commodities – oil and gas – that are always in demand. They have high overhead, but they also have a ready market for the product and consequent strong cash positions.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

Using that strong cash-flow, the companies have been following two strategies to boost their shares; First, they are simply buying back shares to support the price. And second, they are paying out high dividend yields, offering investors a steady income stream from the stocks. Average dividend yield in the energy sector is up to 4%, almost double the S&P 500’s average yield of 2.1%.

With this in mind, we’ll take a closer look at two Strong Buy energy stocks, according to the analyst community, that are paying out dividends well above the average – bringing investors the gift of a 7% yield. Using the TipRanks database, we’ve looked up the details, and we’ll flesh them out with some recent analyst commentary.

Kimbell Royalty Partners (KRP)

We’ll start with a look at Kimbell Royalty Partners. This company combines both real estate and energy investing; Kimbell invests in land, specifically, the mineral extraction rights on land-acres in known petrochemical producing basins. The company’s portfolio holds interests in over 13 million acres in 28 states, and includes properties in all of the major onshore oil and gas basins in the US. Kimbell boasts over 97,000 wells, with its largest presence – some 41,000 active wells – in Texas’ Permian Basin.

In 2021, Kimbell saw its earnings situation switch from deep losses to small gains. From 4Q20 to 1Q21, the EPS loss shrank from $1.66 to a mere 2 cents, and in Q2 the company reported a modest 4-cent EPS gain. At the top line, revenues troughed in 2Q20, and have been rising steadily ever since. The Q2 revenues from oil, gas, and natural gas liquids came in at $39 million, the highest in over two years.

Rising revenues and earnings have supported a return to strong dividends. Management was forced to cut back on dividend payments early in the corona crisis – but that was a less of a setback than it seemed, as the company has a history of adjusting dividend payments to keep them in accord with income. Since second quarter of last year, Kimbell has raised the dividend three times. The current payment, of 31 cents per common share, annualizes to $1.24 and gives a yield of 7.41%.

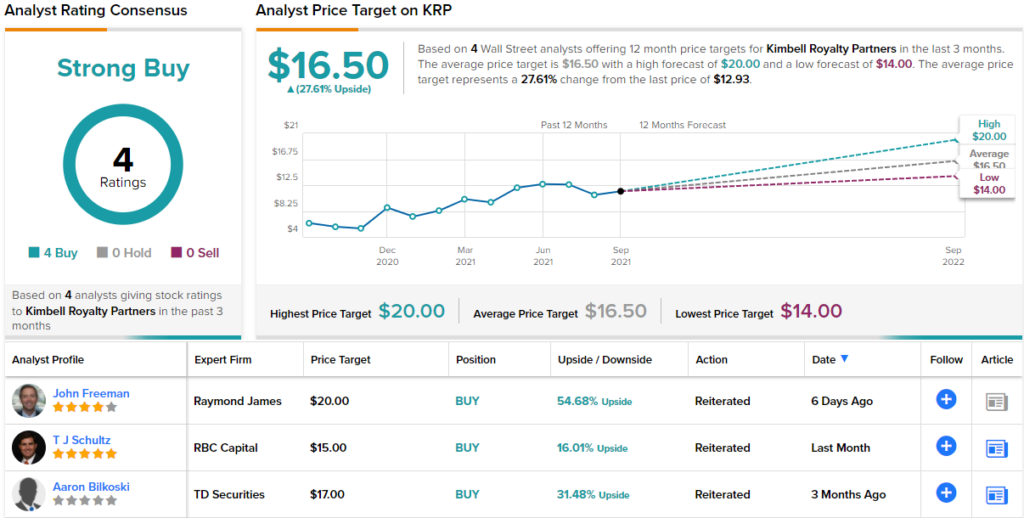

Covering Kimbell for Raymond James, analyst John Freeman notes the dividend as a key factor.

“For 2Q, KRP declared a dividend of $0.31/share, a ~15% increase q/q, amounting to 75% of distributable cash flow (remaining 25% used to reduce debt). We expect this ratio to remain constant through 2H21, with 3Q/4Q projected distributions of ~$0.27/~$0.28 per-share, respectively. This amounts to a FY2021 dividend of ~$1.13/share equating to an ~11% dividend yield! Keep in mind this dividend is tax free… Hard to imagine there are many opportunities any better than scooping up shares in an 11%+ tax free yield,” Freeman opined.

These comments back up Freeman’s Strong Buy rating, and his $20 price target implies a one-year upside potential of ~55%. (To watch Freeman’s track record, click here)

Wall Street is in general agreement with Freeman’s views here, as shown by the unanimous Strong Buy consensus rating on the stock. Kimbell’s shares are priced at $12.93 and the $16.50 average price target gives a 28% upside for the year ahead. (See KRP stock analysis on TipRanks)

Hess Midstream Operations (HESM)

Next up is Hess Midstream, one of the many companies that lives in the so-called midstream sector of the energy industry, moving oil, natural gas, natural gas liquids, and refined petroleum products from wellheads and refineries to storage facilities, transport terminals, and end users. Hess has a range of assets, covering gathering, processing & storage, and terminaling & export, based in the rich Bakken formation of North Dakota.

Hess reported gains in the second quarter of this year, with $162 million in net income, compared to $107.8 million in the year-ago quarter. Per share, the income came to 44 cents, up 51% from 2Q20. Turing to the top line, Hess reported $294 million in total revenues. This was about 9% above the prior year’s second quarter, and the highest result in the last two years. Revenues have increased in each of the last three quarters.

On interest to dividend investors, Hess reported distributable cash flow in Q2 of $207.5 million. This supported a 50 cent dividend payment to common shareholders. At $2 annualized, the dividend yields 7.8%. Hess has been raising its dividend payment regularly over the past few years, COVID or no COVID.

Analyst Alonso Guerra-Garcia, writing from Scotiabank, sees plenty of reason for optimism in Hess Midstream.

“This year, we’ve continued to see outperformance in HESM’s operational results as gas capture has outpaced expectations,” Garcia noted. “HESM hits the right note on return of capital, while optimizing (and continuing to delever) the balance sheet, and maintains the financial flexibility to return additional capital. Increased activity in the Bakken with HES’s third rig (potentially fourth next year) also sets up for continued growth long-term.”

To this end, Garcia puts a $29 price target here, indicating room for 12% upside in the next 12 months. Based on the current dividend yield and the expected price appreciation, the stock has ~20% potential total return profile. (To watch Garcia’s track record, click here)

Overall, there are 5 ratings on Hess Midstream, and they include 4 Buys and 1 Hold, for a Strong Buy consensus from the analysts. HESM shares are priced at $25.87 and the average price target of $28.60 implies ~11% upside going into next year. (See HESM stock analysis on TipRanks)

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.