The 1H20, after the coronavirus crisis and the economic downturn, was a true black swan. Yet, markets are on the upswing, with the NASDAQ near record highs and the S&P 500 holding above 3,200. It’s a positive sign, and a welcome one as we enter the Q2 earnings season. Investors are both cautious and guardedly optimistic going in.

The second quarter saw some serious turbulence as headwinds and tailwinds collided. Among the headwinds: the lockdowns of March and the dreaded ‘second wave’ of the virus in June. The tailwinds included the lifting of restrictions in May, and the restarting of economic activity. Initial results are showing that Q2 earnings were not as grim as Q1. The question now is, is it sustainable?

We just don’t know. And that makes dividend stocks, the classic defensive play, look better every day. Using TipRanks database, we identified three stocks that have maintained their dividend payments even during the height of pandemic. They are yielding at least 5%, and are backed by enough analysts to earn a “Strong Buy” consensus rating.

NexPoint Real Estate Finance (NREF)

The first stock on our list is a newcomer to the markets. NexPoint, a real estate investment trust focused on mortgage loans for single- and multi-family residential rental units, went public this past February. While the IPO, of $19 per share, was at the low end of the initial range, the offering was successful with 5 million shares sold bringing in $95 million.

Since then, NexPoint has had the bad luck to run headlong into the coronavirus-inspired economic downturn. With million laid off or unemployed, rental owners have had a hard time collecting from tenants, leading to difficulties for the mortgage holders. Even in this difficult climate, however, NREF was able to beat the earnings forecast, and report 23 cents EPS against the forecast of 22 cents.

Meeting earnings expectations allowed the company to meet its dividend obligations, as well. NREF declared its Q1 dividend payment on the same day it released earnings figures, and paid the dividend out at 40 cents per share on June 30. This payment annualizes to $1.60 and gives an excellent yield of 10.6%. Compare that to the ~2% average yield found among S&P listed companies, and the attraction here is clear.

Covering this stock for Raymond James, analyst Stephen Laws writes, “…NREF [has a] high quality portfolio of stabilized, long-duration investments, which we believe results in better earnings visibility than peers. NREF’s portfolio does not have any land or construction loans or any loans collateralized by hotel, retail, or office properties. We believe shares should trade roughly in line with book value as we believe the company is well positioned to capitalize on the stressed market environment given the recent capital raise.”

To this end, Laws rates NREF a Strong Buy along with an $18 price target, suggesting it has room for 19% growth in the coming year. (To watch Laws’ track record, click here)

Overall, NREF shares have a unanimous Strong Buy analyst consensus rating, a show of confidence by Wall Street’s analyst corps. The stock is selling for $15.11, and the average price target of $18.50 implies 22% growth in the year ahead. (See NREF stock analysis on TipRanks)

TPG RE Finance Trust (TRTX)

For our next stock, we’ll stick with the REIT sector. TPG RE Finance was sponsored by global asset firm TPG, to handle commercial real estate financing. TRTX has a portfolio worth over $5.8 billion, and its properties are mainly multi-family dwellings or office space, along with significant exposure to hotels and mixed-used properties.

Business closures and mass unemployment put enormous pressure on most apartment- and office exposed REITs in the first half of the year, and TRTX was no exception. The company saw Q1 earnings plummet to negative territory, and reported a $2.20 loss per share. Nevertheless, TRTX has chosen to keep up its dividend payments.

It was not a light decision, nor was it easy to carry out. The company’s Q1 dividend, which had been suspended, was restored at the previously declared 43 cents per share, while the Q2 payment was cut back to 20 cents. The cut to the dividend was made to keep the payment better in line with share value. After the cut, TRTX’s dividend offers a yield of 10.2%. It’s important to remember here that TRTX’s shares have really recovered their value from the market crash earlier this year.

JMP’s 5-star analyst Steven DeLaney notes the dividend – and TRTX’s commitment to it – in his recent note on the stock. He writes, “[The] new lower cash dividend suggests a cautiously prudent approach in the near term. On June 17, the company announced that the 2Q dividend will be $0.20 per share and a decline of 53% from the prior $0.43. Additionally, the temporarily suspended 1Q dividend of $0.43 will be paid in cash on July 14. We believe the new quarterly dividend level is appropriate to preserve liquidity ahead of some level of expected credit workouts in the loan portfolio.”

On the strength of the dividend and the company’s forward prospect, DeLaney rates TRTX a Buy. His $10 price target show confidence in a 24% one-year upside growth potential. (To watch DeLaney’s track record, click here)

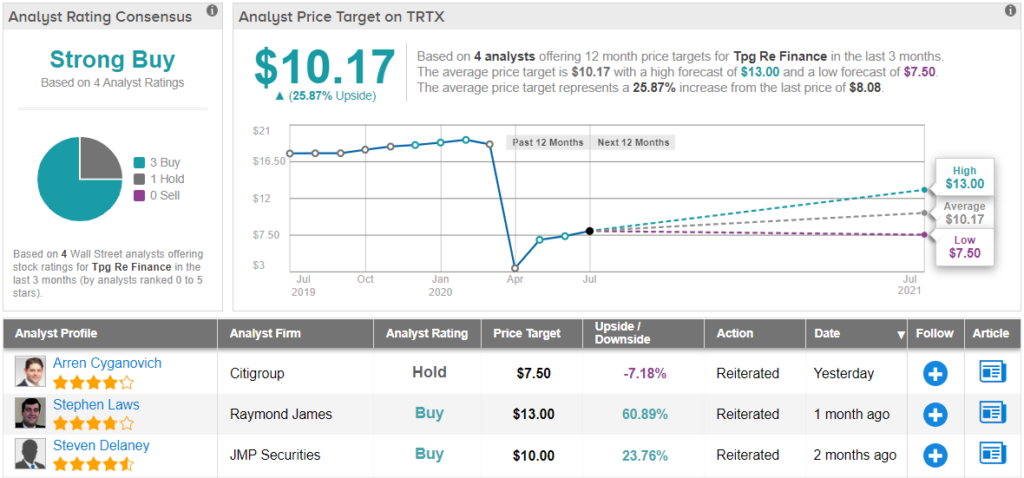

Wall Street agrees with DeLaney; that much is clear from the aggregate data. TRTX has a Strong Buy rating from the analyst consensus, based on 3 Buys and 1 Hold. Shares are priced at $8.08 and have an average price target of $10.17, suggesting nearly 26% upside. (See TRTX stock analysis on TipRanks)

CatchMark Timber (CTT)

The last stock on our list is another REIT, but with a twist. CatchMark invests in timber lands, mainly in or near the major mill markets in the US. The company owns 1.5 million prime acres, in Oregon as well as across the Southeast and South, from the Carolinas through to Texas. CatchMark owns the lands and the timber on them, but does not deal with the derivative forest products or the manufacturing processes.

The company showed a net loss in Q1 – of 9 cents per share – but set in the context of recent quarters, that was not a bad performance. The company has been reporting EPS losses since 2018, but typically sees those losses mitigate sequentially. This past Q1 was no exception; the 9-cent EPS loss was an improvement from the previous quarter’s 24 cent loss. CatchMark will report Q2 earnings in August.

At the same time that CatchMark reported Q1 earnings, it also declared the Q2 dividend. The payment remains steady at 13.5 cents per share, yielding a strong 5.5%. The company has a 6-year history of keeping up its dividend payments, in all economic conditions.

5-star analyst Paul Quinn, from RBC, sees CatchMark as a strong defensive play for more than just dividend. He writes, “With so much uncertainty in the world today, we see Timberlands as an attractive asset class due to their steady income characteristics and long lifespan. Given CatchMark’s pure-play Timberland status and exposure to attractive markets in the US South, we expect that the company will screen increasingly well to investors….”

Quinn backs this with a $10 price target, suggesting room for a modest 2% growth. (To watch Quinn’s track record, click here)

Once again, the analyst is in sync with Wall Street’s collective view. The analyst consensus here is a Strong Buy, and it is unanimous: all three of the recent reviews on this stock come down to Buy. The shares are selling for $9.75, and the average price target is $10. This suggests that the stock’s recent appreciation may force analysts to reassess their targets in the near future. (See CatchMark stock analysis on TipRanks)

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.