This year has seen a strong bullish trend that has hit the skids in the last couple of months, resulting in a pullback from recent highs and an increase in volatility. For the retail investor, the main result is a tougher environment for finding just the right stock.

That’s where Wall Street’s top analysts come in. These stock pros have built solid reputations for finding those right stocks – in any conditions.

Covering the tech sector for Needham, analyst Quinn Bolton stands head and shoulders above his peers. Bolton, who holds the #4 ranking overall out of more than 8,500 stock analysts, is the Street’s top tech expert. His ratings have a 67% success rate, and an investor who had followed Bolton’s recommendations over the past year would have realized a return of 36.3%.

So it would seem that when Bolton talks, investors should listen. We’re going to do just that now, opening the TipRanks database to find the latest details on two semiconductor chip stocks that Bolton has recommended lately. In fact, Bolton is not the only one singing these stocks’ praises. According to TipRanks, they are both rated as ‘Strong Buys’ by the analyst consensus. Let’s take a closer look.

Lattice Semiconductor (LSCC)

The first of Bolton’s picks is Lattice Semiconductor, an Oregon-based firm that specializes in low power programmable semiconductor chips, with product lines designed to solve customer problems in the automotive, communications, computing, consumer, and industrial markets.

This is one of the smaller chip companies, with a market cap just $10 billion, but it realized some $646 million in revenues last year. The company has a strong customer list, including a score of important manufacturing firms in North America. Lattice has pulled off an important coup in recent years, maintaining a steady upward trend in both revenues and earnings every quarter.

Lattice has staked out a niche in the market for FPGAs, field-programmable gate array chips. These specialized semiconductor chips are found in a wide range of products and are used particularly in edge computing, AI apps, robotics, IoT, and autonomous driving systems. The chips can be reprogrammed multiple times, allowing customers to purchase one set – a major cost saver as design needs change, and an important growth factor in this market.

That addressable market growth has powered Lattice’s recent successes. The company’s 2Q23 revenues, the last reported, came to $190.1 million, $2.76 million over the forecast, and up almost 18% year-over-year. The company’s bottom line, a non-GAAP earnings figure of 52 cents per diluted share, was 1-cent better than had been expected.

Covering Lattice for Needham, top analyst Bolton is impressed by the company’s leadership, its solid niche position, and its recent growth. He writes: “Under the leadership team of Jim Anderson, CEO, Lattice has expanded its low-end FPGA product portfolio with its Nexus platform and is more than doubling its TAM by entering the mid-range FPGA segment with its Avant platform. We believe the company will generate multi-year double-digit revenue growth. Despite not being a direct play on AI, we believe the company should trade at a premium to its peers based on strong organic growth expectations, diversified customers, exposure to attractive end-markets and geographies, industry-leading gross and operating margins, sticky wins and lack of political/export control risk.”

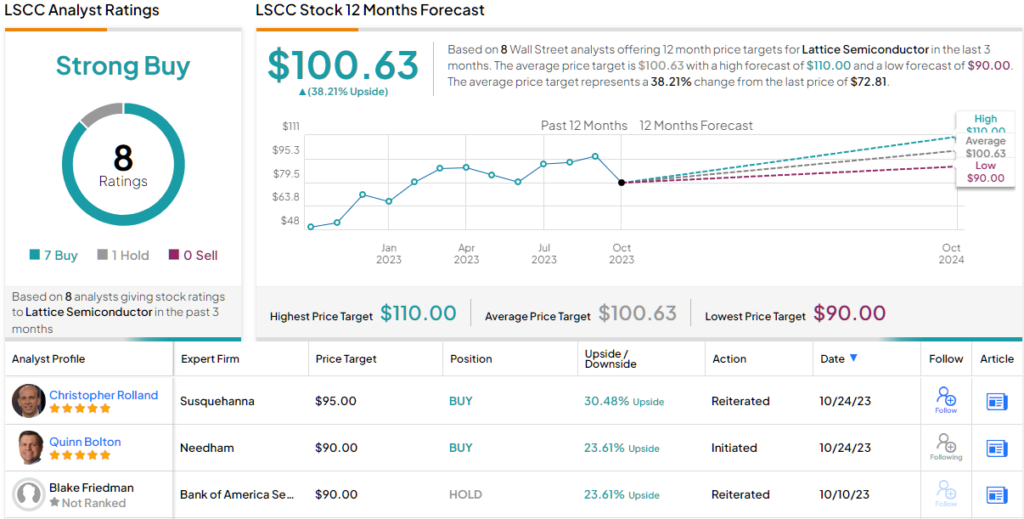

These comments support Bolton’s Buy rating on LSCC, and his $90 price target implies ~24% upside over the next 12 months. (To watch Bolton’s track record, click here)

Overall, the Strong Buy consensus rating on this stock is based on 8 recent analyst reviews, which break down 7 to 1 in favor of the Buys over Holds. LSCC shares are trading for $72.81 and their $100.63 average price target is even more bullish than Bolton would allow, suggesting a one-year upside potential of 38% for Lattice. (See LSCC stock forecast)

SMART Global Holdings (SGH)

Next up is SMART Global Holdings, a small-cap chip maker that works through a set of subsidiary companies. SMART designs and develops lines of high-end semiconductor chips for computing, memory, and LED applications and uses its technical knowledge to create custom-engineered products that are the best in their class.

SMART’s products, which include DRAM, Flash storage, and solid-state memory circuits, are found in a wide range of small electronics, from smartphones and tablets to laptops and desktops, to LED flat-screen displays and lighting systems.

Over the past year, SMART has experienced first a deceleration and then a decline in its quarterly revenues and earnings. The company has responded with a strategic shift toward developing quality revenue and improving gross margins. As part of this shift, the company announced in June that its wholly-owned SMART Modular Technologies subsidiary had entered into a definitive agreement to sell a majority stake, 81%, of SMART Modular Brazil. The transaction, worth approximately $166 million, is expected to close in late 2023 or early 2024.

Losses due to that transaction and the discontinuation of the Brazil business impacted the company’s last quarterly report for Q4 of fiscal 2023. In that report, SMART showed revenues of $316.7 million, down over 12% year-over-year and missing the forecast by over $58 million. SMART’s earnings came in at $0.35 per share by non-GAAP measures, missing expectations by a dime. For the full fiscal year 2023, the company’s revenue came to $1.44 billion, up a modest 3.3% from fiscal 2022.

For Quinn Bolton, however, this stock shows plenty of reasons why investors should by in.

“We believe SGH stands to benefit from multiple secular tailwinds (including AI/ML, data analytics, 5G, enterprise storage and specialty lighting) and a recovery in the memory cycle. We view the Memory Solutions segment as a reliable source of revenue and cash flow, the LED segment as an opportunistic acquisition with levers to enhance profitability and the IPS segment as the long-term growth driver,” Bolton opined.

Looking ahead, Bolton rates SGH as a Buy, and he sets a $22 target price that indicates room for nearly 64% share appreciation heading into next year. (To watch Bolton’s track record, click here)

Overall, the Street’s analysts clearly like this electronic components company. SGH has 4 unanimously positive analyst reviews to support its Strong Buy consensus rating, and its $24.25 average price target implies a robust one-year gain of 80% from the current trading price of $13.44. (See SGH stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.