During the 2024 election campaign, candidate Trump pledged to implement tariffs as punitive and protective measures. Now, as President, he has acted on this promise. Trump announced a 25% tariff on imports from Canada and Mexico, with Canadian energy resources subject to a lower 10% tariff. Additionally, a 10% tariff was imposed on imports from China.

Following negotiations, Mexico and Canada have agreed to enhance border security to address U.S. concerns over illegal immigration and drug trafficking. As a result, the implementation of tariffs on imports from these countries has been delayed by 30 days to allow for further discussions. However, the tariff on Chinese imports has taken effect immediately

If fully implemented, these tariffs could reshape the U.S. steel market – Canada alone supplies about 40% of U.S. steel imports. The most immediate impact? Higher steel prices. Domestic producers will likely raise their prices in response to the increased cost of imported steel, which will ripple through the supply chain and affect consumers.

However, this shift isn’t all bad news for U.S. steelmakers. As manufacturers reduce their reliance on imports, domestic producers stand to benefit from both higher prices and increased demand. This could lead to a boost in U.S. steel company revenues and stock prices as the market adjusts.

Against this backdrop, Wall Street’s analysts are keeping an eye on steel stocks as hot choices for investors. We’ve opened up the TipRanks database to look at two steel stocks that the analysts are tagging as likely gainers in the coming year. These aren’t big upside names, but they offer steady returns with room for growth. Let’s examine what sets them apart.

Steel Dynamics (STLD)

The first stock we’ll look at is the Indiana-based Steel Dynamics. This company, which has a total production capacity of nearly 13 million tons per year, focuses on the production of lower-carbon-emission, quality steel, mainly produced from recycled ferrous scrap – that is, scrap iron – using electric arc furnace (EAF) technology.

Steel Dynamics operates three main operational divisions: steel, metals recycling, and steel fabrication. The first of these, steel, includes a full range of industrial steel products: hot and cold roll, coated sheet steel, structural steel beams, steel rails, specially engineered bar-quality steel, cold finished steel, and specialty steel sections. The metals recycling division processes both ferrous and nonferrous scrap metals from items such as automobiles, machinery, and appliances, as well as manufacturing scraps, and prepares them for sale to end-users capable of reusing the scrapped materials and producing new steel products from them. Steel Dynamics’ steel fabrication division handles the production of structural steel joist and deck building systems for consumer markets.

Steel is a huge business; it’s found in everything from our skyscrapers to our refrigerators, our cars, and our furniture. You can’t get through a day without using something made out of steel.

Despite that basic fact, Steel Dynamics has seen both revenues and earnings trend downward in recent quarters. For 4Q24, Steel Dynamics reported $3.87 billion in revenues, a figure that was down 8.5% year-over-year and missed the forecast by $90 million. Earnings, reported as a GAAP EPS of $1.36, while also down YoY, were 8 cents per share better than expected.

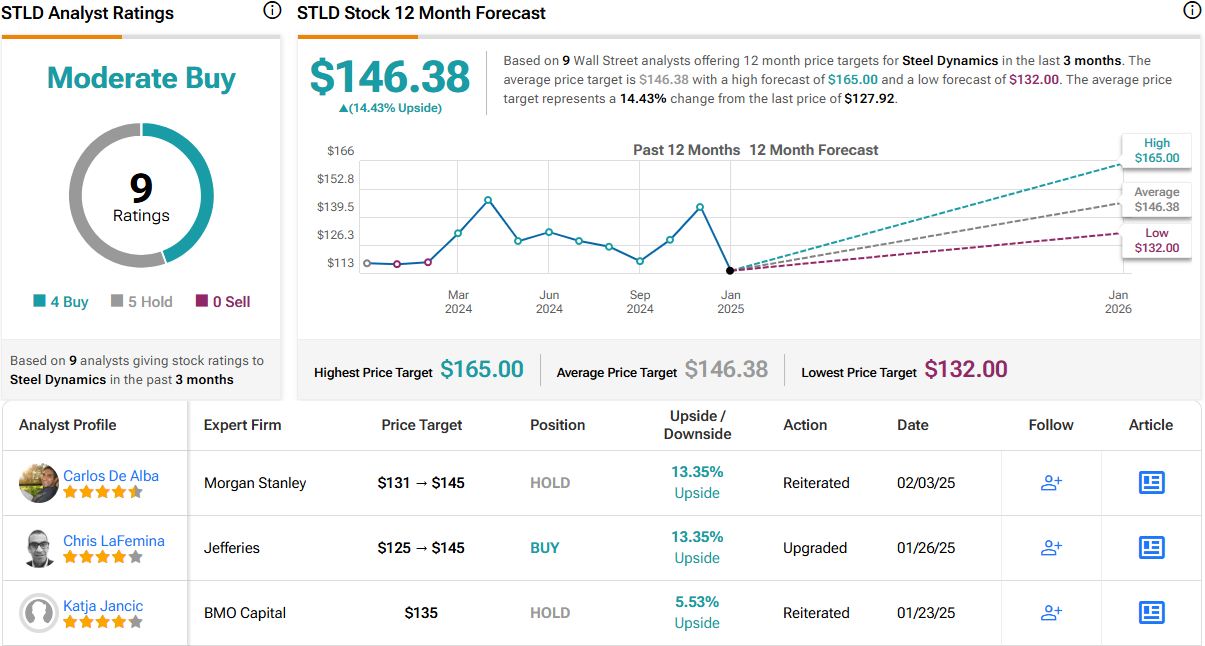

This stock has caught the attention of Jefferies analyst Christopher LaFemina, who is focused on the near- to mid-term future for Steel Dynamics and sees an opportunity at play. He writes of the company and its prospects, “Our base case is for steel prices to rise in 2H25 and into 2026. While at a full run-rate the aluminum investment will partially dilute STLD’s leverage to steel prices, we see less headline M&A risk for this company relative to some other major producers in our coverage. As such, these shares may be the cleanest option for investors who want leverage to US steel market fundamentals and the potential tailwinds under a Trump administration.”

In summary, LaFemina puts a Buy rating on the shares, with a $145 price target that implies a 12-month gain of 13%. (To watch LaFemina’s track record, click here)

The 9 recent analyst reviews on STLD break down to 4 Buys and 5 Holds, for a Moderate Buy consensus rating. The stock is currently trading for $127.92, and its $146.38 average price target suggests that the stock will appreciate by 14.5% in the year ahead. (See STLD stock forecast)

Nucor (NUE)

The second stock we’ll look at is Nucor, which, with its market cap of $30 billion, is the largest of the US steel makers – and one of the largest in the world. The company, which is based in Charlotte, North Carolina, is also the largest scrap recycler operating in the North American market. Nucor was founded in 1955, and today produces a full range of steel and steel products. These include rebars, beams, plates, and sheets used in construction and industry, as well as hot and cold finish steel, steel decking, fasteners, gratings, joists, metal building systems and overhead doors, pilings, steel pipes and tubes, and even steel wire products.

In addition to all of that, Nucor is a major player in the scrap recycling and brokerage business, turning metal scrap into usable steel products and selling the reused metals to industrial customers. Nucor is a major provider of new and recycled steel products to the automotive and construction industries, and even provides specialty steel products to data center customers. The company prides itself on its ability to remain a competent and efficient manufacturer, and to generate consistent free cash flows despite the highly cyclical nature of the steel industry. This can be seen in the company’s cash position; at the end of 2024, Nucor had $4.14 billion in cash and other liquid assets on hand – and its revolving credit facility, worth $1.75 billion, was undrawn.

Nucor declared a 55-cent common share dividend payment on December 11, scheduled to be sent to shareholders on February 11. This marks the company’s 207th consecutive quarterly cash dividend – Nucor has not missed a quarterly payment since it started paying dividends in 1973. While the dividend is rock-solid reliable, the yield is modest – the $2.20 annualized rate gives a forward yield of 1.7%.

Looking at the company’s overall results, we find that Nucor had $7.08 billion in revenue during 4Q24. This was down 8.2% year-over-year, but it beat the forecast by $350 million. The company’s EPS came to $1.22 in the quarter, 59 cents per share better than had been anticipated. For the full year 2024, Nucor reported $30.73 billion in revenues.

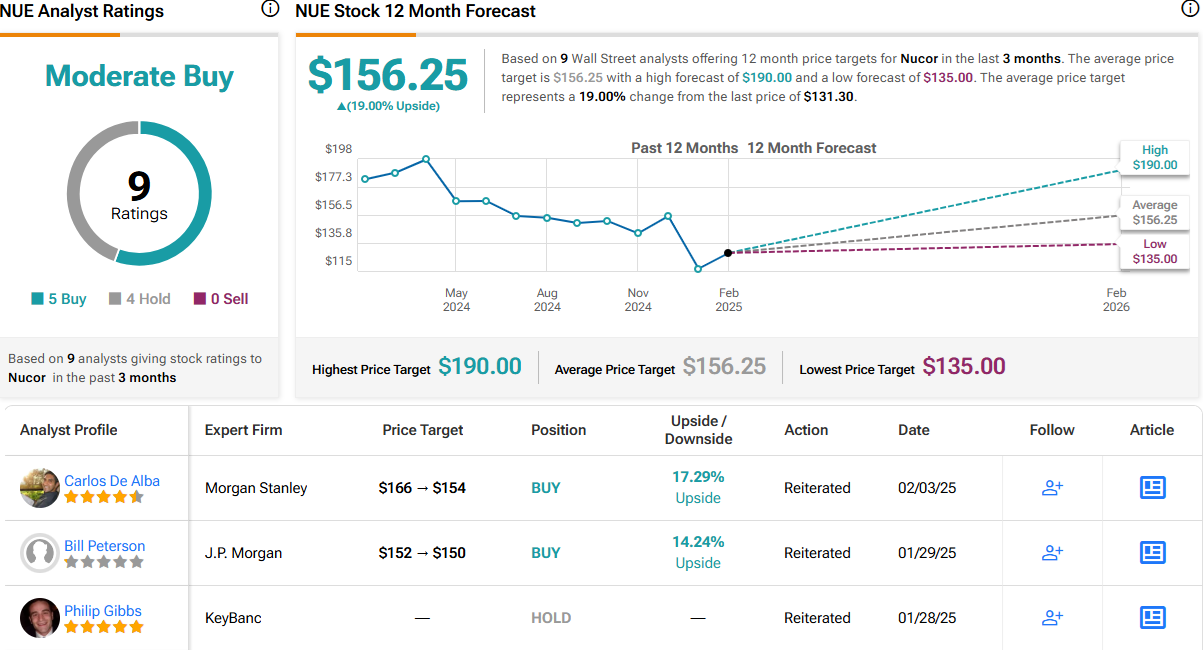

For Lawson Winder, from Bank of America, Nucor presents a sound buying opportunity. He believes that the company’s forecast of an improving steel industry will bear fruit, and says of Nucor’s prospects in the coming year, “Per NUE, market conditions are starting to improve and should gain momentum as the year progresses. In our view, though spot hot-rolled-coil (HRC) pricing remains subdued, we still see potential for a rally in H1’25. NUE should benefit from the rebound in HRC and hold up better in a correction given attractive exposure (relative to peers) to longs/diverse downstream products. Capital returns could also continue to remain robust despite elevated capex in the near-term. NUE has completed two-thirds of its $10 billion (bn) investment plan and is yet to realize the earnings potential from recently completed projects.”

Winder rates NUE shares as a Buy, and his $160 price target indicates a one-year upside potential of 22%. (To watch Winder’s track record, click here)

Like Steel Dynamics above, Nucor has 9 recent analyst reviews; in Nucor’s case, these split into 5 Buys and 4 Holds for a Moderate Buy consensus rating. The shares have a selling price of $131.30 and an average target price of $156.25; together, these prices imply a gain of 19% on the 12-month horizon. (See NUE stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.