Sometimes, finding the right stock can be a chore, and sometimes, a pleasure. But whether it’s a breeze or a slog, some things remain constant. The right stock will always bring a benefit to your portfolio – and high-yield dividend stocks, when carefully chosen, will do just that.

Invest with Confidence:

- Follow TipRanks' Top Wall Street Analysts to uncover their success rate and average return.

- Join thousands of data-driven investors – Build your Smart Portfolio for personalized insights.

Wall Street analysts have been doing the research for you, picking out stocks that are meeting those requirements. And the results are interesting – the analysts have tagged two stocks under $10 with strong dividends, at least 9% to be exact. These aren’t big names that dominate the stock market, but nevertheless, they are companies that deserve a second look.

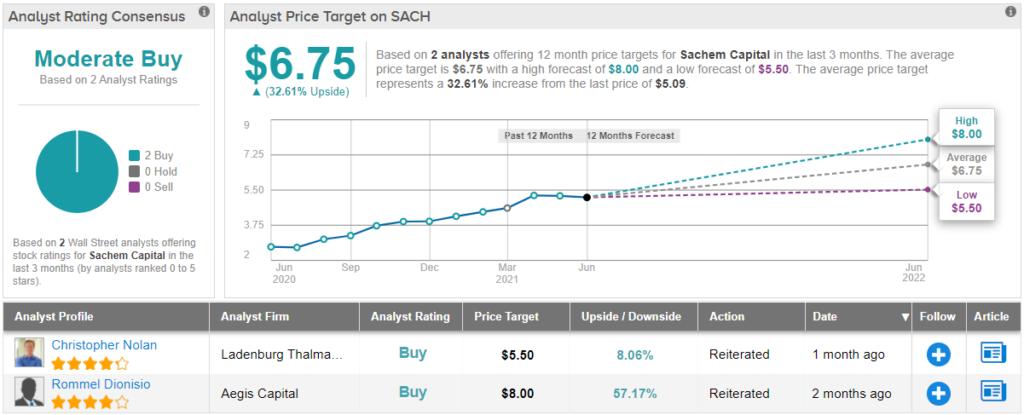

Sachem Capital (SACH)

The first dividend stock we’re looking at here, Sachem Capital, is a real estate investment trust. These financial companies acquire real estate and/or mortgage loans and mortgage-backed securities; Sachem is no exception, and focuses on its portfolio of first mortgage loans. The company offers short-term mortgage loans to real estate investors – rather than owner-occupants – for the purpose of funding acquisition, renovation, development, and improvement of properties.

At the end of the first quarter, Sachem’s portfolio had assets totaling $228.4 million, up a modest $1.7 million from the previous quarter. The company’s revenue came in at $5.7 million for the quarter, a gain of 32.5% year-over-year. EPS, at 10 cents, was flat from the year-ago quarter – and from 4Q20.

Management’s confidence in the quarter was clear from the company’s dividend declaration. Sachem announce at the beginning of April a 12 cent per common share dividend payment. This annualizes to 48 cents per common share – and gives the stock a dividend yield of 9.4%. Among S&P-listed stocks, the average dividend yield is only ~2%, so Sachem’s compares favorably.

Aegis analyst Rommel Dionisio takes a bullish stance on Sachem, noting: “[The] company has increased the scope of its lending operations in recent quarters as the overall economy rebounded from the earlier phases of the COVID pandemic…. Given a robust residential real estate in the company’s core region of Connecticut, the company saw a more rapid pace of loan payoffs during the quarter… We also note that the competitive landscape remains favorable, as many banks and traditional lenders have not significantly eased up on lending requirements.”

With those comments in mind, Dionisio rates SACH a Buy, and his $8 price target implies an upside of 57% for the year ahead. (To watch Dionisio’s track record, click here)

Both of the recent reviews on SACH stock are Buys, making the Moderate Buy consensus rating unanimous. The shares are priced at $5.15 and have an average price target of $6.75, for a upside potential of ~33%. (See SACH stock analysis at TipRanks)

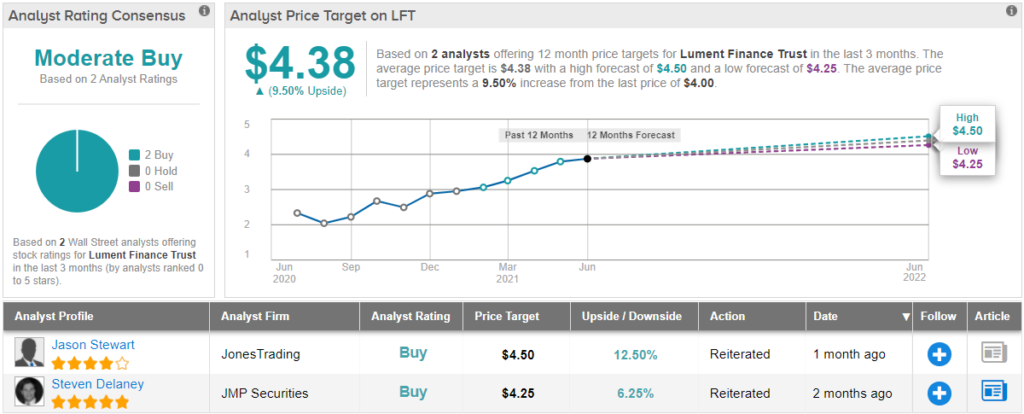

Lument Finance Trust (LFT)

For the next stock, we’ll turn to Lument. This company lives in the micro-cap category, with a market cap of just $96.5 million. Lument carries a portfolio of commercial real estate debt investments, mainly transitional floating rate commercial mortgage loans. This portfolio emphasizes mid-market multi-family properties – apartment complexes.

For the first quarter, ending March 31, Lument reported 11 cents per share income, based on a total net income of $2.8 million. The EPS was up 83% compared to the 6-cent EPS reported one year ago. The company’s distributable earnings for the quarter were listed as $2.8 million, and supported a 9 cent dividend payment.

The dividend was down 4 cents per common share from the prior quarter, 4Q20, mainly in keeping with the company’s policy of setting the payment to fit income. Even after the cut, the common share dividend still annualizes to 36 cents – and gives a strong yield of 9.35%. With the Fed holding rates at historic lows, dividends in the broader stock markets yielding an average of just about 2%, and the 10-year Treasury bond yielding even below that, the attraction of Lument’s yield is clear.

Covering the stock for JonesTrading, analyst Jason Stewart rates LFT a Buy along with a $4.50 price target. This figure implies a 12.5% upside on the one-year time horizon. Based on the current dividend yield and the expected price appreciation, the stock has ~22% potential total return profile. (To watch Stewart’s track record, click here)

“We see two clear catalysts for LFT over the next two quarters: deployment of capital and refinancing of the existing CLOs. First, with fresh capital from the recent preferred stock offering, we expect LFT to leverage the ORIX USA origination platform to grow the balance sheet. Second, the CRE CLO market is having a banner 2020 and financing spreads are compressing which will allow LFT to re-lever the overall equity base,” Stewart noted.

The analyst also points out the company’s underlying soundness: “The loan portfolio was 100% current as of March 31, 2021, with no forbearances granted or defaults. 88% of the portfolio was invested in multifamily and the company maintains no exposure to hospitality assets.”

Judging from the consensus breakdown, it has been relatively quiet when it comes to other analyst activity. Over the last three months, only 2 analysts have reviewed LFT. Both of which, however, were bullish, making the consensus a Moderate Buy. The shares are selling for $4.00, and the average price target of $4.38 indicates a 9.5% upside from that level. (See LFT stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.