One of President Trump’s key campaign promises was to cut government waste, a promise that he’s fulfilling with the formation of DOGE, the Department of Government Efficiency.

Headed by Elon Musk, DOGE is taking Trump’s bull-in-the-China-shop approach to eliminating bloat and waste in the Federal government. The ‘blunt instrument’ approach to cutting back an overly swollen government bureaucracy is controversial and is already seeing some court challenges – but it is also politically popular with Trump’s voter base.

One thing is certain: the current situation is generating a storm of uncertainty. This can be seen in the stock performance of government contractor firms, many of which have seen steep declines since Trump’s November election win.

But there are some bright spots in the contractor sector. Covering these stocks for Cantor, analyst Colin Canfield writes, “GovTech equities have significantly underperformed the market over the last 3M, thanks primarily to the volatility of sentiment around Government budget growth. We think Defense/Intel names are best positioned to outperform, especially as global security threats accelerate ahead of fiscal threats.”

Adding context to the outlook on the defense/intel names, Canfield goes on to say, “Russia’s invasion of Ukraine and China’s stated intent to take Taiwan by force suggest a new era in multi-polar, global conflict, although we believe the realities of international force structures should deter significant escalation. Over time, we expect deficits to take a greater toll on Government names as Congress looks to reduce spending, but we expect Government savings outcomes to materialize as flattened growth vs. outright cuts.”

Against this backdrop, we turned to the TipRanks database to pinpoint two beaten-down GovTech stocks that may be approaching a bottom. Both have struggled amid the broader sector downturn, but Canfield sees potential in their positioning. He rates both as ‘Buys,’ believing they have what it takes to rebound. Let’s take a closer look.

CACI International (CACI)

First on our list is CACI International, an information technology firm based out of Reston, Virginia, just outside of the Capital Beltway. Reston is known as a hub for Federal government contractor companies, and CACI fits squarely in that niche. The company has built a wide-ranging expertise in both technology and national security, and puts that to work for a multitude of government agencies and entities. The company is particularly well-known for providing services to the national security apparatus, including the Departments of Defense and Homeland Security, and the Intelligence Community.

CACI’s services include enterprise IT, digital solutions, cyber tech and security, military mission and engineering support – and even mission operations and data management for the government’s space programs. The company’s capabilities include HR and financial management, investigative and watchdog services, and even such apparently mundane logistical tasks as supply chain management. AI has made waves in recent years, and CACI has been a leader in applying AI and deep learning technology to defense applications to produce cost-effective ways of meeting rapidly evolving needs. CACI has been in the business of government contracting since 1962 and today boasts a market cap of $8.4 billion.

Shares in CACI hit a peak just after the November election, but have since fallen by 34%.

We should note, however, that CACI’s earnings have remained positive even as the share price fell and that the company’s revenues are trending upwards.

Looking at CACI’s last earnings report, released last month and covering fiscal 2Q25, we see that the company’s revenue total was up 14% year-over-year, reaching $2.1 billion and beating the forecast by $60 million. At the bottom line, the company’s non-GAAP EPS figure came in at $5.95, or 75 cents per share ahead of expectations. The company reported a solid work backlog, of $31.8 billion as of December 31, 2024, up 18% year-over-year.

In his coverage of this company for Cantor, analyst Canfield points out that periods of low share price have made good opportunities for investors to buy into CACI. Explaining this dynamic, Canfield writes, “Leading AI, Cyber, and RF capabilities should position CACI well amidst any potential budget cuts although we think CACI’s material NatSec exposure (90%+) insulates it well from slowness. Margin expansion potential may be muted near term by scaling expertise programs, but we think CACI continues to benefit from significant capital deployment opportunities over time.

“Near term, that likely means increased shareholder returns, especially if shares continue to lag, while over time we expect continued bolt-on M&A,” Canfield went on to add. “We note that, like other Government Services names, we may have to wait for O&M outlays to reaccelerate before we get meaningful outperformance, but short-term price dislocations have historically been great entry points as CACI capital deployment and cash-performance lift valuation.”

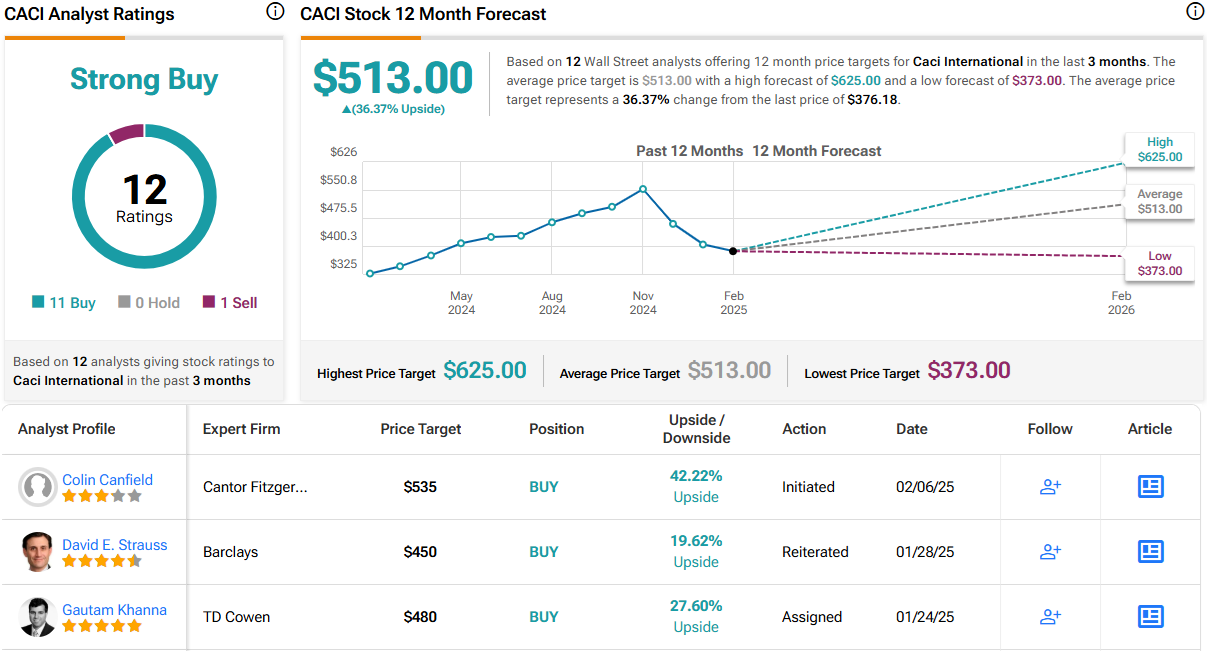

Quantifying this stance, Canfield rates CACI shares as Overweight (i.e. Buy) with a $535 price target that points toward a one-year gain of 42%. (To watch Canfield’s track record, click here)

Overall, CACI gets a Strong Buy consensus rating from the Street, based on 12 recent analyst reviews that break down to a lopsided split of 11 Buys and 1 Sell. The stock has a current trading price of $376.18, and its average target price, now at $513, points toward a share appreciation of 36% on the one-year horizon. (See CACI stock forecast)

Booz Allen Hamilton (BAH)

The second stock we’ll look at here is Booz Allen Hamilton, another of the ‘Beltway Bandit’ firms that offer consulting, management, and information technology services to the US government. Booz Allen is based in McLean, Virginia—next door to Reston, where CACI has its headquarters—and it has been in the business of outside consulting, for both the public and private sectors, since 1914.

Booz Allen describes its particular expertise as problem-solving by putting the right people to work in the right places. With more than a century of experience behind it, Booz Allen has had to change with the evolving landscape of the consulting business and today boasts capabilities in such fields as cybersecurity, data science and analytics, digital solutions, and engineering. The company employs more than 35,000 people and is the largest provider of AI services to the federal government. Like CACI above, Booz Allen is a major service provider to the Defense Department; it also serves health, finance, transportation, space, and energy agencies.

Turning to the company’s financial results, we find that BAH released its fiscal 3Q25 report on January 31 and showed solid year-over-year gains at both the top and bottom lines. The company’s revenues of $2.92 billion were up 13% year-over-year and were $50 million better than anticipated. Earnings, reported as a non-GAAP EPS of $1.55, were 10% better than the same period in the prior year—and were 3 cents over the forecasts.

Of note to investors, Booz Allen pays out a modest but highly reliable common share dividend. In its last declaration, the company raised the payment by nearly 8% to 55 cents per share. At this rate, the dividend amounts to $2.20 per common share annually and gives a forward yield of 1.6%. The new dividend is scheduled for payment this coming March 4. While the dividend yield is modest, Booz Allen has been making the quarterly payments consistently for the past 12 years and has steadily increased the dividend payment over that time.

Booz Allen’s stock hit a peak in late October of last year but since then has fallen by 31%. Yet, once again, we’re looking at a stock that, in the Cantor view, has strong potential as a ‘bargain’ buy. Analyst Canfield explains that the company is likely to outlast current headwinds and that the long-term prospects for BAH are sound: “While sentiment headwinds related to government deficit initiatives and BAH cost+ exposure have driven significant price dislocation, we think recent underperformance is overdone. We expect BAH’s cyber, AI and IT businesses continue to be growth leaders among scaled Government Technology businesses over the next 3Y (>10% organic). Civil cuts may weigh, but any reductions to spend likely serve as growth moderators, pushing IT and AI adoption needs to the right rather than erasing them. While near-term capital deployment is likely focused on shareholder returns, we also expect BAH to become a more meaningful M&A integrator over time, leveraging seed-funding opportunities around spectrum, quantum and Space.”

These comments back up Canfield’s Overweight (i.e. Buy) rating on the stock, and his $160 price target suggests a one-year upside potential of 25%.

Booz Allen’s stock has a Moderate Buy consensus rating from the Street, based on 11 reviews that include 6 to Buy, 4 to Hold, and 1 to Sell. The shares are priced at $127.94 and have an average price target of $156, implying an upside for the next 12 months of 22%. (See BAH stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.