AppLovin (NASDAQ:APP) is among my most successful investments, but I am still bullish. The company’s share price growth over the past 12 months tops anything we’ve seen from the so-called ‘Magnificent Seven.’ And after four successive earnings beats, valuation metrics support my bullishness. AppLovin currently trading at 16x forward earnings, and analysts expect the company’s earnings to grow by 20% annually over the next three to five years. It’s a Strong Buy, in my view, and according to analysts.

AppLovin Stock Is Powered by AI

On May 8, AppLovin announced its financial results for the first quarter, and it was a fourth straight earnings beat. Central to this earnings beat was artificial intelligence (AI). AppLovin started rolling out its new AI engine in 2023, but management said it would be hard to predict how much upside the tech would provide. Called Axon 2.0, the AI technology recently turned one year old, and it’s really starting to contribute to revenue growth.

AppLovin’s AppDiscovery platform utilizes Axon 2.0’s power to improve user acquisition (UA) for app developers. By understanding user behavior and preferences, the AI engine helps AppDiscovery deliver more targeted advertising campaigns with greater accuracy and efficiency. This translates to better campaign performance for developers and a more relevant advertising experience for users.

AppLovin CEO Adam Foroughi said, “Advertisers have increased their spend on our platform as a result of the improved performance from Axon.”

Axon 2.0 is also being rolled out beyond the mobile gaming market — mobile gaming is the company’s bread and butter. “We also work with non-gaming apps, and we’ve seen success once we rolled out Axon 2.0 across a variety of non-gaming companies growing on our platform too,” Foroughi said in the Q1 earnings call. The CEO also highlighted that the non-gaming verticle was seeing stronger growth than the mobile gaming space, partially because it’s starting from a lower base.

Moreover, the company has suggested that Axon 2.0 hasn’t been fully integrated yet and that more growth is expected. Coupled with returning growth in the advertising segment as a whole, the future looks bright for AppLovin.

AppLovin’s Growth Trajectory Is Changing

Four earnings beats in a row is obviously great, but it’s really exciting because AppLovin’s growth trajectory hasn’t always been that strong. If we look back at 2022 and 2023, we can see that revenue wasn’t always moving in the right direction. In fact, at the beginning of 2022, Q1 revenue fell 21.2% sequentially.

I find this improving growth trajectory really interesting and important because AppLovin’s management hasn’t been putting a lot of emphasis on its selling processes. Foroughi says he’s not good at sales but claims the company aims to deliver a great product that will create a ripple effect throughout the industry, with happy clients informing their peers about AppLovin’s stellar performance. With Axon 2.0, it does seem like this ripple effect is thoroughly underway.

AppLovin Stock Is Still Cheap

AppLovin is currently trading at 16x non-GAAP forward earnings for 2024. That’s actually a 34.5% discount versus the information technology sector average and represents a significant discount versus big tech peers. From a GAAP perspective, AppLovin is trading at 30.4x forward earnings, which is a little less attractive but still appealing, given the company’s growth trajectory.

Looking further forward, analysts expect earnings per share to grow at 20% annually over the medium term — the next three to five years. In turn, this leads to a forward price-to-earnings-to-growth (PEG) ratio of 0.8x. That’s one of the most attractive PEG ratios I’ve come across in this market. Using the GAAP valuation, the PEG ratio is around 1.33x. That’s still not bad, given market conditions and the long-term potential of AI.

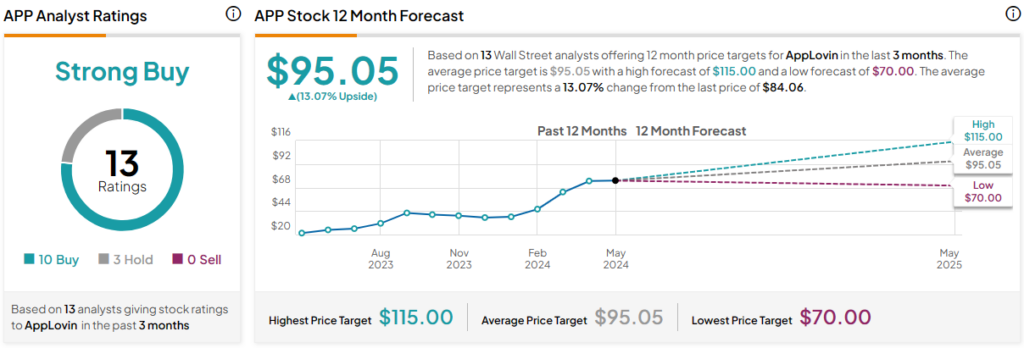

APP Stock Is a Buy, According to Analysts

AppLovin stock is rated a Strong Buy, according to analysts offering 12-month price targets in the last three months. There are currently 10 Buys and three Hold ratings. The average AppLovin stock price target is $95.05, implying 13.1% upside potential.

The Bottom Line on AppLovin Stock

AppLovin stock has rewarded shareholders with a 267% increase over the past 12 months. The stock has gone from strength to strength on the back of its use of AI and a recovering advertising market. Further, the company still looks cheap on a non-GAAP basis and is one of the few companies in the space to trade with a PEG ratio under 1.0x. I’m expecting more upside from AppLovin stock, just as analysts do.