Apple stock (AAPL) continues to trade near all-time highs, despite the company’s stagnating financial growth. Although Fiscal 2024 marks another year of marginal revenue gains and declining profits, investors remain enthusiastic about Apple’s prospects. Optimism around key segments like iPhone and Services, coupled with enormous stock buybacks, keep Wall Street confident in the face of Apple’s seemingly underwhelming top and bottom line numbers. Considering that this setup is likely to persist moving forward, I remain bullish on Apple.

Don't Miss Our Christmas Offers:

- Discover the latest stocks recommended by top Wall Street analysts, all in one place with Analyst Top Stocks

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

Apple’s Stagnated Financials: The Challenges of Mature Dominance

So, as I just mentioned, the paradox between Apple’s underlying performance and its rather hefty share price levels is that its financials have seen little growth over the past year, as once again confirmed in the company’s latest Q4 Fiscal 2024 results. Segment sales for the year highlight this trend: product revenues for the year declined from $298.1 billion to $294.9 billion, while net income declined from roughly $97.0 billion to $93.7 billion.

Specifically, while iPhone revenues reached $46.2 billion, a 6% increase year-over-year, and iPad revenues grew 8% to $7.0 billion, other segments like Wearables (down 3% YoY to $9 billion) and Mac (up just 2% YoY to $7.7 billion) experienced either declines or negligible growth, which I see as reflecting the maturity of Apple’s core product lines. In fact, one could argue that these results point to a broader reality—the company’s dominance and maturity in the tech space suggest it should continue to struggle to deliver meaningful sales growth, especially for hardware.

Despite these lackluster numbers, the stock continues to command a lofty valuation. Specifically, Apple is trading at over 30 times the consensus Fiscal 2025 EPS estimate, a multiple I would say is more suitable to rapidly growing companies than a mature tech giant. As you know, such lofty multiples typically require strong underlying growth, yet Apple’s figures suggest otherwise.

Why Wall Street Ignores Apple’s Stagnation

So why does the market’s enthusiasm for Apple remain cheerful? Well, one core catalyst seems to be the remarkable growth seen in the Services segment. Services revenue reached an all-time high of $25 billion in Fiscal Q4, marking a 12% year-over-year increase. I think the importance of Services growth for Apple cannot be understated, and the market clearly acknowledges this. Given that this high-margin segment also gradually accounts for a larger chunk of Apple’s revenue mix over time, it bodes well for Apple’s future profitability.

Management highlighted that increased customer engagement, new subscriptions, and ongoing content investments were some of the most prominent factors driving Services revenues higher in the most recent quarter. In my view, the segment’s sustained, double-digit growth rate adds a thick layer of optimism that should keep powering investor confidence in AAPL stock.

Apple’s Buybacks Continue to Impress

In addition to the growth in Services, Apple’s ongoing buyback program is another notable factor that is likely to sustain the stock’s bullish sentiment. Apple repurchased nearly $95 billion worth of its own shares in Fiscal 2024, up from $77.6 billion in the previous year, marking another year of record buybacks. While Apple’s enormous market cap of $3.39 trillion might make even nearly $95 billion seem fairly modest, the effect is still impactful, as it translates to a buyback yield of nearly 3%.

Combined with the stock’s cult-like investor base, which tends to hold on for the long term, it seems that Apple’s massive buybacks create a constant demand for shares that outweighs any pessimism regarding revenue stagnation. This is evident in the stock’s resilience, as even with Warren Buffett‘s Berkshire Hathaway (BRK.A) (BRK.B) selling nearly half of its stake—about 390 million shares—last quarter, the share price held firm. I view this as a clear testament to the strength of Apple stock, given that Berkshire’s sales should have led to quite significant downward pressure.

Is AAPL Stock a Buy?

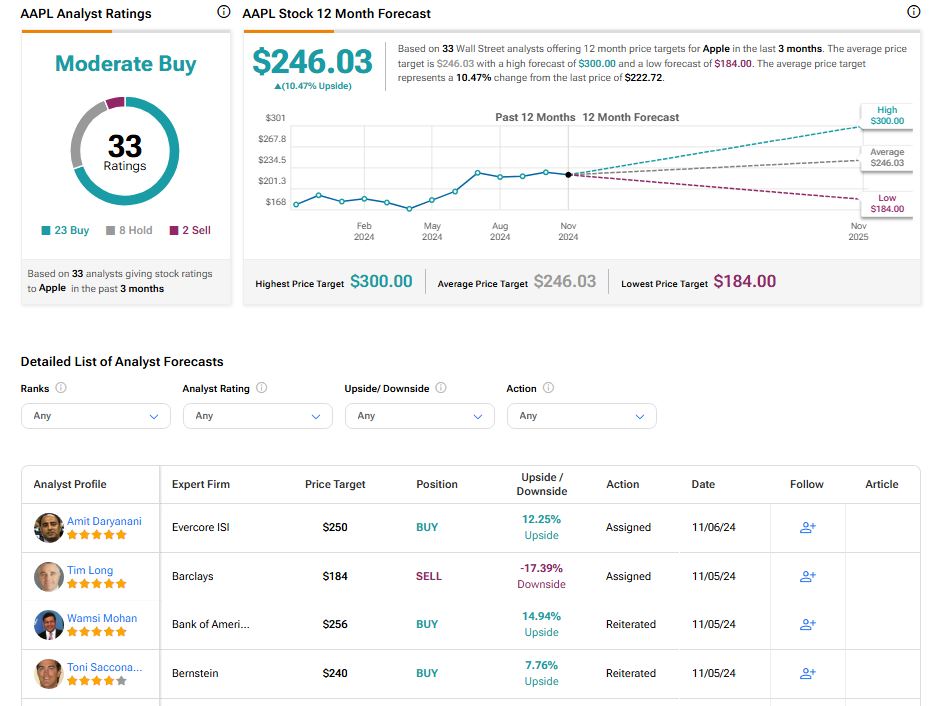

Despite Apple stock’s high valuation, Wall Street maintains a relatively bullish outlook. Currently, AAPL holds a Moderate Buy consensus rating, with analysts issuing 23 Buy ratings, eight Holds, and two Sells over the past three months. At $246.03, the average AAPL price target indicates 10.47% upside potential.

If you’re wondering which analyst you should follow if you want to trade AAPL stock, consider Michael Walkley, who represents Canaccord Genuity. He is the most accurate analyst covering the stock (on a one-year timeframe). He boasts an average return of 35.53% per rating and a 92% success rate.

Conclusion

Overall, despite limited revenue growth and declining profits, it seems that the optimism around Apple’s stock remains robust primarily due to strong growth in the high-margin Services segment and continued buybacks. Specifically, Services revenue keeps hitting new record highs by the quarter, sustaining double-digit growth, which signals exciting long-term profitability potential.

In the meantime, Apple’s aggressive buybacks support the share price and keep translating to a decent buyback yield, even at the stock’s lofty valuation. Given that this setup is likely to persist, Apple’s investment case remains intact even as the tech giant posts somewhat lackluster growth metrics in the short term. Therefore, I remain bullish on Apple.