Apple Inc. sold $14 billion of bonds as low borrowing costs prompted the iPhone maker to come to the debt market for a third time since May, Bloomberg reported.

Invest with Confidence:

- Follow TipRanks' Top Wall Street Analysts to uncover their success rate and average return.

- Join thousands of data-driven investors – Build your Smart Portfolio for personalized insights.

According to the preliminary prospectus of the offering disclosed in an SEC filling, Apple (AAPL) sought to issue bonds in six tranches, including notes due 2026 and notes due 2061. The 40-year security will yield 95 basis points above Treasuries, after initially discussing between 115 and 120 basis points, according to the Bloomberg report.

“We intend to use such net proceeds for general corporate purposes, including repurchases of our common stock and payment of dividends under our program to return capital to shareholders, funding for working capital, capital expenditures, acquisitions and repayment of debt,” Apple said in the preliminary share prospectus.

Apple can borrow at a rate of 1.86% for about nine years, according to Bloomberg Barclays index data. That’s down from 1.94% when Apple was last in the market in August. The move comes as the company is looking to trim its net cash position, by returning more cash to shareholders. According to Bloomberg Intelligence, the tech giant may need to increase its annual shareholder returns to over $100 billion to attain its net-cash neutral target over the coming years.

Last week, Apple reported its largest revenues in a single quarter, exceeding the $100 billion milestone for the first time. However, looking ahead to the March quarter, the company’s CFO Luca Maestri said that the services business will face a “tougher year-over-year comparison,” following increased demand for digital services amid the pandemic-led lockdowns last year. Maestri added that sales growth in airpods and in the wearables, home, and accessories category is expected to decelerate sequentially in 2Q.

Following the strong 1Q results, Wedbush analyst Daniel Ives maintained a Buy rating and a price target of $175 (30% upside potential) on the stock.

“We essentially view this quarter as the kickstart to the 5G supercycle which so far, we are seeing order activity continue to track significantly ahead of expectations as well as its predecessor iPhone 11 signaling a green light into FY21,” Ives wrote in a note to investors. “Investors are also laser focused on Services revenue which once again came in ahead of expectation.” (See Apple stock analysis on TipRanks)

Currently, the rest of the Street has a cautiously optimistic outlook on the stock. The Moderate Buy consensus rating is based on 20 Buys, 6 Holds and 2 Sells. Meanwhile, the average analyst price target of $149.19 indicates 11% upside potential to current levels. That’s after shares yielded 68% over the past year.

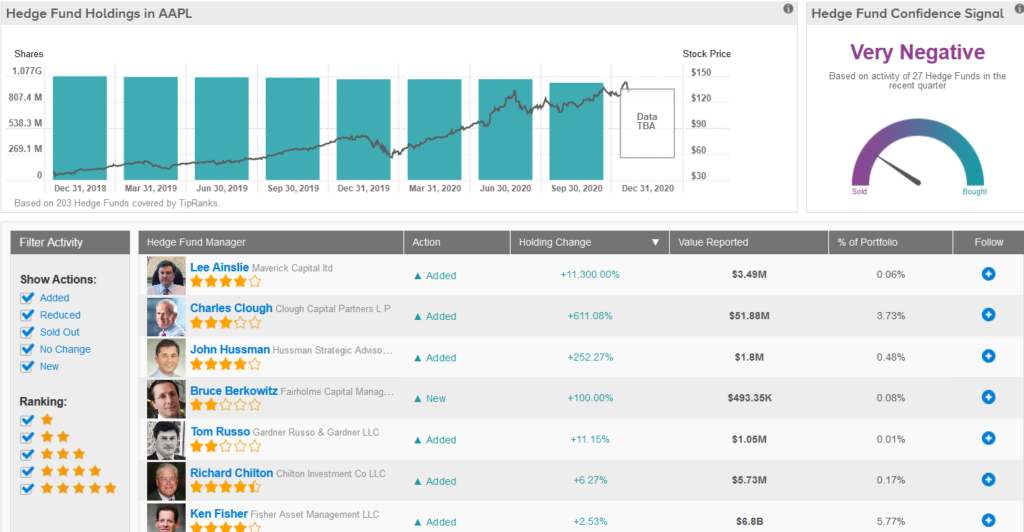

Meanwhile, TipRank’s hedge fund trading activity tool shows that confidence in AAPL is currently very negative as 27 hedge funds trimmed their cumulative holdings in the stock by 38 million shares in the last quarter.

Related News:

Virgin Galactic Shares Pop 14% Pre-Market After Flight Test Program Update

XPeng’s EV Deliveries Pop 470% In January; Shares Surge 6% Pre-Market

Facebook’s Strong Advertising Revenues Fuel Blowout Quarter