You can’t talk about tech today without bringing up the Magnificent 7 or AI. The Mag 7 are the top tech giants, ruling their fields with massive market caps. AI is the shiny new thing, the technology development driving tech to new frontiers. Together, the two are defining just where we’re going to go – and are providing investors with enormous opportunities to cash in on the trip.

Apple (NASDAQ:AAPL) and Alphabet (NASDAQ:GOOGL) are two of the biggest names among the Mag 7 tech stocks, and they need little introduction. Multi-trillion-dollar companies, with their hands in multitudes of pots, their recent moves have brought a potent combo of AI, edge computing, and cloud services into the spotlight.

Analyst Barton Crockett, from Rosenblatt Securities, has taken the measure of both tech giants – and come down with a clear opinion on which of these is the superior Magnificent 7 stock to buy. Let’s give them a closer look, and check out Crockett’s notes as well.

Apple

The first company we’ll look at is Apple, the largest titan in the tech industry, known for its innovative devices that creatively leverage technology.

Recently, Apple made a splash when CEO Tim Cook introduced us to Apple Intelligence, the firm’s name for its ongoing efforts to integrate AI technology into its existing hardware lines. Apple Intelligence will be built into iPhones, iPads, and Macs, providing seamless assistance as users write and express themselves online. The AI will draw on the user’s own content, the stored files and data on the devices, to develop a generative AI that fits the user. And, Apple has not ignored security – the company’s Apple AI is designed to set a new standard for privacy protection in AI technology, while enhancing the user’s ability to create novel written and visual materials.

The Apple Intelligence announcement came at just the right time; Cook introduced it publicly on June 10, just a few weeks after the company’s fiscal 2Q24 earnings release. The two together – the earnings and the AI – allayed investor worries about the company’s business. The worries came from the iPhone and China. The iconic smartphone device has become the main driver of Apple’s revenues, while the China market in recent years became more and more important for Apple. Industry experts had expressed concern that Apple was growing too dependent on that combination – but the fiscal Q2 results and the AI announcement went a long way toward putting those fears to rest.

Covering Apple for Rosenblatt, Crockett takes particular note of the company’s strong privacy protections in its AI as an attractive feature.

“Strong privacy is by far the top feature consumers want in AI, based on our recent US survey, arguing for market share lift potential for Apple in AI, based on the unique privacy focus of Apple Intelligence, to date unmatched by Android. Apple’s approach also appears to immunize it from cost pressures at hyperscalers, while enabling Apple to benefit from their investments. We see this tipping AI risk/reward in favor of Apple,” Crockett opined.

Based on this stance, Crockett rates AAPL shares as a Buy, and raises his price target from $196 to $260. The raised target implies a one-year upside of nearly 13%. (To watch Crockett’s track record, click here)

Overall, Apple gets a Moderate Buy consensus rating from the Street, based on 35 recent reviews that break down to 25 Buys, 9 Holds, and 1 Sell. However, the analysts expect shares to remain range-bound for the foreseeable future as indicated by the $230.25 average price target. (See AAPL stock forecast)

Alphabet

Next up is Alphabet, the parent company of the internet’s leading search engine, Google, and the leading video search, YouTube. Through them, Alphabet is the leading company in the lucrative world of online search and its associated advertising. This is a lucrative business, and it’s pushed Alphabet into the uppermost levels of Wall Street’s giants; the company is the fourth-largest publicly traded firm on the Street, with a market cap of $2.32 trillion.

Alphabet has been making strong use of AI in recent months. In December of last year, the company introduced Gemini, a group of AI products based on multimodal large language models. Gemini has high potential to bring important improvements to most of Google’s various functions, from online search to text writing and translation services. Gemini has the potential to enhance Google’s search, making it more competitive against the challenge from Microsoft’s Bing search engine, which is already making use of OpenAI’s technology. In addition, Gemini is already part of Google’s online translation service, where it uses natural language processing to provide clear text translations across a large number of languages. And finally, Gemini has been billed as a direct competitor to OpenAI, as a chatbot that offers a similar set of functions as ChatGPT.

Gemini has been well-received, and it should not surprise us that Alphabet’s stock has been showing solid gains in recent months.

However, Rosenblatt’s Crockett has toned down his outlook on the stock. The analyst cites several factors, including uncertainties in how AI will shake out as a component of online search functions and in how Google will handle its competition with Bing.

“We lower our Alphabet rating to NEUTRAL, seeing multiple areas of transitional risk that recommend stepping back for a little while to see how the company handles it. Areas of risk include the AI’s impact on search — including the likely at least transitionally negative impact on search ad revenues of layering in AI Overviews. There is also nascent evidence of search share loss to Bing. And the transitioning of search ad revenue to retail media networks seems set to accelerate as other retailers such as Walmart follow Amazon’s lead and push into this arena,” Crockett explained.

The analyst goes on to outline some additional risks for Alphabet, noting: “Also presenting some risk is the aggressive entry of Amazon this year into video advertising (making ads default on Prime Video this year, and launching an aggressive upfront sales effort this May), which could impact ad sales dynamics at YouTube. We also see risk that competitive dynamics push Alphabet into a higher-than-expected capex spending cycle for AI.”

Crockett’s Neutral rating on the stock comes with a $181 price target, suggesting that the stock will face a modest 3.5% decline in the coming year.

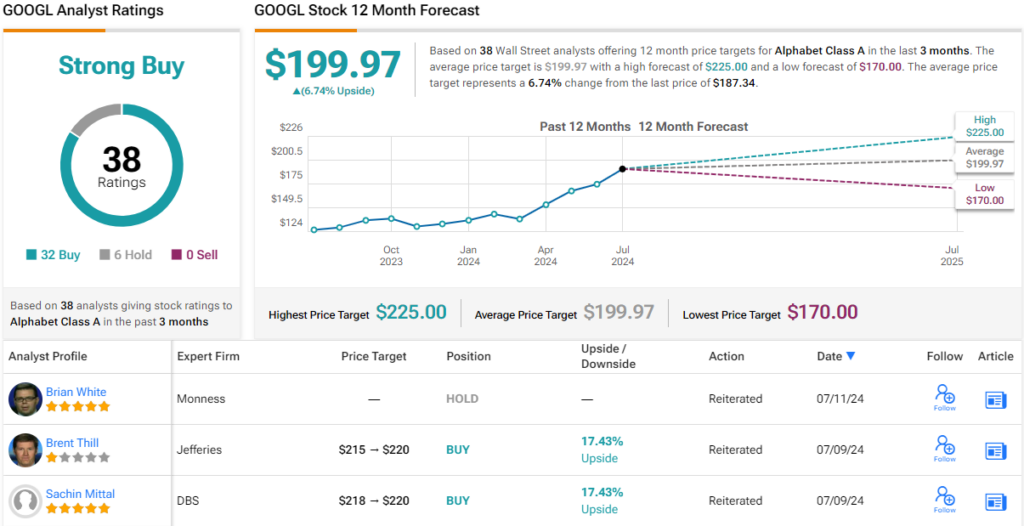

This view is more bearish than the Street’s take; the analyst consensus here is a Strong Buy, derived from 38 reviews that include 32 Buys and 6 Holds. The shares are priced at $187.22, and their $199.97 average price target implies a ~7% one-year increase. (See GOOGL stock forecast)

So with the facts in, it’s clear that Rosenblatt analyst Barton Crockett rates Apple as the superior Magnificent 7 stock right now, a better buy than Alphabet and a solid choice for investors.

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

Questions or Comments about the article? Write to editor@tipranks.com