It was good news for Salesforce (NYSE:CRM), as the customer relationship management company snapped up over 2% in Monday afternoon’s trading session. It was all thanks to a report from Monness, Crespi, Hardt that things were likely to get better for Salesforce in the near term, and that optimism fueled investor response accordingly.

Confident Investing Starts Here:

- Easily unpack a company's performance with TipRanks' new KPI Data for smart investment decisions

- Receive undervalued, market resilient stocks straight to you inbox with TipRanks' Smart Value Newsletter

The word from Monness, Crespi, Hardt—as expressed by analyst Brian White—is that two major revenue vectors for Salesforce may soon tick up: subscription/support sales and professional services revenue. Professional services revenue is projected to gain 3% year-over-year when the earnings numbers come out, jumping to $592.9 million. Not bad by itself, but the real winner will likely be subscription and support sales, which will surge to a hefty $8.058 billion. That’s up 13% year-over-year, and that alone should help Salesforce clear analyst consensus projections of $8.53 billion in revenue for the quarter.

This news couldn’t come soon enough for Salesforce, which is still reeling from a Business Insider report that noted a former vice president’s claim that the firm fired him for basically being a whistleblower. Said former vice president, Karl Wirth, noted that he raised concerns about Salesforce software’s ability to both process and organize customer data in a matter of milliseconds. Court documents assert that said processes took “…several hours.” Calling such claims “…all a lie,” he was subsequently fired. That was exactly what no customer ever wants to hear, and with that in mind, it’s little wonder that Salesforce is fighting back.

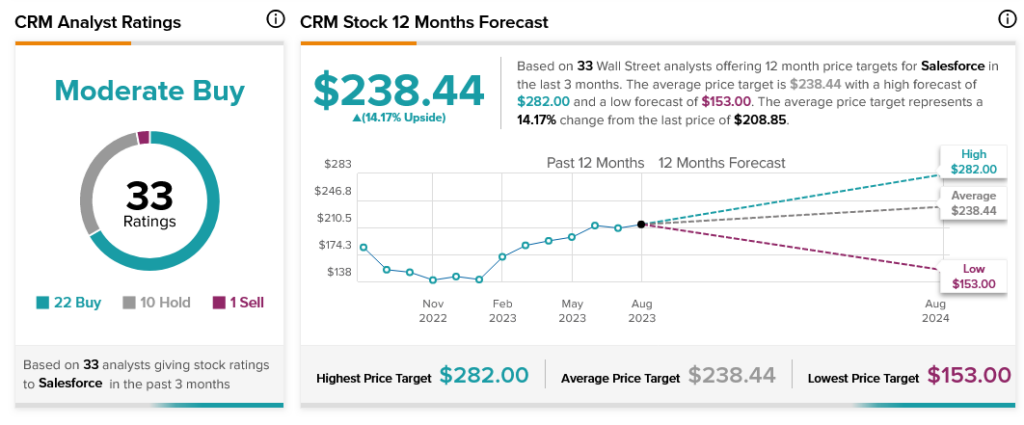

Analysts, however, have considerable faith in Salesforce. With 22 Buy ratings, 10 Holds, and one Sell, Salesforce stock is considered a Moderate Buy by analyst consensus. Further, Salesforce stock offers investors a 14.17% upside potential thanks to its average price target of $238.44.