After two years of strong stock market performance, Wall Street is generally optimistic about 2025. But there is always a contrarian view – and in this case, it’s laid out by hedge manager Bill Smead, who points out that the yield on 10-year Treasury bonds remains high and continues to edge back toward 5% – a move he believes will dampen enthusiasm for stocks.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Smead argues that this reflects the market’s anticipation of persistent inflation and higher interest rates. In the second half of 2024, the Fed reduced interest rates by 1% to counter easing inflationary pressures. Yet, as Smead observes, inflation remains stubbornly high, with annualized rates creeping back toward 3%. While inflation may not surge as it did three years ago, its persistence above the Fed’s 2% target creates pressure to maintain higher interest rates. Historically, elevated rates have weighed on stock performance, and Smead suggests this dynamic could disrupt the ongoing bull market.

So, how should investors respond? While stocks remain resilient for now, there are prudent strategies to hedge against potential downturns. Dividend stocks, for instance, are a classic defensive play and a smart way to diversify a portfolio. Their regular payments provide a reliable income stream, while the best dividend payers offer power yields capable of boosting the overall return.

Against this backdrop, we’ve opened up the TipRanks database to uncover details on two dividend payers with yields of about 11%, which have recently garnered praise from analysts. What’s more, according to the analysts, these stocks also offer double-digit upside potential. Here’s a closer look at these income-generating opportunities.

Franklin BSP Realty Trust (FBRT)

We’ll start with Franklin BSP Realty Trust, a real estate investment trust, or REIT. These companies exist to invest in real properties of all sorts, either through direct funding of loans or through the purchase of mortgage-backed securities. Franklin BSP works on the former model, providing or servicing loans in the commercial real estate sector. The company has built up a portfolio primarily composed of first mortgage loans on multifamily residential properties – that is, the company is a mortgage lender for apartment complexes.

As of the end of last September, Franklin BSP’s portfolio included 157 loans, with an average loan size of $33 million. Of this, 74% was collateralized by multifamily properties. The remainder was secured by other types of commercial real estate, although the company has minimal exposure to office properties, which make up only 4% of the portfolio. Franklin BSP’s investments are mainly in senior mortgage loans, which account for 99% of the total; 95% of the portfolio loans are set at floating rates. The core portfolio principal balance at the end of 3Q24 was $5.2 billion.

This makes for big business. In the third quarter of 2024, the last period reported, Franklin BSP closed $380 million in new loan commitments and funded $325 million of principal balance. At the same time, the company received $510 million in loan payments.

The company’s approach to loan origination is to tailor loans to specific properties – although it does stick to a profile on first mortgage loans. That profile includes loan sizes between $10 million and $250 million; up to an 80% loan-to-value ratio; a 3- to 5-year term for transitional loans; and a 10-year term for stabilized loans. Franklin BSP will consider any commercial property type, although, as noted, the company does lean toward multifamily residential properties. A primary aim in Franklin BSP’s activity is to generate a stable income for investors.

Which brings us to the dividend. Franklin BSP last declared its dividend on December 16 and paid it out on January 10. The common share dividend was set at $0.355, marking the twelfth payment in a row at that rate. The dividend annualizes to $1.42 per common share and gives a robust forward yield of 11.2%.

The company backs up its dividend with strong liquidity. Franklin BSP reported $1.1 billion in total liquidity at the end of 3Q24, of which $346 million was in cash and cash equivalents.

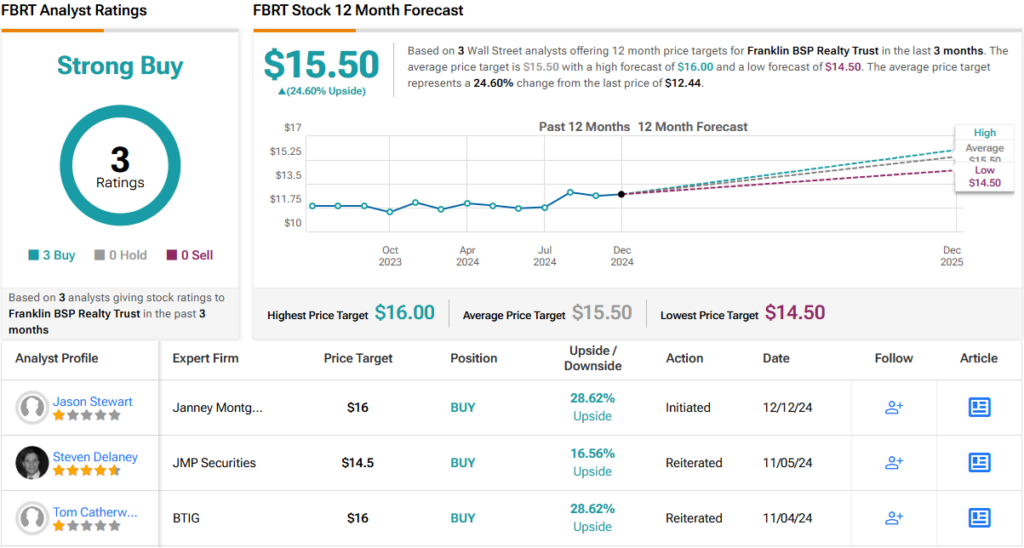

This REIT has caught the eye of Janney analyst Jason Stewart, who is impressed by Franklin BSP’s overall position. Stewart says of the company, describing that position: “FBRT operates one of the strongest balance sheets in the sector, has world-class sponsorship, and a peer-leading track record through a challenging CRE lending market. The company’s origination platform has led the sector in activity and sets the company apart from peers. Current vintage loans will produce cyclically high ROEs, and with 36% of the portfolio in 2023/2024 vintage originations, the company is in a unique position to capitalize on the dislocation in the CRE lending market. Over time, we expect required returns for best-in-class CRE mortgage REITs to trend back to historical averages in the 8% – 9% range.”

These comments support the analyst’s Buy rating, while his $16 price target implies a ~29% upside potential on the one-year horizon. Together with the dividend yield, the total one-year return here is potentially 40%. (To watch Stewart’s track record, click here)

Overall, FBRT shares have a Strong Buy consensus rating, based on 3 unanimously positive Wall Street reviews. The shares are priced at $12.44, and their $15.50 average price target price suggests that the stock will gain ~25% over the next 12 months. (See FBRT stock forecast)

BrightSpire Capital (BRSP)

For the second stock on our list, we’ll look at another REIT, BrightSpire Capital. This is an internally managed REIT, with a $739 million market cap and a focus on building a diverse portfolio of commercial real estate assets. The company believes in economies of scale, aiming to leverage that for a competitive advantage.

Getting into details, BrightSpire has a portfolio worth approximately $3.9 billion, and comprised of 76 loans. The loan segment, consisting of senior and mezzanine loans, makes up 80% of the total portfolio. The remaining 20% is mainly composed of net lease and other real estate transactions. Of the properties in the portfolio, 41% are multifamily dwellings, and 38% are office properties. The remainder is mostly composed of industrial spaces, hotels, and mixed-use properties. Geographically, BrightSpire is active in the US, mainly in the West (43% of the portfolio) and Southwest (28% of the portfolio). The company has a presence in the Northeast, at 14% of the portfolio, and 6% of its properties are located in Europe.

We should note that BrightSpire’s revenues and earnings have been trending downward in recent quarters. In the last period reported, 3Q24, the company had a bottom line of $0.21 per share, by non-GAAP measures. While the year-ago figure was 28 cents per share, the 3Q24 number beat the forecast by 2 cents per share.

Even though it was slipping, the company’s earnings were sufficient to support the common share dividend. BrightSpire last declared the dividend payment on December 16, and paid it out on January 15. The 16-cent dividend annualizes to 11.2%.

For analyst Gaurav Mehta, covering this REIT for Alliance Global, the key point here is potential. He believes that BrightSpire is well-positioned to deliver improved results going forward, and that the dividend is a clear advantage. Mehta writes of the company, “Our Buy rating is based on restart of new loan originations, management’s focus on resolving watch list loans and REO assets, balance sheet with ample liquidity and a dividend yield of 11.2%. At the current valuation, we believe that risk/reward is skewed to the upside.”

Quantifying his stance, Mehta puts a Buy rating on BRSP shares, with a $7.25 price target that suggests the stock will gain ~30% in the next 12 months. With the dividend yield added in, that upside can reach 41%. (To watch Mehta’s track record, click here)

There are 6 recent analyst reviews on file for BRPS shares, with a 4-to-2 split favoring Buy over Hold to give the stock its Moderate Buy consensus rating. The shares are currently trading for $5.59, and their $7.60 average price target, even more bullish than the Alliance Global view, points toward a gain of ~36% by early next year. (See BRSP stock forecast)

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.