Telehealth company Hims & Hers Health (HIMS) witnessed a major dip in its stock recently despite reporting 95% revenue growth for the fourth quarter of 2024 and a notable jump in earnings. Investors are concerned due to gross margin pressures and the company’s update that it will stop offering compounded semaglutide on its platform after the first quarter, triggering mixed reviews from analysts about the future of its weight loss business.

End of HIMS’ Semaglutide Tailwinds

Despite the recent pullback, HIMS stock has rallied over 187% in the past year and is up 69% year-to-date. This surge came in as the company began prescribing compounded semaglutide, the active ingredient in Novo Nordisk’s (NVO) GLP-1 blockbuster weight loss medications Ozempic and Wegovy, when the branded treatments were in shortage.

However, on February 21, the U.S. Food and Drug Administration (FDA) announced that the persistent U.S. shortage of Novo Nordisk’s weight loss injection Wegovy and diabetes treatment Ozempic had been resolved. This announcement negatively hit Hims & Hers Health and other companies that gained by offering compounded semaglutide.

Hims & Hers’ weight loss offerings will now mainly include its oral medications and the liraglutide injection, which the company plans to launch in the early second half of 2025. Also, the company has indicated that under the 503A personalization exemption, it may offer personalized doses of semaglutide, if clinically applicable.

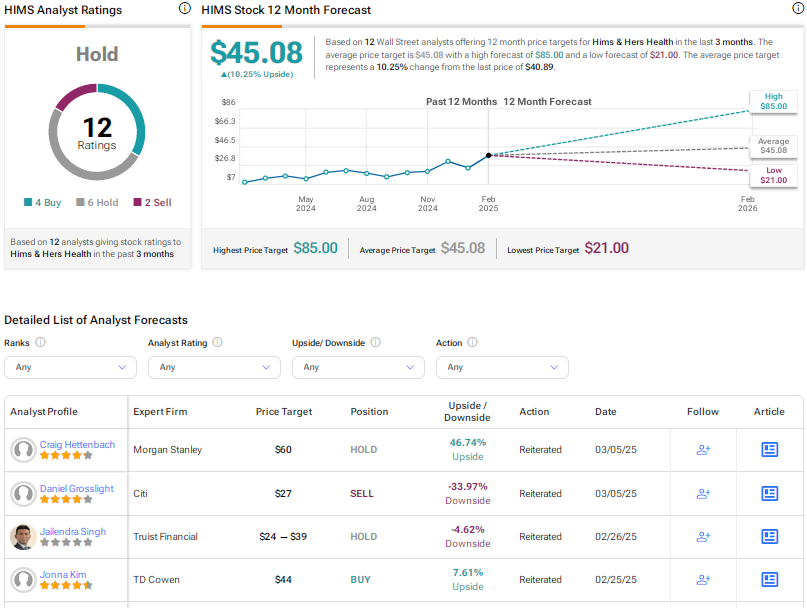

Analysts Have Mixed Opinions on HIMS Stock

On Wednesday, Citi analyst Daniel Grosslight reiterated a Sell rating on HIMS stock with a price target of $27 following an announcement by Novo Nordisk about the launch of NovoCare Pharmacy, a cash pay-only offering that allows uninsured patients (or commercial patients having no coverage) to buy Wegovy for $499 per month. Grosslight noted that Novo’s offering is similar to Eli Lilly’s (LLY) LillyDirect offering for Tirzepatide vials and will impact Hims & Hers and other pharmacies offering compounded semaglutide.

In contrast, Needham analyst Ryan MacDonald reiterated a Buy rating on HIMS stock and boosted the price target to $61 from $31. While the FDA’s announcement that semaglutide is no longer in shortage shortens the runway for revenue generation from the commercially available doses of compounded semaglutide, the analyst noted that HIMS sees a durable weight loss revenue stream this year, driven by a combination of personalized semaglutide, oral weight loss offerings, and generic liraglutide.

Assuming $725 million of weight loss revenue, HIMS issued FY25 guidance well above the Street’s estimate and Needham’s bull case expectations outlined in its 2025 top pick report on the stock. Consequently, MacDonald remains bullish on HIMS stuck and sees the pullback as a buying opportunity, given the encouraging growth in the company’s non-weight loss business and durable weight loss revenue stream.

IS HIMS Stock a Buy, Sell, or Hold?

Overall, Wall Street is sidelined on HIMS stock, with a Hold consensus rating based on four Buys, six Holds, and two Sells. The average HIMS stock price target of $45.08 implies 10.3% upside potential.