Social media stock Pinterest (NYSE:PINS) recently brought out its earnings report, which went over like a lead balloon. But analysts stepped in and offered some commentary that suggested things might not have been as bad as they seemed at Pinterest, though they sure looked bad. However, the commentary wasn’t much help against the numbers, and Pinterest shares were down over 10% in Friday afternoon’s trading.

Piper Sandler’s Thomas Champion lived up to his surname for Pinterest, noting a new traffic partnership with Google (NASDAQ:GOOG) (NASDAQ:GOOGL) that was enough to keep an Overweight rating on Pinterest. He followed that up with a price target increase to a new Street high of $48. UBS’ Stephen Ju also joined in, noting that Pinterest was increasingly drawing demand from advertisers, which should help fuel revenue going forward.

A Growing Competitive Problem

Yet, even as advertisers seem to be making a comeback to digital media, there are signs of trouble for Pinterest here as well. Those advertisers seem to be moving to bigger platforms to spend their ad dollars, leaving Pinterest somewhat out in the cold. While Pinterest’s focus on delivering pictures—and occasional video—certainly does have a market niche, it doesn’t quite have the range of its larger competitors. Advertisers will want to get the most they can for their money, leaving Pinterest and smaller competitors to fight after the bigger firms’ leftovers.

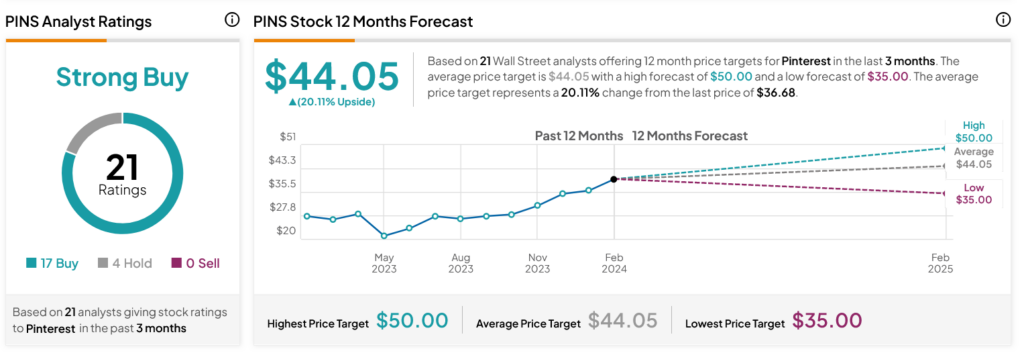

Is Pinterest a Buy, Sell, or Hold?

Turning to Wall Street, analysts have a Strong Buy consensus rating on PINS stock based on 17 Buys and four Holds assigned in the past three months, as indicated by the graphic below. After a 47.58% rally in its share price over the past year, the average PINS price target of $44.05 per share implies 20.11% upside potential.