Alphabet (GOOGL) will be stepping up to the earnings plate tomorrow (February 4), when it will deliver its fourth quarter results after the market action comes to a close. While the shares have delivered market-beating gains of 41% over the past year, heading into the print, the stock looks primed to keep on outperforming.

Maximize Your Portfolio with Data Driven Insights:

- Leverage the power of TipRanks' Smart Score, a data-driven tool to help you uncover top performing stocks and make informed investment decisions.

- Monitor your stock picks and compare them to top Wall Street Analysts' recommendations with Your Smart Portfolio

That at least is the opinion of Oppenheimer analyst Jason Helfstein, who thinks Meta’s recent results bode well for the search giant.

“META indicated strong advertising trends and recent investor conversations suggest a favorable setup heading into results on search revenue concerns, but expecting higher margins,” the analyst explained. “Additionally, META confirmed Gen AI is driving ad price growth, which should also benefit GOOG, cementing it as an AI winner.”

Due to limited 3P data, Helfstein thinks investor expectations for Google are “lowest in mega-cap Internet,” and while the holiday season was strong and the economy is expected to perform well this year, he believes “investor bogey” is lower than the Street’s forecast of 10% revenue growth, although expectations for margins are higher.

Meanwhile, on the pertinent subject of AI, some investors worry that the “cohort dynamics” of younger chatbot users could negatively impact Google in the long run, but there is no evidence of this happening yet. “We believe GOOG is in a better position with AI than many investors had expected 12-18 months ago,” Helfstein went on to say.

DeepSeek’s recent impact also gets a shout-out here and in a positive way. While the current competition in ranking tables may be between DeepSeek and OpenAI, Helfstein thinks these leads tend to be short-lived as all major models incorporate advancements made by others. Bears might argue that declining costs will commoditize search, but Helfstein believes this view overlooks Google’s years of developing practical products and its “best in class” data.

Turning to the numbers, Helfstein forecasts Q4 growth for Search, YouTube, and Google Cloud Platform (GCP) at +12%/+10%/+32% year-over-year, compared to the Street’s expectations of +11%/+11%/+32%. The analyst projects GAAP EPS at $2.22, ahead of the consensus estimate of $2.12.

Looking ahead to Q1, Helfstein anticipates Search/YouTube/GCP revenue growth of +8%/+10%/+25% y/y, whereas Wall Street is modeling +9%/+9%/+30%. On GAAP EPS, he expects $1.98 versus the Street’s $2.03 forecast.

With an attractive Q4 setup in play, Helfstein has upped his price target from $215 to $225, implying a ~12% upside from current levels. He remains bullish on GOOGL, maintaining an Outperform (i.e., Buy) rating. (To watch Helfstein’s track record, click here)

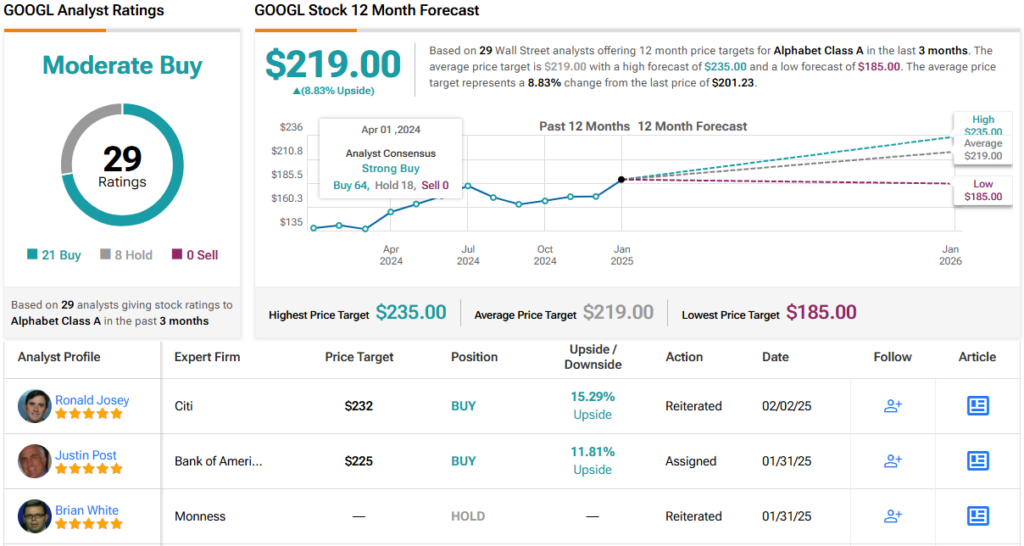

Other Wall Street analysts are similarly optimistic. Out of 29 recent GOOGL ratings, 21 are Buys and 8 are Holds, leading to a Strong Buy consensus. Going by the $219.60 average target, a year from now, shares will be changing hands for a ~9% premium. (See GOOGL stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.