American Woodmark (AMWD) reported disappointing Fiscal 2022 Q1 results ended July 31, 2021. Earnings and revenue fell short of consensus estimates as the company felt the full force of evolving inflationary pressures. AMWD plunged 12.36% to close at $70.46 on August 31.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

American Woodmark manufactures and sells kitchen, bath, and home organization products used in home construction markets.

Fiscal Q1 net sales were up 13.5% year-over-year to $442.6 million as the company experienced growth across key business lines. Additionally, repair and remodel sales channels posted high-teens growth. However, sales fell short of the consensus estimate of $461.79 million. (See American Woodmark stock charts on TipRanks)

Adjusted EPS was $0.70, down from $1.63 in the same quarter last year. It also missed consensus estimates of $1.55 a share. Furthermore, adjusted EBITDA shrunk to $32.1 million compared to $56.4 million in the same quarter last year.

Concerned by an uptick in inflationary pressures, American Woodmark plans to continue to implement significant pricing actions. The impact of these actions should increase in the second half of the year, according to the company’s CEO Scott Culbreth.

Culbreth stated, “Looking forward our focus remains on increasing production to match a strong demand environment and reducing backlog and realizing additional pricing actions to mitigate inflationary pressures in materials, logistics, and labor.”

During the quarter, American Woodmark carried out share buybacks worth $25 million.

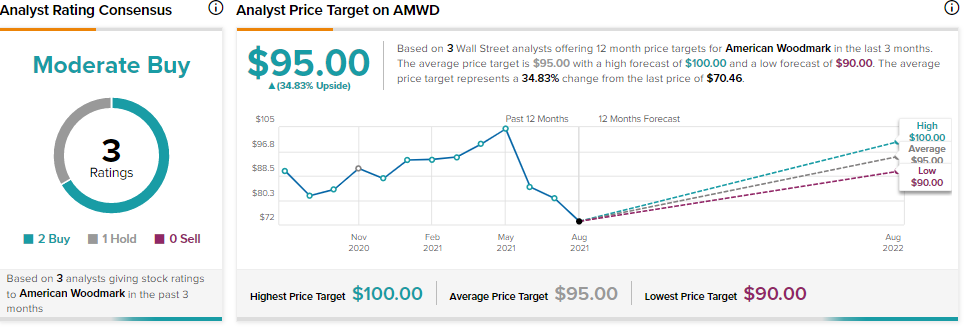

Recently, Jefferies analyst Collin Verron reiterated a Buy rating on the stock and decreased the price target to $95 from $103.

Consensus among analysts is a Moderate Buy based on 2 Buys and 1 Hold. The average American Woodmark price target of $95 implies 34.83% upside potential to current levels.

Related News:

Catalent Q4 Results Beat Estimates; Announces $1B Bettera Acquisition

What Does IGM Biosciences’ Newly Added Risk Factor Tell Us?

A Look at Madison Square Garden Entertainment’s Risk Factors