Shares of Advanced Micro Devices (AMD) finished up in today’s trading despite a cautious outlook from Mizuho Securities. The firm’s analyst, four-star rated Vijay Rakesh, noted that the chipmaker has some challenges in the artificial intelligence market due to Nvidia’s (NVDA) dominant position. Indeed, Rakesh pointed to AMD’s struggles to secure a significant share of the chip-on-a-wafer-substrate market, which is a technology that is used by Taiwan Semiconductor (TSM) to manufacture processors.

While Nvidia remains the leader in this space, Rakesh does see opportunities for AMD to gain ground in the traditional server and PC markets. As a result, Rakesh maintained his Outperform rating for AMD despite the cautious outlook. Interestingly, though, he lowered his price target from $140 to $120 per share. This is because the research firm lowered its prediction for Fiscal Year 2025. In fact, it now expects AMD to earn $31.9 billion in revenue and $4.70 per share, compared to the previous forecast of $32.2 billion in revenue and $5.00 in EPS.

The firm also changed its prediction for 2026 to $38.3 billion in revenue and $6.33 per share, which is slightly lower than what other experts predict. At the time time, Rakesh reduced his price target for Nvidia from $175 to $168, ahead of the company’s upcoming GTC event, in order to adjust for a lower earnings multiple.

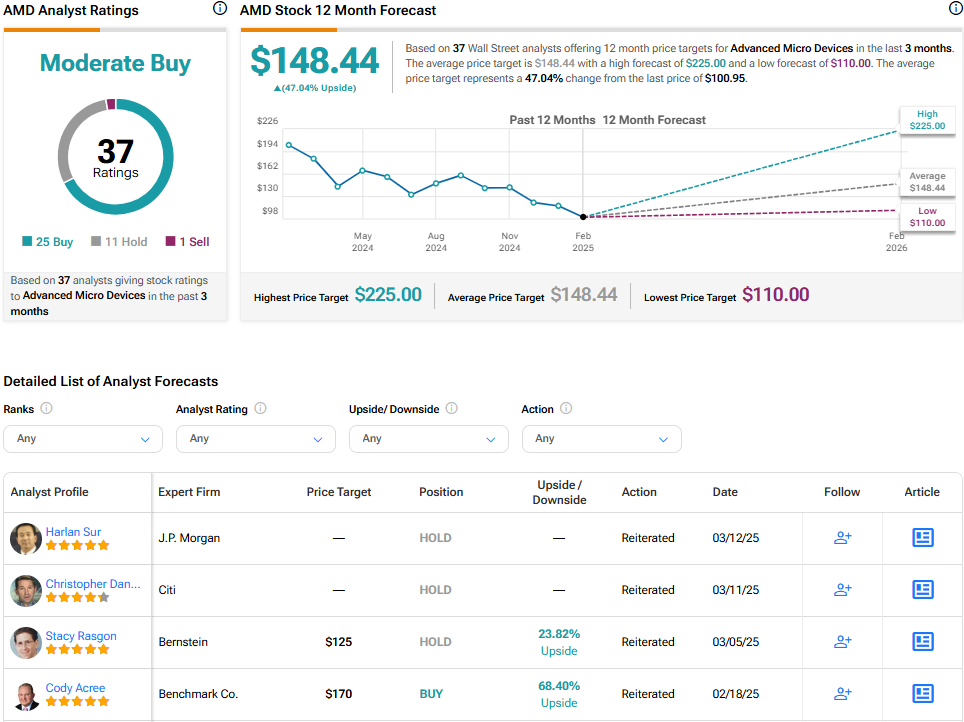

Is AMD a Buy, Sell, or Hold?

Overall, analysts have a Moderate Buy consensus rating on AMD stock based on 25 Buys, 11 Holds, and one Sell assigned in the past three months, as indicated by the graphic below. Furthermore, the average AMD price target of $148.44 per share implies 47% upside potential.