Advanced Micro Devices (NASDAQ:AMD) shares have been on a steep decline, sinking 36% over the past year. Not long ago, the company was seen as a real threat to Nvidia’s dominance in the AI chip space, but that narrative has taken a serious hit as the Street lowers expectations for AMD’s AI chip business.

Maximize Your Portfolio with Data Driven Insights:

- Leverage the power of TipRanks' Smart Score, a data-driven tool to help you uncover top performing stocks and make informed investment decisions.

- Monitor your stock picks and compare them to top Wall Street Analysts' recommendations with Your Smart Portfolio

With the semi giant about to report Q4 earnings tomorrow (February 4), Susquehanna’s Christopher Rolland, an analyst ranked in the top 1% of Wall Street stock experts, thinks investors might be in for some more disappointing news, despite the potential for a decent outlook.

“In short, we expect generally in-line guidance, with a possibility of upside driven by Server and PC,” the 5-star analyst said. “However, we note the likely removal of a full-year MI300 guide, perhaps a modest negative for AMD AI bulls. While buy-side MI300 expectations have been coming down for the last few months (we think between $6-7B from the prior $10B+ for 2025), overt signs of this deceleration may weigh.”

That said, considering the shares’ retreat, Rolland does go on to add that this deceleration is now “widely understood and (mostly) removed from shares.”

In fact, Rolland’s take on AMD is mostly positive. Regarding EPYC (DC CPU), his recent checks “support a strong 2025, driven primarily by share gains.” AMD is currently looking to expand its share in the hyperscaler market, particularly in China, while also accelerating adoption in the enterprise sector. Rolland believes the ASP (average selling price) “waterfall effect” from Milan to Genoa to Turin should positively impact revenue on a year-over-year basis, with the analyst expecting an increase of around 20%.

On the client side, driven in part by tariff-related pull-ins, Rolland’s checks have been “constructive,” while he recently raised December builds. Such a dynamic could help support Q4 and Q1, but could present risks to PC numbers in 2Q25 and further down the line.

For the Embedded segment, Rolland anticipates a “modest recovery” as FPGAs should improve after Q1, assuming inventory levels are finally normalized. Moreover, recent price increases of up to 20% could offer further support. In the Gaming segment, however, weak console sales continue to be a headwind.

The question is whether the company will comment on any declining sales of the MI300, and that could pose a risk to 2025 Street estimates. Rolland thinks old sell-side MI300 estimates for 2025 were just too exuberant, believing that following the results many on the Street could take the opportunity to “reset top line expectations for the year.”

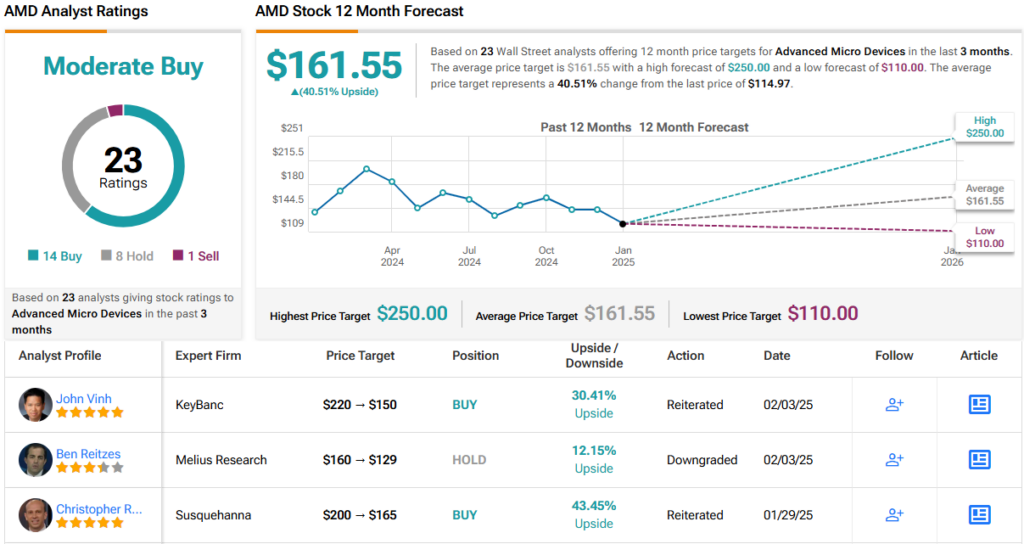

What it all boils down to is a Positive (i.e., Buy) rating from Rolland although his price target is lowered from $200 to $165. Nevertheless, there’s still potential upside of 44% from current levels. (To watch Rolland’s track record, click here)

Elsewhere on the Street, the stock claims an additional 13 Buys, 8 Holds and 1 Sell, for a Moderate Buy consensus rating. The average price target stands at $161.55, suggesting shares will gain 40% in the year ahead. (See AMD stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.