AI is the buzzword of the moment and has been the driving force behind the ongoing bull market. While you could say that there’s plenty of hype attached to the latest trend there’s no argument about how impactful the game-changing tech can be.

AI is being integrated across sectors, from healthcare and finance to manufacturing and consumer electronics, sparking demand for both edge and cloud-based computing solutions. This demand has been a boon for the semiconductor industry, with chipmakers in a race to make the most of this opportunity, as these companies provide the specialized chips that handle huge data loads and perform complex tasks.

Against this backdrop, companies have accelerated the development of AI-focused chips, and no one so far has grabbed this opportunity more spectacularly than Nvidia (NASDAQ:NVDA). The semi giant has positioned itself as the best maker of AI chips and has virtually cornered the market to itself.

However, if there’s one name that is considered a potential rival that can eat away at its dominance, then that is AMD (NASDAQ:AMD). The Lisa Su-led firm has already done that to another chip giant, having closed the gap considerably on Intel in the CPU market.

Earlier this year, Wolfe’s Chris Caso, an analyst ranked in the top 2% of Wall Street stock experts, added AMD to the firm’s Wolfe Alpha List, suggesting that AMD offered an attractive alternative to Nvidia’s soaring stock. However, Caso has recently shifted his recommendation, favoring another semiconductor player, Micron (NASDAQ:MU), due to its crucial role in supplying advanced memory and storage solutions essential for AI applications, which demand high data processing and rapid access speeds.

While Caso maintains a positive outlook on AMD’s AI potential and its server CPU gains, he sees an even greater opportunity ahead for Micron as AI demand accelerates. He also highlights that previous concerns around memory supply imbalances and pricing pressures, particularly in DRAM and HBM segments, appear overstated.

“Our thesis in memory has been that the imbalance between supply and demand in DRAM memory, driven by constrained CapEx levels and supplier focus on HBM, would drive industry shortages and pricing growth,” Caso explains. Although bearish sentiment emerged over potential oversupply issues in 2024 and 2025, Caso now sees these concerns as exaggerated.

As such, Micron has replaced AMD on the Wolfe Alpha List, though Caso retains an Outperform (i.e. Buy) rating on AMD with a $210 price target, implying a 42% upside over the next year. Meanwhile, his Outperform rating on Micron comes with a $200 price target, suggesting a potential 79% gain over the same period. (To watch Caso’s track record, click here)

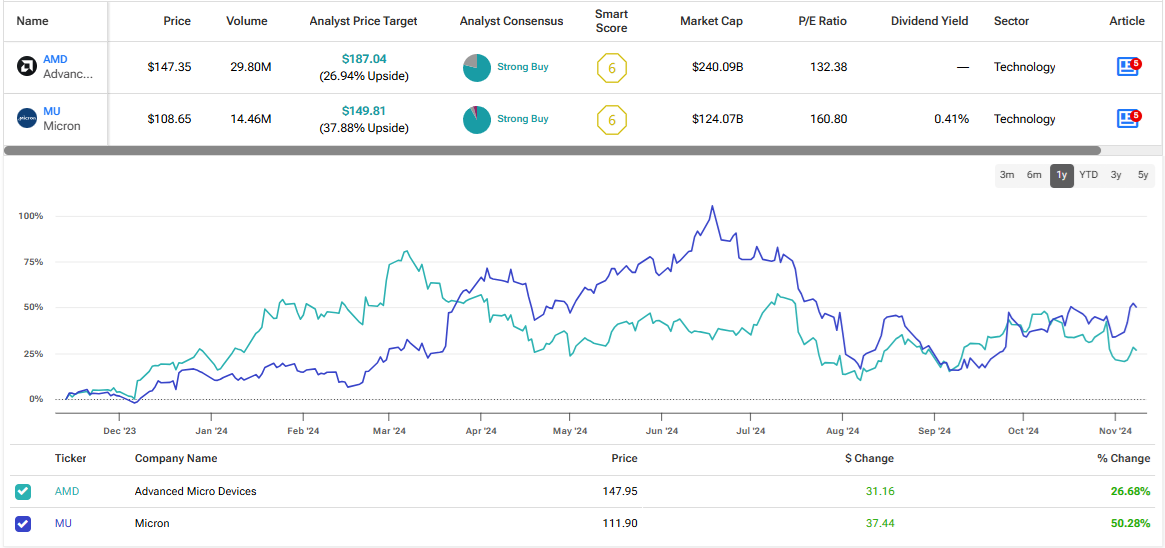

Meanwhile, both these names get plenty of support from the analyst community; AMD boasts a Strong Buy consensus rating based on 26 Buys vs. 6 Holds. Its average price target stands at $187.04, suggesting the stock will gain ~27% over the one-year timeframe. (See AMD stock forecast)

With 23 Buys vs. 1 Hold, the analyst consensus also rates Micron a Strong Buy. At $149.81, the average target indicates gains of ~38% are in store for the stock over the coming year. (See Micron stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.