The Advanced Micro Devices (NASDAQ:AMD) juggernaut has shown no signs of slowing down in 2024. Continuing where 2023 left off, the stock’s upward trajectory (up by 20% year-to-date) has been mostly uninterrupted.

Maximize Your Portfolio with Data Driven Insights:

- Leverage the power of TipRanks' Smart Score, a data-driven tool to help you uncover top performing stocks and make informed investment decisions.

- Monitor your stock picks and compare them to top Wall Street Analysts' recommendations with Your Smart Portfolio

However, as AMD prepares to announce its 4Q23 results today and provide a glimpse into its outlook for the year, the question arises: Could these consistent gains become a double-edged sword if the chip giant fails to deliver a blockbuster report?

Well, that is a possibility, says UBS analyst Timothy Arcuri, although going by the analyst’s latest checks, that seems highly unlikely. In fact, his recent checks have left Arcuri feeling confident ahead of the print.

“The tactical setup around earnings is complicated somewhat by the recent rally, but we are nonetheless more confident on AMD’s data center GPU revenue opportunity and are significantly raising our CY24/CY25 estimates,” the 5-star analyst said.

Fueling Arcuri’s bullish stance are his channel and customer checks that validate his view that AMD has “firm demand commitment” for ~400,000+ MI300A/X accelerator series units for C2024.

While that figure is in-line with how Arcuri thought demand would play out since last summer, until recently the analyst was uncertain around supply and cautious regarding the potential for double ordering. “After having gone back to several customers and suppliers, we are more confident that these units are real and AMD now has sufficient CoWoS capacity to do 10%+ the volumes of NVDA,” he explained.

Even factoring in a “very conservative” ASP (which could reach as much as $20k+ for some clients), this implies revenue of $5 billion for data center GPU could represent a “pedestrian target” for 2024. Arcuri even this thinks that AMD could see out the year at a run-rate that could be nearer to $10 billion/year with GPU units still set for further quarter-over-quarter growth through most of 2025.

Accordingly, Arcuri has increased his respective MI300 revenue forecasts for CY24/CY25 from $2.3 billion/$4.3 billion beforehand to $4.8 billion/$10.8 billion. “Though our new CY24 revenue estimate of $4.8B is >2x our prior estimate,” Arcuri said, “it is still baking in a lot of conservatism both in terms of units and ASP.”

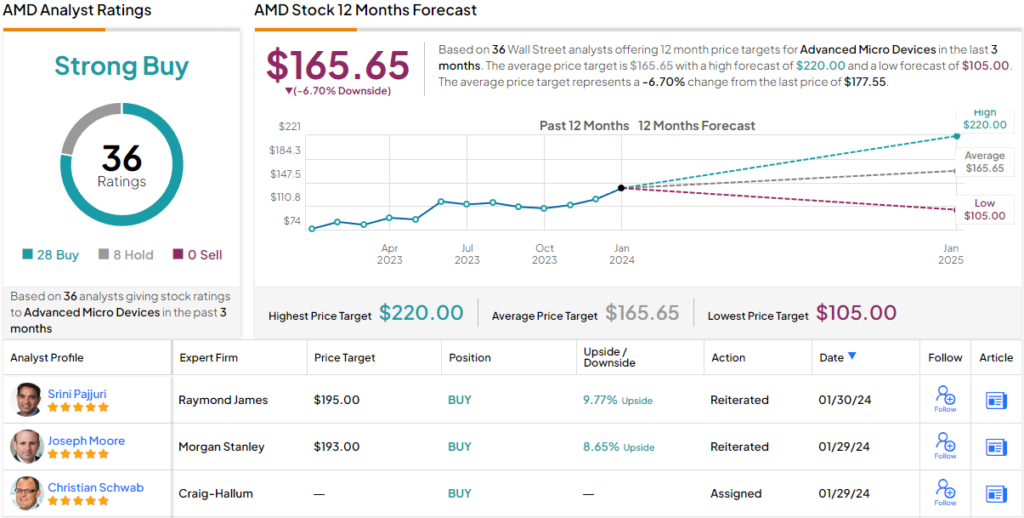

That optimism also translates to a new price target and a Street-high one at that. Arcuri’s figure takes a big leap from $135 to $220, suggesting the stock will post growth of 24% in the year ahead. (To watch Arcuri’s track record, click here)

The current consensus among analysts presents a bit of a puzzle. Despite a Strong Buy consensus rating, with 28 Buy recommendations vs. 8 Holds, the sentiment is that the stock has become overheated. As such, the $163.87 average target implies the stock will post a decline of ~7% over the coming months. It will be interesting to see whether the analysts update their price targets shortly. (See AMD stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.