For the first time in a while, I’m considering buying one of the most exciting tech companies in the Nasdaq: Advanced Micro Devices (AMD). Based on my valuation model, the stock could deliver a 35% compound annual growth rate in price over the next three years. In addition, it appears to have a 35% margin of safety for investment at this time. As a semiconductor company well-positioned to capitalize on long-term AI demand, the stock has a strong operational context. Given these factors, I am bullish on AMD stock.

Confident Investing Starts Here:

- Easily unpack a company's performance with TipRanks' new KPI Data for smart investment decisions

- Receive undervalued, market resilient stocks right to your inbox with TipRanks' Smart Value Newsletter

AMD’s Recent Downtrend Reveals an Attractive Entry Point

In the last six months, AMD stock is down by approximately -35% in price. This creates a potential buying opportunity when the company’s medium-term growth prospects are placed alongside the new valuation that has emerged. To illustrate the value opportunity, consider that the stock had a GAAP price-to-earnings ratio of around 400 in March 2024, but it is now just over 100. Moreover, the company’s price-to-sales ratio has dropped from 15 in March 2024 to just 7.8 today.

While Nvidia (NVDA) has the most dominant moat in AI infrastructure provision with its world-class graphics processing units, AMD is shrewdly focusing its resources on capturing the AI inference market. This market requires different computational capabilities compared to the AI model training market, and is also expected to be more protracted, allowing for less cyclical dynamics in growth.

AMD’s Data Center segment’s revenue grew by 122% year-over-year in Q3 2024, and the company expects similar growth to continue, supported by the release of new products like the MI350 series in late 2025. While the market was clearly disappointed by AMD’s lowered guidance for Q4 2024 and Fiscal 2025, the market sell-off of AMD’s stock that followed is seen as an opportunity for value investors.

Based on my research and calibrated with the Wall Street consensus estimates, a compound annual growth rate of about 20% in AMD’s revenues over the next three years is likely. In addition to this, the company’s net margin is most certainly going to expand significantly over the next three years due to cyclical dynamics, where AMD is entering a profit harvesting phase after a heavy investment period where it positioned itself to capitalize on new compute demand.

To put this growth potential into perspective, AMD’s financial projections highlight significant earnings power. At a net margin without non-recurring items of 35% in December 2027, this will lead to a net income without non-recurring items of $15.75 billion if it has total revenue of $44.5 billion. In addition, with a moderate increase in the company’s outstanding shares over the next three years to about 1.9 billion (aligning with historical trends), the company will have an earnings per share without non-recurring items of $8.30. This outlook is a strong foundation to invest from.

AMD Stock Could Be Worth $290 in Three Years

I’m bullish on AMD stock for the substantial 35% compound annual growth rate I could achieve over three years if the stock hits my price target of $290. The company’s price-to-earnings ratio without non-recurring items is currently nearly 39. I consider this approximately fair, but I do think that a moderate contraction in this is likely by December 2030 due to saturation in the current AI-related upcycle.

The fair value is further elicited by a future three-year earnings per share without non-recurring items consensus estimate of 39.5% compared to 27.1% as an actual historical three-year annual average, and a price-to-sales ratio of 7.9 versus a 10-year median of 5.45.

At a price-to-earnings without non-recurring items ratio of 35 in December 2027, the company’s stock price will be $290, given my estimate that it will have $8.30 in earnings per share at the time.

Additionally, AMD’s weighted average cost of capital is 16.84%, with an equity weight of 98.61% and a debt weight of 1.39%, where equity costs 17.03% and debt costs 3.75% before tax. When discounting back my December 2027 price target of $290 to the present day using the company’s weighted average cost of capital as the discount rate, the implied intrinsic stock value at the moment is $180.

As the current stock price is $115, the implied margin of safety for investment is 35%.

What Is the Target Price of AMD?

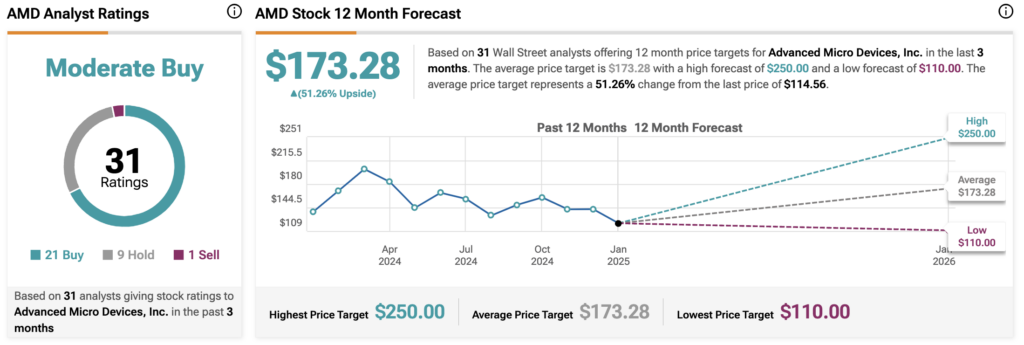

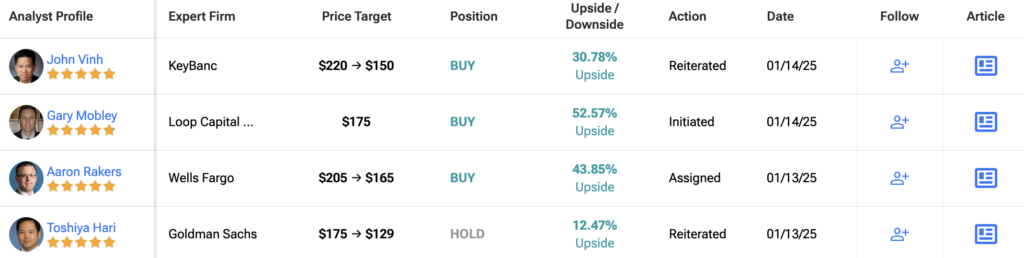

On Wall Street, AMD has a consensus Moderate Buy rating based on 20 Buys, nine Holds, and one Sell. The average AMD price target indicates a 50% upside potential over the next year. Given this outlook, I feel even more confident in my independent analysis and three-year price target of $290.

Key Takeaway: AMD Stock Is an Opportunity Worth Considering

Investing in the best companies in the world is not just about buying into a company’s operational and financial strengths. In addition, valuation is perhaps the most important (and often overlooked) quality of an investment that capital allocators must focus on to achieve the greatest alpha possible. Six months ago, AMD’s stock price was too expensive, but at this valuation, I think the medium-term returns have the potential to be exceptional.

Looking for a trading platform? Check out TipRanks' Best Online Brokers , and find the ideal broker for your trades.

Report an Issue