After revealing its Q1 results, Amazon (NASDAQ:AMZN) earned a polite round of applause from the Street for beating expectations on both revenue and earnings.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

The company generated revenue of $143.3 billion in the quarter, amounting to a 12.5% year-over-year increase while outpacing the Street’s forecast by $750 million. Likewise, EPS of $0.98 easily trumped the analysts’ expectations of $0.83, as operating income rose by 218% from the same period a year ago to $15.3 billion.

While ecommerce revenues still account for the bulk of sales, the star of the show, however, was the all-important AWS business, which saw revenue climb by 17.7% y/y to $25 billion, bettering the 14.7% anticipated by Wall Street and accelerating from Q4’s 13% jump.

The strong AWS performance garnered positive attention from Citi’s Ronald Josey, a 5-star analyst rated in the top 1% of the Street’s stock pros, who provided an upbeat assessment.

“With AWS growth reaccelerating to +17% Y/Y, faster delivery improving frequency and conversion rates, and the potential for sustained margin expansion, we are incrementally positive on shares of Amazon,” said Josey. “And with core AWS demand accelerating as optimizations normalize and GenAI generating a multi-billion ARR (and quickly becoming one of Amazon’s growth pillars), we believe the focus increasingly turns to expanding OI margins.”

Pertaining to that, as an increasing number of customers depend on Amazon for their daily necessities, conversion rates are seeing an improvement due to the company’s newer regionalized fulfillment network. And with North American profit margins growing by 460 basis y/y and international margins becoming positive, Josey believes these are the “early days of improving Retail profitability.”

Over the short-term, the conversation might revolve around the “margin benefit from extending the useful life of servers,” yet with multiple long-term growth drivers in the mix, Josey thinks the business is now “structurally more profitable.”

Accordingly, Josey rates AMZN shares a Buy, while raising his price target to a Street-high of $245 (from $235), suggesting the stock has room for growth of ~33% from current levels. (To watch Josey’s track record, click here)

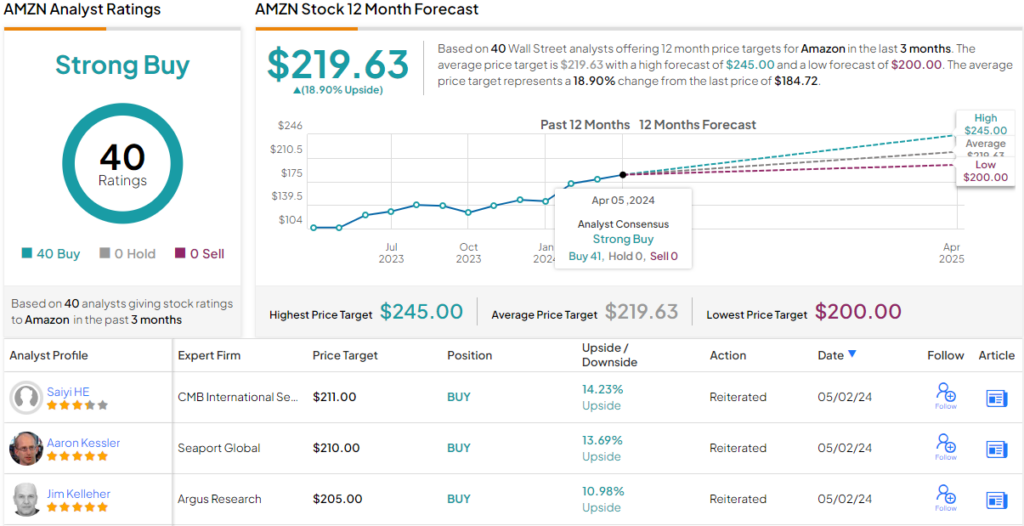

It’s not often that the analysts all agree on a stock, so when it does happen, take note. AMZN’s Strong Buy consensus rating is based on a unanimous 40 Buys. The stock’s $219.63 average price target suggests ~19% from the current share price of $184.72. (See AMZN stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.