Amazon.com Inc. (AMZN) said it is leasing an additional 12 Boeing (BA) 767-300 converted cargo aircraft as the e-commerce giant seeks to make delivery times faster amid an increase in online orders.

One of the new aircraft joined Amazon’s air cargo operations in May, and the remaining 11 are expected to be delivered in 2021. These aircraft will be added to Amazon’s existing fleet of 70 aircraft.

“Amazon Air is critical to ensuring fast delivery for our customers – both in the current environment we are facing, and beyond,” said Sarah Rhoads, VP of Amazon Global Air. “During a time when so many of our customers rely on us to get what they need without leaving their homes, expanding our dedicated air network ensures we have the capacity to deliver what our customers want: great selection, low prices and fast shipping speeds.”

In addition, Amazon announced that it will open new regional air hubs at Lakeland Linder International Airport in Florida later this summer and at San Bernardino International Airport next year, along with the central Amazon air hub at the Cincinnati/Northern Kentucky International Airport in 2021.

Last month, Amazon Air started gateway operations at Austin-Bergstrom International Airport in Austin, Texas, and Luis Muñoz Marín International Airport in San Juan, Puerto Rico.

Since its inception in 2016, the e-commerce company has invested hundreds of millions of dollars and created thousands of new jobs at Amazon Air locations across the U.S., the company said.

Shares in Amazon have jumped 48% since mid-March as stay-at-home orders during the coronavirus pandemic have been good for business. Demand for its products has surged, with the internet colossus expanding operations during lockdown and responding to consumers’ needs, many of which switched to online retail for the first time during the global crisis.

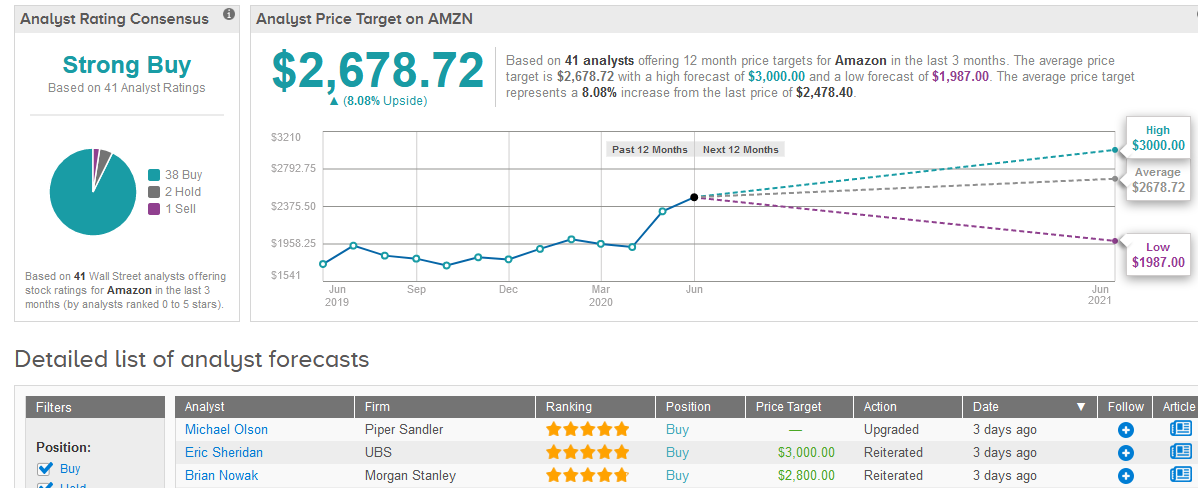

The stock closed little changed at $2,478.40 in Wednesday’s trading.

Five-star analyst Eric Sheridan this month reiterated a Buy rating on the stock with a bullish $3,000 price target forecasting shares are poised to gain another 21% over the coming year.

Sheridan believes that the change COVID-19 has brought about for consumer shopping, media consumption & cloud demands will not only be beneficial during shelter-in-place orders but also create “sustained long-term behaviors that are likely pulling forward prior multi-year industry adoption curves into 20/21”.

“We see AMZN as benefitting in terms of rev growth over the near to medium term and see most of the areas of incremental growth (scaled benefits of larger wallet share, 3P (especially FBA) shifts, media consumption, Prime sub, ad & cloud) as all accretive to medium to long term margin structure,” Sheridan wrote in a note to investors.

Overall, Wall Street analysts have a bullish outlook on Amazon. The stock scores 38 Buy ratings versus 2 Hold and 1 Sell rating adding up to a Strong Buy consensus. The $2,678.72 average price target is less aggressive than Sheridan’s but still implies 8% upside potential in the coming 12 months. (See Amazon stock analysis on TipRanks).

Related News:

Amazon’s Jeff Bezos Invests In UK Freight Startup Beacon

Apple Snaps Up AI Startup Inductiv, As Analysts Boost PTs On Store Reopenings

KKR Invests $1.5 Billion in Reliance’s Jio Platforms In Biggest Deal In Asia