Alphabet (GOOGL) is set to report its Q3 earnings on October 29, and I am bullish leading up to the report. The tech giant has been increasing its profit margins and delivering accelerated revenue growth for its investors. Corporations are still pouring money into online advertising, and Alphabet remains a leader in the artificial intelligence industry.

Google Cloud Is The Next Growth Opportunity

Online advertising has been the main catalyst for Alphabet stock’s ascent, but Google Cloud is another reason why I am bullish on the stock. Google Cloud growth has outpaced advertising growth for several quarters, including the second quarter of 2024.

During that quarter, overall revenue jumped by 14% year-over-year. Meanwhile, Google Cloud revenue increased by 28.8% year-over-year to reach $10.35 billion and represented 12.2% of the firm’s total revenue. Google Cloud is positioned to become a larger slice of the pie in future quarters. Not only is the segment outpacing ad growth, but cloud computing has a tremendous runway thanks to artificial intelligence.

The research firm Grandview Research projects that the cloud computing market will maintain a compounded annual growth rate of 20.3% from now until 2030. The same research firm also projects a 36.5% CAGR for the artificial intelligence industry. If AI continues to soar and exceed expectations, some of that growth can spill over to the cloud computing industry. Investors should closely monitor Google Cloud’s growth rate in Q3, as it should continue to outpace online advertising revenue. I feel optimistic about Google Cloud revenue growth heading into the third quarter.

Profit Margins Will Continue to Rise

Over the past few quarters, Alphabet has reported higher net income growth rates than revenue growth rates. Top-line growth has still been in the double-digits for most quarters, but net income has taken off. This trend makes me bullish about Alphabet stock going into Q3 earnings.

Let’s take a look at the previous quarter. While revenue increased by 14% year-over-year, net income jumped by 29% year-over-year. The end result was a 27.9% net profit margin. Alphabet’s profit margins have been trending upward, and it is realistic to see the company post a 30% net profit margin by the end of 2025, if not sooner. Rising profits also give the company more flexibility to raise its dividend by 10% or more each year.

Google Cloud has been a major catalyst for the company’s profit margin growth. This segment’s operating income almost tripled year-over-year, going from $395 million in Q2 2023 to $1.17 billion in Q2 2024. Enhanced profits will also put a brighter spotlight on the stock’s 23.7 P/E ratio. Alphabet’s P/E ratio currently lags behind the S&P 500’s 30 P/E ratio and is also lower than that of each stock in the Magnificent Seven. This relatively low valuation, combined with rising profits, makes Alphabet stock look attractive going into third-quarter results.

Alphabet Is in the Middle of a Correction

Some tech stocks like Amazon (AMZN) and Meta Platforms (META) are near all-time highs leading up to their third-quarter results. However, Alphabet is in the middle of a correction. It’s down by roughly 14% from its all-time high, and this dip makes me more bullish on the stock.

There aren’t many quality companies that also trade at quality prices. However, Alphabet is an exception to the rule. The dip mostly stems from fears about a potential monopoly breakup that could impact Alphabet’s advertising revenue. In my opinion, these fears are overblown and present an attractive long-term buying opportunity.

Is Alphabet a Buy?

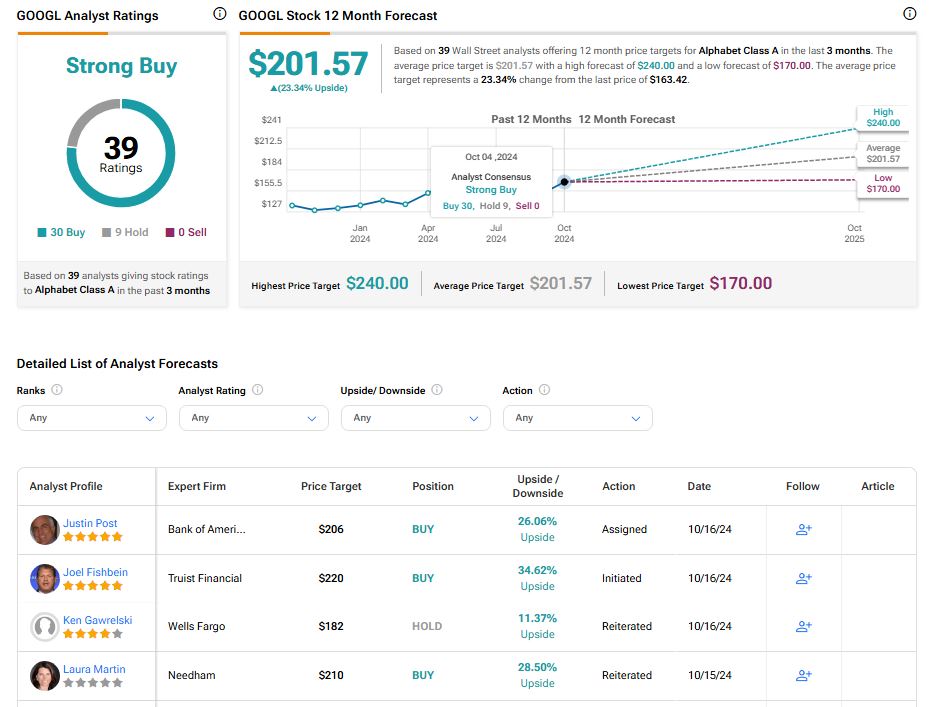

Alphabet is currently rated as a Strong Buy among 39 analysts. The stock has received 30 Buy ratings and nine Hold ratings. No analyst has rated Alphabet stock as a sell. At $201.57, the average GOOGL price target implies 23.34% upside potential.

See more GOOGL analyst ratings

The Bottom Line on Alphabet Stock

Alphabet is one of the most reasonably priced big tech companies in the stock market, and it can generate sizable gains for long-term investors. The company is a leader in the online advertising industry and has a rapidly growing cloud computing segment. Google Cloud now makes up 12.2% of total revenue and should continue to make up a larger slice of the pie in upcoming quarters.

Investors can also expect to see higher profit margins as Alphabet continues to strengthen its bottom line. Recent news about a potential monopoly breakup has scared some investors, but the uncertainty presents an opportunity before Alphabet reports earnings on October 29.